Back Ratio Spread - A Lesser-Known Strategy for Advanced Options Traders

Published on May 15, 2025(Last updated on October 16, 2025)

Reviewed by Leav Graves

The back ratio spread is an options strategy that traders use when they expect a strong move in a stock’s price. It involves buying more options than selling, creating a position with limited risk and potentially unlimited profit. But how does it work? When should you use a back spread instead of a simple debit spread? What makes a call ratio backspread bullish and a put ratio spread strategy bearish?

KEY TAKEAWAYS

- The back ratio spread is an advanced options strategy that combines long and short options in a specific ratio to create a trade with limited risk and potentially unlimited profit.

- You sell a smaller number of more expensive options and use the proceeds to buy a larger number of cheaper options, this can result in unlimited profit if the trade goes your way, while keeping the risk limited (and sometimes even creating a net credit).

- Risk and reward depend on structure, but most back ratio spreads offer a defined maximum loss and significant upside potential when executed correctly.

Understanding the Back Ratio Spread

A back ratio spread is an options strategy where traders buy more contracts than they sell, creating a trade with limited risk and the potential for unlimited profit. The goal is to capitalize on strong price movements in either direction while maintaining a controlled downside.

This back ratio spread typically follows a 2:1 or 3:1 ratio:

- Buying two or three options

- Selling one option at a different strike price

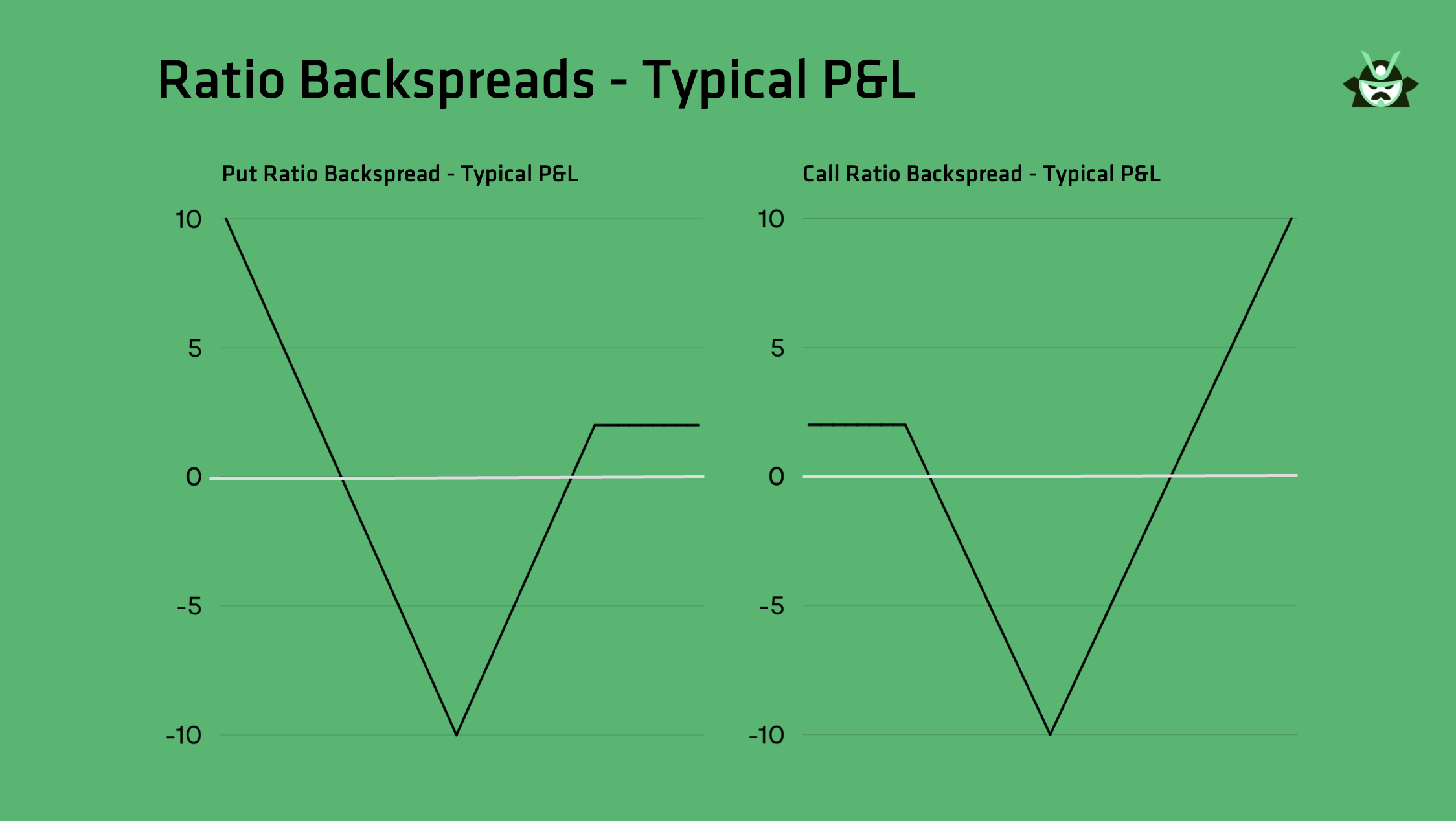

As we will explain to you in a minute, there are basically two types of back ratio spreads, the call and the put versions, with these P&L charts:

Since the trader holds more long positions than short ones, there is an asymmetry in risk and reward. If the stock moves in the expected direction, the extra long option benefits, offering significant profit potential.

How a Back Ratio Spread Works

Traders set up a back ratio spread by selecting options at different strike prices but with the same expiration date. The trade can be constructed using calls (call ratio backspread) for a bullish outlook or puts (put ratio spread strategy) for a bearish expectation.

- Call ratio backspread: Used when expecting a strong upward move. The trader buys more calls than they sell, ensuring unlimited upside.

- Put ratio spread strategy: Used when anticipating a sharp decline. More puts are bought than sold, maximizing profit potential on a strong drop.

