Trade Idea - Short Put on CVX

Published on July 6, 2026 | 4 min read(Last updated on July 9, 2026)

Table of Contents

Table of Contents

Disclaimer: The trades discussed in this blog reflect the author's personal strategies and decisions. These are not financial advice and should not be considered recommendations to buy, sell, or hold any financial instruments. The author is not a licensed financial advisor. Options trading carries significant risk, and readers should perform their own research or consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Chevron (CVX) is trading around $168, and the options market is paying up to be short volatility here. IV rank is sitting at roughly 71%, which is rich for a large, slow-moving integrated oil major, so the put side is fat and that's the part that interests me. I don't need CVX to rally. I just need it to hold above $160 over the next 18 days, and I'm getting paid a healthy premium to take that side.

The Trade

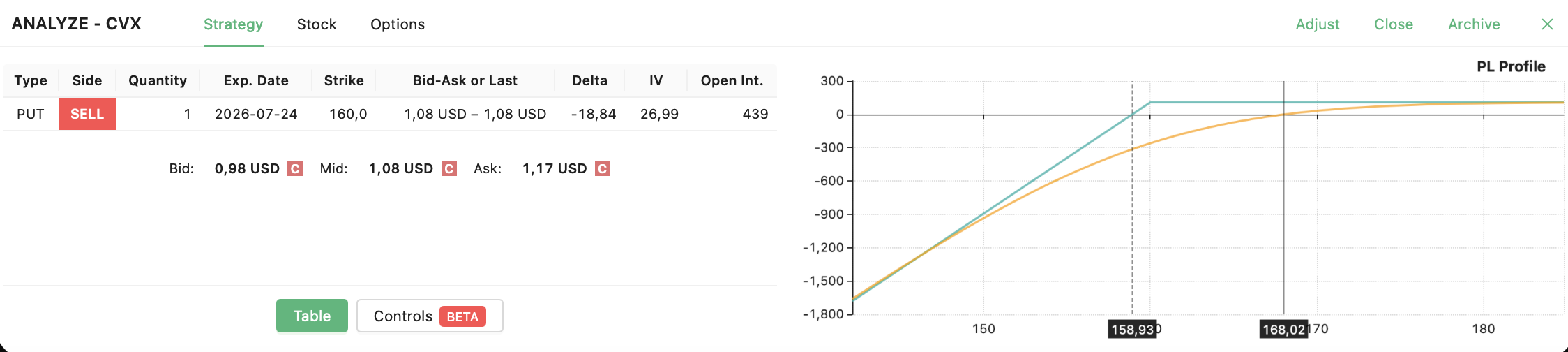

Here's the trade:

- Sell 1x CVX 24 Jul 2026 $160 Put @ ~$1.08

- Net credit: ~$1.08 ($108 per contract)

- Breakeven: $158.92

For reference, here is the current risk profile of the position:

