Trade Idea - Bear Call Spread on AMKR

Published on June 29, 2026 | 3 min read(Last updated on July 9, 2026)

Table of Contents

Table of Contents

Disclaimer: The trades discussed in this blog reflect the author's personal strategies and decisions. These are not financial advice and should not be considered recommendations to buy, sell, or hold any financial instruments. The author is not a licensed financial advisor. Options trading carries significant risk, and readers should perform their own research or consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Amkor Technology (AMKR) is trading around $81.64, and the options market is paying up to be short volatility here. IV rank is sitting at roughly 93%, which is about as rich as this name gets, so the call side is fat and that's the part that interests me. I don't need AMKR to fall. I just need it to avoid a ~29% jump over the next couple of weeks, and I'm getting paid a healthy premium to take that trade.

The Trade

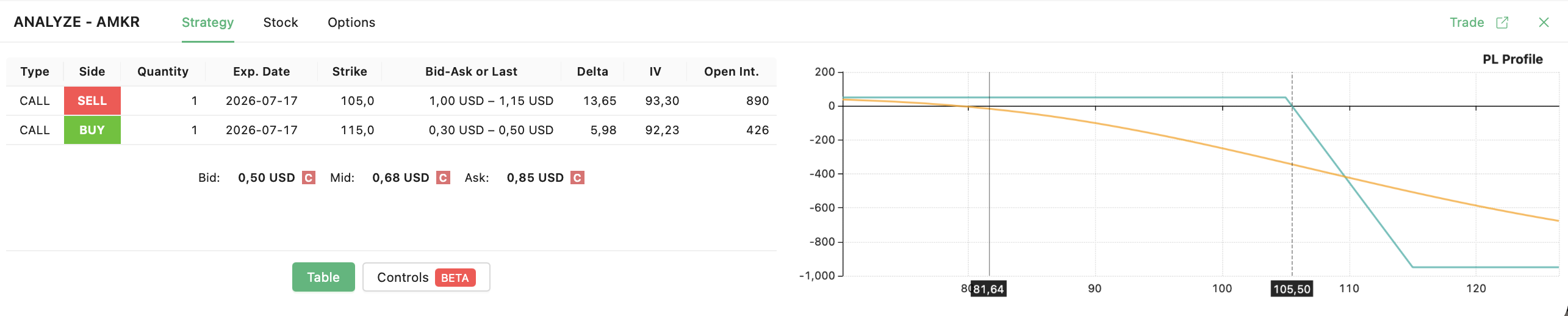

Here's the trade:

- Sell 1x AMKR 17 Jul 2026 $105 Call @ ~$1.05

- Buy 1x AMKR 17 Jul 2026 $115 Call @ ~$0.40

- Net credit: ~$0.68 ($68 per spread)

- Breakeven: $105.68

- Max risk: $932 (the $10 width less the credit)

For reference, here is the current risk profile of the position:

And this is the stock price chart:

The stock is trading near $81.64, and my $105 short strike sits roughly 29% above spot, which is a deep out-of-the-money entry. The short call is showing a delta around 14, so the market is pricing only a modest probability of it ever coming into play. For this trade to get tested, AMKR would have to put together a near-30% move higher in under three weeks. That's the kind of buffer I want when I'm fading a stretched, high-IV name rather than chasing direction.

The main risk here is a sharp momentum or sector-wide rally: semis can move fast, and a hot tape doesn't care about my strike placement. But that's exactly why I structured this as a defined-risk spread instead of a naked call: the long $115 wing caps my worst case at $932 no matter how far AMKR runs. Just as importantly, I don't see any big catalysts on the calendar between now and expiration, so I'm not bracing for a scheduled surprise. A normal grind higher still leaves plenty of room to my $105.68 breakeven.

The logic is straightforward: IV rank at 93% means I'm collecting richer-than-normal premium, the expiration falls ahead of the next scheduled earnings report so I'm not carrying event risk, and with about 18 days to expiration theta has plenty of runway to chew through the $0.68 I took in. If IV mean-reverts lower from these elevated levels, which is the base case when rank is this high, that's a volatility tailwind stacked on top of the time decay.

I'd expect to get out of this one fairly soon. With premium this inflated and the strike this far away, decay and an IV crush should let me buy the spread back cheap well before expiration, and I'd rather book the bulk of the gain and free up the risk than squeeze the last few cents. As always, I put myself in the worst-case scenario before pulling the trigger: if AMKR somehow takes off and challenges the $105 strike, my exit plan is to roll the spread down and out, pushing to a later expiration and resetting strikes to collect additional credit and re-establish the buffer rather than sitting and hoping.

As always, I have logged the trade in my trade log.

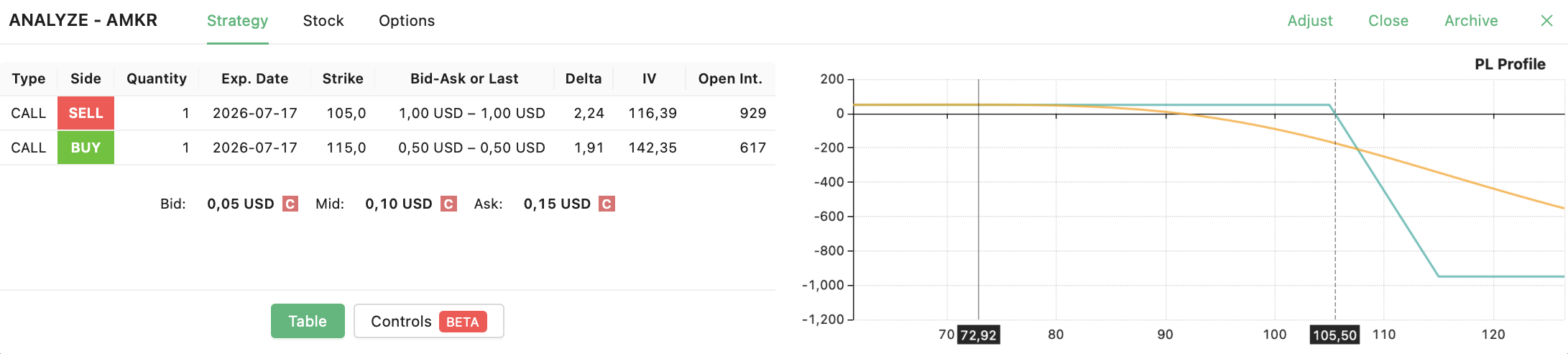

Update: Trade Closed

Easy trade, I'm actually sorry I did not simply buy a put since it fell harder than I thought. But it is what it is, still a very good profit in percentage terms:

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.