Unlike a front ratio spread, where traders sell more contracts than they buy (increasing risk), a back spread prioritizes risk control while still allowing for substantial gains.

Why Traders Use a Back Ratio Spread

The main reason traders choose this back ratio spread is its ability to capitalize on volatility while limiting downside exposure. It works best when:

- The stock is expected to make a big move in one direction

- Implied volatility is rising, increasing option prices

- Traders want high profit potential with controlled risk

However, back ratio spreads require strong price movement to be profitable. If the stock stays flat, the trade may result in a small loss, making timing and market outlook crucial.

Pros and Cons of Ratio Backspreads

A back ratio spread can be a powerful options strategy, but like any trade, it has its advantages and drawbacks. Here’s a quick overview before diving into the details:

Pros | Cons |

Unlimited upside potential | Needs strong price movement to profit |

Lower cost than stock ownership | If you're right on direction but wrong on magnitude, losses can still occur |

Risk is limited to the debit paid | Can be complex for beginners |

Benefits from increased implied volatility | Difficult to manage if volatility drops |

Pros of a Back Ratio Spread

- Unlimited upside potential – The extra long option in a back spread creates a scenario where profits can keep rising as the stock moves in the right direction.

- Lower cost than owning stock – Instead of paying full price for 100 shares, traders can use a call ratio backspread or a put ratio spread strategy to get similar exposure at a fraction of the cost.

- Risk is capped – In most cases, the maximum loss is limited to the net debit paid to enter the trade, making it a defined-risk strategy.

- Volatility can work in your favor – A rise in implied volatility generally increases the value of the long options, helping the trade.

Cons of a Back Ratio Spread

- Requires strong movement to profit – If the stock stays flat, the trade can lose value due to time decay.

- Right direction, but not enough movement – Even if the stock moves as expected, the trade can still lose money if the move isn't large enough to overcome costs and time decay.

- Not beginner-friendly – The structure involves multiple strike prices and varying ratios, making it harder to understand and execute.

- Volatility risk – If implied volatility drops after entering the trade, the long options may lose value, reducing the trade’s effectiveness.

If you want to screen the market based on other strategies, you can visit our screener for options traders. You can also rely on our custom scan feature to find any trade, especially those you would not be able to find anywhere else online.