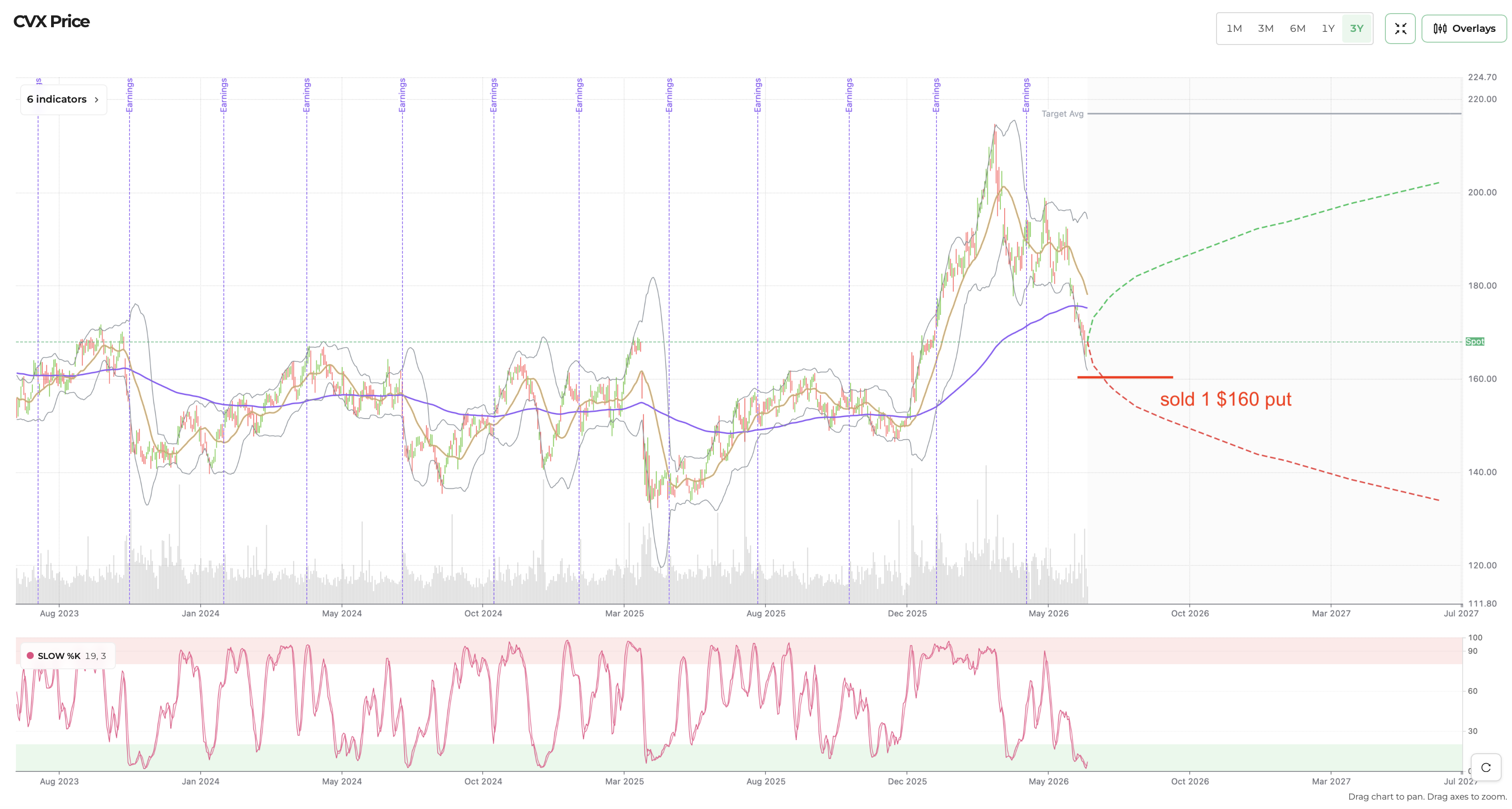

And this is the stock price chart:

The stock is trading near $168, and my $160 short strike sits about 5% below spot, which is a comfortable out-of-the-money entry. The short put is showing a delta around 19, so the market is pricing only about a 1-in-5 chance of it ever coming into the money. For this trade to get tested, CVX would have to drop close to 5% in under three weeks and keep sliding to my $158.92 breakeven. On a name this size, with a 4%-plus dividend yield underpinning it, that's the kind of buffer I want when I'm selling into elevated volatility rather than betting on direction. It helps that the pullback has largely already happened: CVX has slid from the $210s toward the high $160s, and the stochastic is sitting down in oversold territory, so I'm selling puts into weakness that already looks stretched rather than into a fresh top.

The main risk here is oil. CVX is a commodity name at heart, and if crude keeps sliding, Morgan Stanley has been flagging a possible global glut into the second half of the year, the stock can grind lower regardless of how far away my strike looks today. Unlike a defined-risk spread, a short put leaves my downside open: if CVX falls hard, I'm on the hook to buy shares well above where they'd be trading. I'm comfortable with that here for one reason: this is a stock I don't mind owning at $160. That's a supermajor with a strong balance sheet, a roughly 4% yield, and consistent buybacks, at a cost basis about 5% under today's price. If I'm assigned, I end up holding a quality dividend payer at a discount, not a broken momentum name.

The logic is straightforward: IV rank at 71% means I'm collecting richer-than-normal premium for a stock that doesn't usually move much, and with about 18 days to expiration theta has plenty of runway to chew through the $1.08 I took in. If IV mean-reverts lower from these elevated levels, which is the base case when rank is this high, that's a volatility tailwind stacked on top of the time decay.

The one date I'm watching is earnings. CVX reports Q2 results in the back half of July, and the consensus estimate clusters around July 31 (just after my July 24 expiration) which would let this trade clear before the event. But the exact date isn't fully locked in, and at least one calendar has flagged July 24 itself. If the report gets confirmed for expiration day, I'd treat that as event risk and either close early or roll out past the print rather than hold a short put naked into earnings. That's the single assumption I'd re-check before putting this on.

I'd expect to get out of this one fairly soon. With premium this inflated and the strike this far away, decay and an IV crush should let me buy the put back cheap well before expiration, and I'd rather book the bulk of the gain and free up the collateral than squeeze the last few cents. As always, I put myself in the worst-case scenario before pulling the trigger: if CVX sells off and challenges the $160 strike, my plan is to roll the put down and out, pushing to a later expiration and a lower strike to collect additional credit and rebuild the buffer, or simply take assignment and start selling covered calls against the shares. Either path keeps me in control instead of sitting and hoping.

As always, I have logged the trade in my trade log.

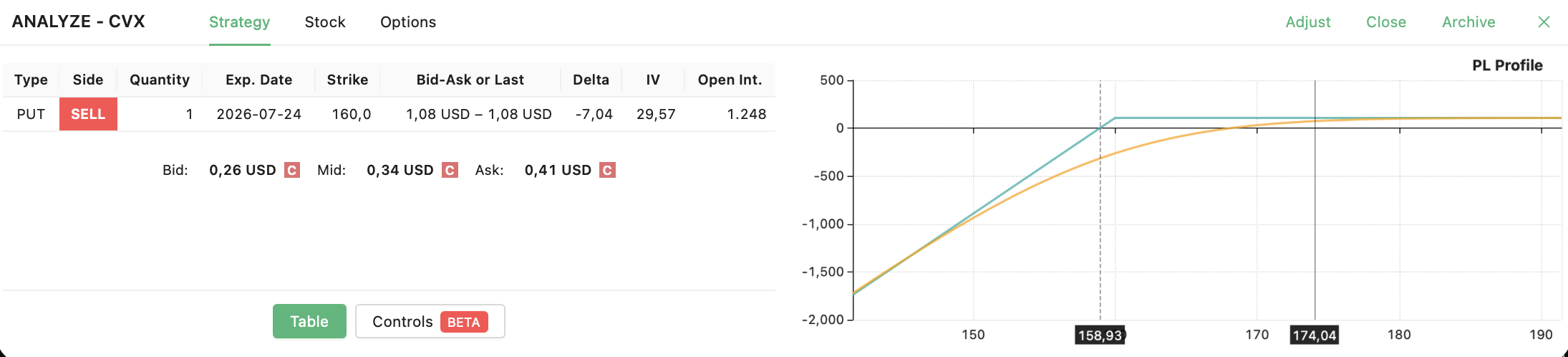

Update: Trade Closed

One of the easiest short put trades for this year. Closed it at a good and quick profit:

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.