Trade Idea - Short Put on RCL

Published on June 15, 2026 | 3 min read(Last updated on July 9, 2026)

Table of Contents

Table of Contents

Disclaimer: The trades discussed in this blog reflect the author's personal strategies and decisions. These are not financial advice and should not be considered recommendations to buy, sell, or hold any financial instruments. The author is not a licensed financial advisor. Options trading carries significant risk, and readers should perform their own research or consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Royal Caribbean (RCL) has ripped back from its May lows and is now trading around $314, pushing up against the upper Bollinger Band after a strong, steady run higher. Normally a stock this extended isn't where I'd reach for premium, but IV rank is still sitting around 74%, so the put side is paying well, and that's the part that interests me. I don't need RCL to keep climbing here. I just need it to avoid a ~14% collapse over the next month, and I'm getting paid a rich premium to take that bet.

The Trade

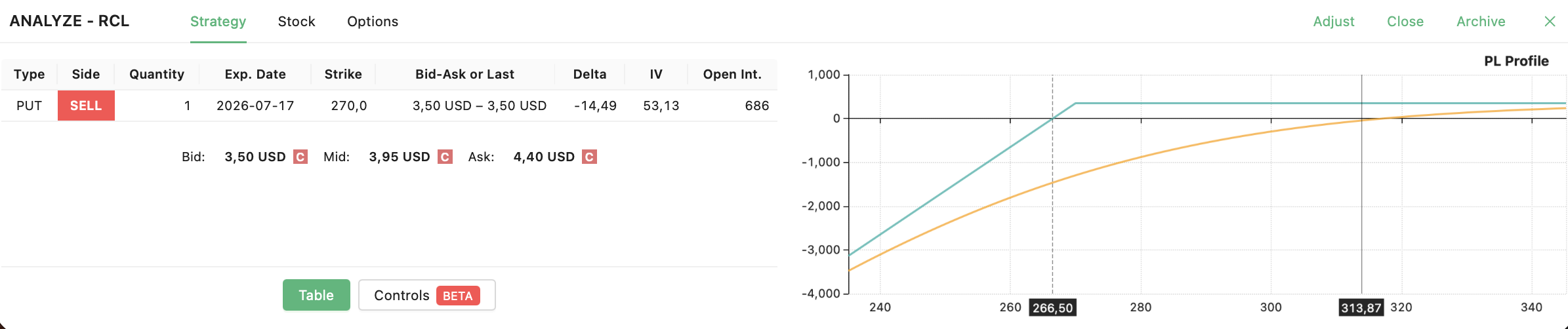

Here's the trade:

- Sell 1x RCL 17 Jul 2026 $270 Put @ $3.50

- Breakeven: $266.50

For reference, here is the current price chart of RCL:

The stock is trading near $314 after grinding up off the ~$265 area it bottomed at in mid-May. My $270 short strike sits roughly 14% below spot, which is a deep out-of-the-money entry: the option is showing a delta around -14, so the market is pricing only a modest probability of it ever coming into play. Just as importantly, $270 lands below the May swing low, so for this trade to get tested the stock would have to give back the entire recent rally and then break to fresh lows. That's the kind of buffer I want when I'm selling into strength rather than weakness.

The main issue here is that RCL is extended. The slow stochastic is up in the high-70s/80s, momentum has run hot, and a pullback from the upper band wouldn't surprise me at all. But that's exactly why I went so far out of the money instead of selling a closer, fatter strike. A normal mean-reversion dip toward the moving averages around $282-$285 still leaves me with a comfortable cushion to my $266.50 breakeven. My cycle work is looking good into July, with the bullish path the slightly cleaner one, so I'm not leaning on a continued melt-up. I'm leaning on the strike being far enough away that ordinary noise doesn't matter.

The logic is straightforward: IV rank above 70% means I'm collecting richer-than-normal premium, the expiration falls ahead of the next scheduled earnings report so I'm not carrying event risk, and with about 32 days to expiration theta has plenty of runway to chew through the $3.50 I took in. If IV drifts lower from here, that's a volatility tailwind on top of the time decay.

Royal Caribbean is a cash-generative leader in the cruise space with a strong booking backdrop, so I'd be even ok owning the shares if assigned. As always, I put myself in the worst-case scenario before pulling the trigger: if RCL somehow takes out $270 and I get assigned, I'm holding shares of a quality operator at roughly a 14% discount to today's price. From there I'd wheel it with covered calls or simply hold and wait it out.

As always, I have logged the trade in my trade log.

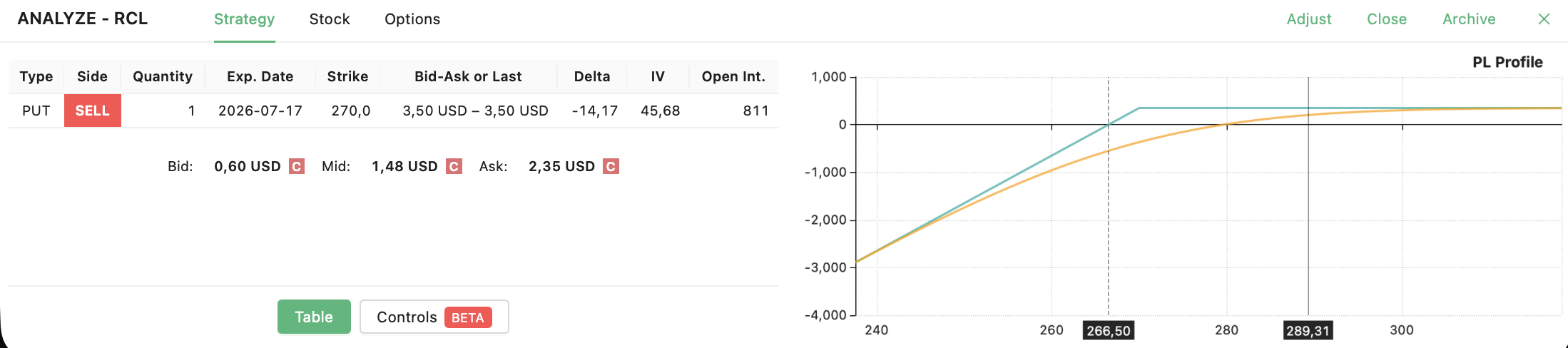

Update: Trade Closed

I thought this would be easier, but it turned out to be OK. I closed it at a very good profit:

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.