How the Back Spread Works

A back ratio spread is structured by buying more options than selling, creating a position with a limited downside and strong profit potential if the stock moves significantly. It is typically opened for a net debit, meaning traders pay upfront to establish the position. However, in some cases, it can be structured for a small net credit if the short option has enough extrinsic value to offset the cost of the long options.

Understanding the Setup

A back spread can be built using either calls (call ratio backspread) or puts (put ratio spread strategy), depending on whether the trader is bullish or bearish. The typical structure follows a 2:1 ratio, but 3:1 variations also exist:

- Call ratio backspread (bullish): Buy two OTM calls, sell one ATM call.

- Put ratio spread strategy (bearish): Buy two OTM puts, sell one ATM put.

Because more options are bought than sold, this structure creates asymmetry in risk and reward, offering unlimited profit potential in the right conditions.

Implied Volatility and Its Impact

Back spreads benefit from increased implied volatility, which raises the value of the long options. A spike in volatility before expiration can make the trade more profitable, even if the stock hasn’t moved significantly. On the other hand, a drop in volatility can reduce the value of the long options and hurt the trade.

Max Profit, Max Loss, and Breakeven Points

- Max profit: Since the trade includes an extra long option, there is no cap on potential gains if the stock moves strongly in the expected direction.

- Max loss: Occurs when the stock price settles near the short strike at expiration. It is calculated as the difference between the strikes (long – short) multiplied by the number of contracts minus any net credit received (or plus any net debit paid) when entering the trade.

- Breakeven points: These depend on the strike prices selected and the debit or credit received. The further the stock moves, the higher the potential for profit.

In the next sections, we’ll break down specific ways to build a back spread, looking at both bullish and bearish variations.

Call Ratio Backspread: The Bullish Strategy

A call ratio backspread is a bullish options strategy that profits when the stock price moves significantly higher. It is structured by selling a smaller number of at-the-money (ATM) calls and buying a greater number of out-of-the-money (OTM) calls, giving traders a way to capitalize on a strong upward move while keeping risk limited. If you remember, we talked about this strategy at the end of our call ratio spread article.

How It’s Structured

The typical call ratio backspread consists of:

- Selling one ATM call option – This helps reduce the overall cost by collecting premium.

- Buying two OTM call options – These provide unlimited upside potential if the stock rallies.

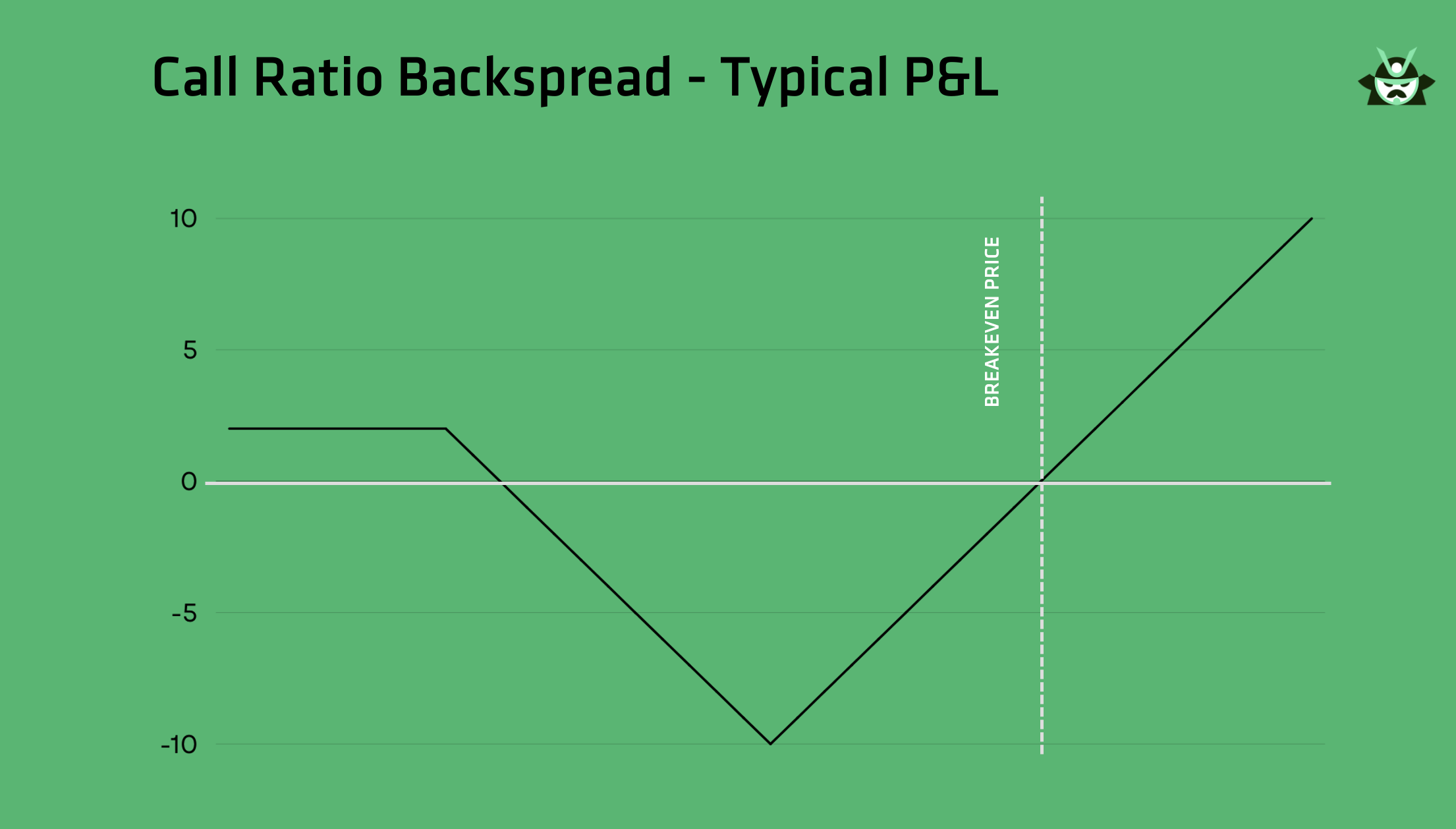

This is the typical P&L of a call ratio backspread (in case you collected the premium):

Since more options are bought than sold, the payoff structure has uncapped profit potential on the left if the stock drops. On the right, there is a small capped loss, which can sometimes turn into a small capped profit depending on how the strikes are selected, effectively removing upside risk. The trade forms a downward triangle in the middle, where losses may occur if the stock remains near the long strike at expiration.

Risk and Reward

- Max profit: Unlimited if the stock continues moving upward.

- Max loss: Occurs if the stock finishes at or near the strike of the long calls at expiration. It is calculated as the difference between the strike prices (long – short), multiplied by the number of contracts, minus any net credit received (or plus any net debit paid) when entering the trade.

- Breakeven points: The stock must rise beyond a certain level for the trade to become profitable. (Or stay below the short leg, if strategy was traded for a credit)

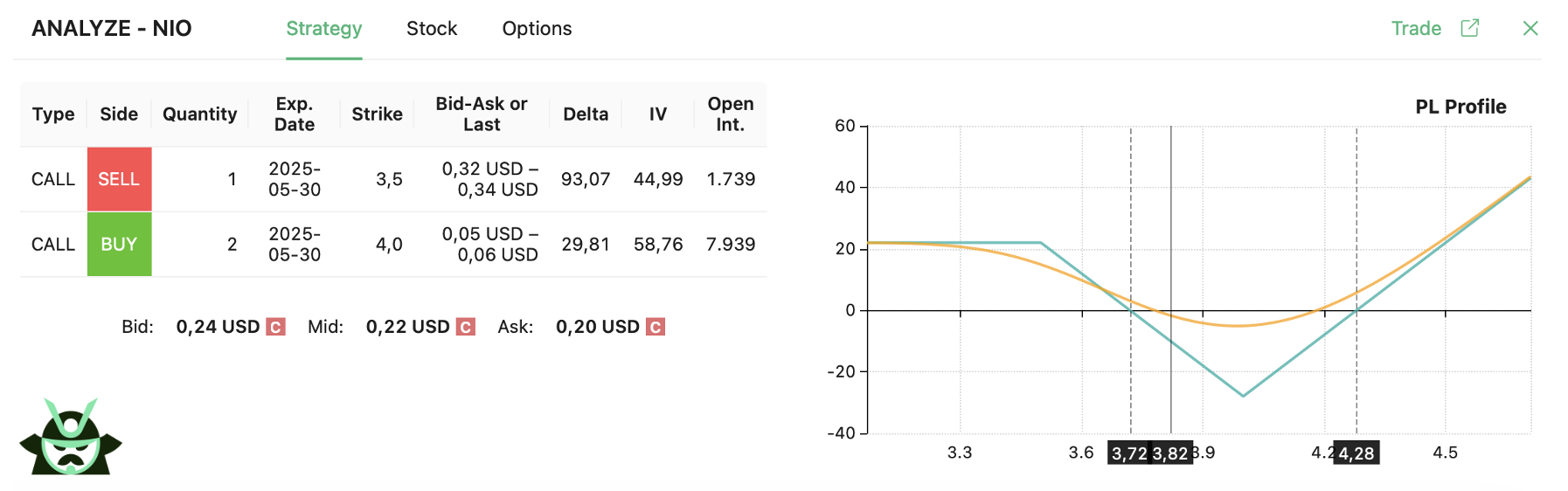

Example Trade - Call Ratio Backspread

Here’s a trade found using our custom scan feature. The underlying is NIO, currently trading near $3.82. The trade is structured as follows:

- Sell one NIO 3.5-strike call expiring in one week

- Buy two NIO 4.0-strike calls expiring in one week

The strategy P&L chart is the following:

Notice that your maximum loss is capped and it occurs when NIO is at $4 at expiration, while you have an uncapped profit potential above $4.28 and a capped profit below $3.5. If you're looking for a more straightforward bullish setup with defined risk and capped reward, the bull call spread strategy offers a simpler alternative, especially for newer traders who want to limit complexity.

Put Ratio Backspread Strategy: The Bearish Approach

A put ratio backspread strategy is used by traders who expect a strong downside move in the underlying asset. It is structured by selling a smaller number of at-the-money (ATM) puts and buying a greater number of out-of-the-money (OTM) puts, creating a position with unlimited profit potential if the stock drops significantly, while keeping risk limited. Just as mentioned earlier for the call version, we talked about this strategy at the end of our put ratio spread article on the blog.

How It’s Structured

The typical put ratio backspread consists of:

- Selling one ATM put option – This helps offset the cost by collecting premium.

- Buying two OTM put options – These provide significant profit potential if the stock declines sharply.

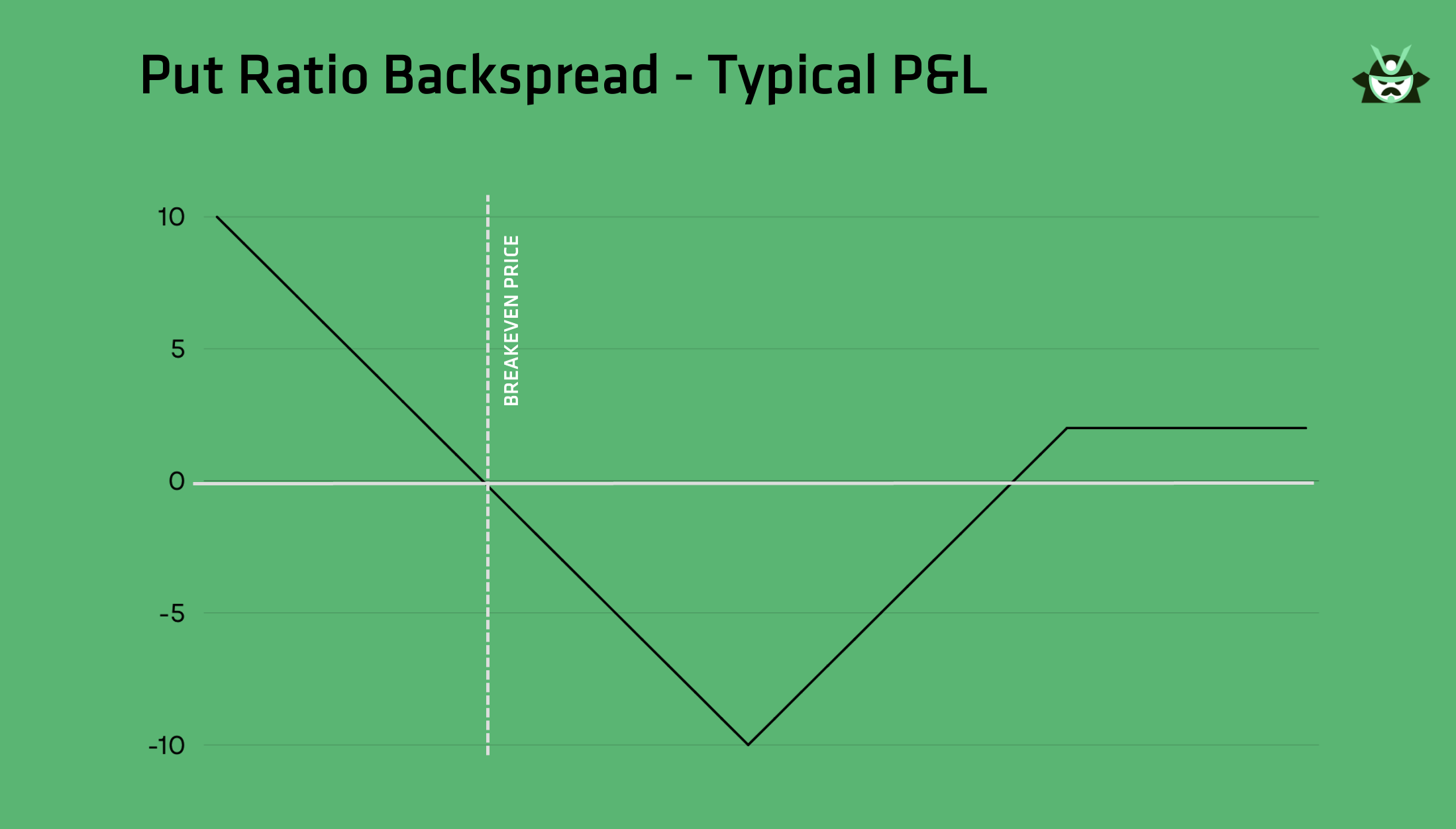

This is the typical P&L of a put ratio backspread (in case you collected the premium):

Since more options are bought than sold, the payoff structure has uncapped profit potential on the left if the stock drops. On the right, there is a small capped loss, which can sometimes turn into a small capped profit (like in our P&L above) depending on how the strikes are selected, effectively removing upside risk. The trade forms a downward triangle in the middle, where minor losses may occur if the stock remains near the short strike at expiration.

Risk and Reward

- Max profit: Unlimited if the stock experiences a sharp decline.

- Max loss: Occurs if the stock finishes at or near the strike of the long puts at expiration. It is calculated as the difference between the strike prices (short – long), multiplied by the number of contracts, minus any net credit received (or plus any net debit paid) when entering the trade.

- Breakeven points: The stock must fall below a certain level for the trade to become profitable. (Or stay above the short leg, if the strategy was traded for a credit)

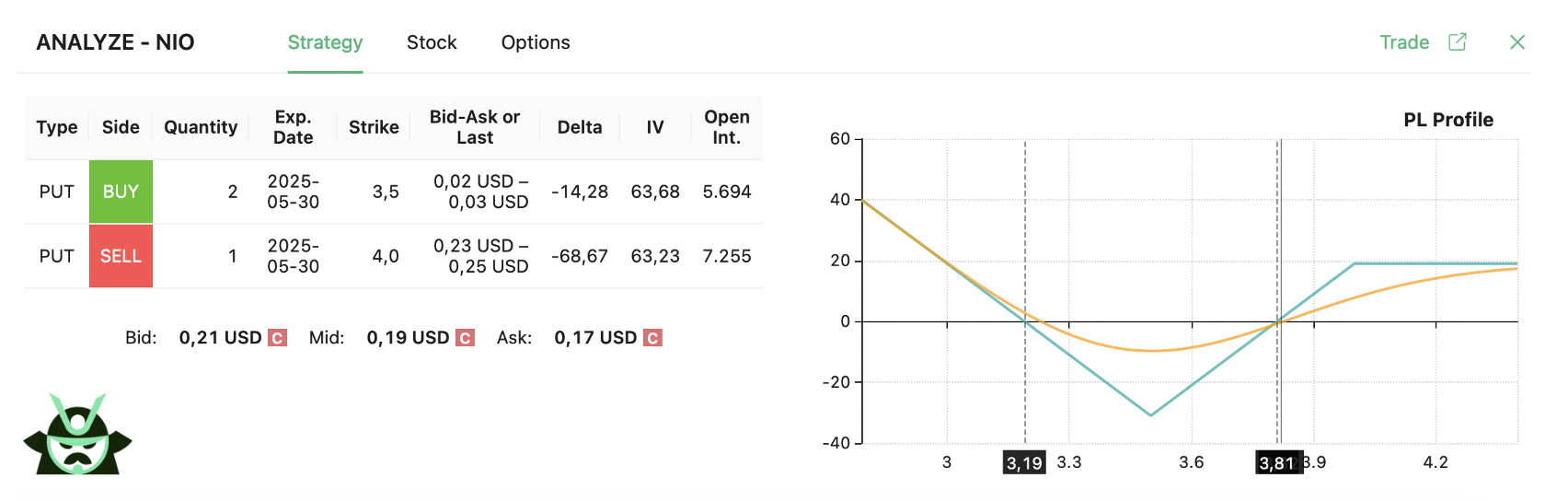

Example Trade - Put Ratio Backspread

Here’s another setup found using our custom scan feature. The underlying is, once again, NIO. The trade is structured as follows:

- Buy two NIO 3.5-strike puts expiring in one week

- Sell one NIO 4.0-strike put expiring in one week

The strategy P&L chart is the following:

As shown in the chart, your profit is uncapped below $3.19, while above $4.0 you keep a small capped profit. The area of maximum risk is around $3.5 at expiration. If you prefer a defined-risk bearish position rather than a complex ratio setup, the bull put spread strategy can serve as a cleaner alternative.

In the next section, we’ll look at the ZEBRA strategy, a variation of the back ratio spread that offers stock-like exposure with lower risk.

Special Case: The ZEBRA Strategy

The ZEBRA strategy (Zero Extrinsic Value Back Ratio Spread) is a unique variation of the back ratio spread that removes extrinsic value, making it a cost-efficient way to replicate stock ownership. Unlike a standard call back ratio spread or put ratio spread strategy, the ZEBRA options strategy aims for near-100 delta exposure, meaning it behaves similarly to holding 100 shares of stock, without the same capital requirement or risk. Since the ZEBRA structure builds upon the same foundations as a vertical spread, it gives traders similar directional exposure with tighter control over risk.

How the ZEBRA Strategy Works

A ZEBRA is built using the back spread framework but adjusted to eliminate extrinsic value. It follows a simple 2:1 structure:

- Call ZEBRA (bullish): Buy two ITM calls and sell one ATM call

- Put ZEBRA (bearish): Buy two ITM puts and sell one ATM put

By selling the ATM option, the trade removes extrinsic value, leaving only intrinsic value in the position. This results in a strategy that closely mimics stock ownership, while limiting the maximum loss to the debit paid.

Why Use a ZEBRA?

- Mimics stock exposure – Traders can gain near-100 delta without the full capital outlay.

- Limited downside risk – Unlike holding shares outright, the max loss is capped at the initial debit.

- No margin requirements – Since no shares are bought or sold, margin requirements are lower than traditional stock trading.

- More efficient than married strategies – Similar to a married put or married call, but without extrinsic value costs.

This back ratio spread is ideal for traders looking to take directional positions while maintaining risk control. In the next section, we’ll discuss when to use a back ratio spread and how to apply these strategies in different market conditions. Understanding how an options market maker behaves when quoting and filling ratio spreads is also important. Liquidity, slippage, and pricing dynamics can shift your trade outcome, especially in multi-leg strategies. For another multi-leg setup that locks in defined profits through arbitrage, explore the box spread.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.