Black and Scholes Option Pricing Model - The Benchmark Behind Option Prices

Published on February 23, 2026 | 8 min readReviewed by Leav Graves

The Black and Scholes option pricing model sits behind prices traders see. If you trade European options, it shapes value through price, time, and volatility. This article will cover the Black and Scholes method, inputs, option pricing model formula, and more.

KEY TAKEAWAYS

- The Black and Scholes option pricing model is a mathematical framework used to estimate the fair value of European options based on price, time, volatility, and interest rates

- American options - i.e. those that can be exercised earlier than the expiration date - rely on the Binomial model rather than the Black & Scholes

- The model relies on clear assumptions such as constant volatility and no early exercise, which makes it powerful but imperfect

- Traders and analysts use the model as a pricing benchmark, risk management tool, and foundation for more advanced option models

What Is the Black and Scholes Option Pricing Model?

The Black and Scholes option pricing model is a structured way to estimate what a European option should be worth, using a small set of observable inputs like price, time, volatility, and interest rates. Its goal is not to predict where a stock will go, but to assign a fair value to an option given today’s conditions.

The model was developed in the early 1970s by Fischer Black and Myron Scholes, with key mathematical extensions by Robert Merton. Before their work, option pricing was mostly based on rules of thumb and loose comparisons. What made this approach different, and disruptive at the time, was that it linked option prices to a clear probabilistic framework. For the first time, traders had a common reference point instead of relying only on intuition or past trades.

At its core, the Black and Scholes method treats price movements as random but measurable. By assuming a specific behavior for prices and volatility, the model turns uncertainty into something that can be priced. This idea is embedded in the Black and Scholes option pricing model formula, which balances the expected upside of the underlying asset against the discounted cost of exercising the option later.

Applying the Black and Scholes Option Pricing Model

The model is designed specifically for European-style options, meaning options that can only be exercised at expiration. It applies to both calls and puts. The call price comes directly from the main formula, while put values are obtained either through the Black and Scholes put option formula or via put-call parity. American options, which allow early exercise, fall outside the model’s scope.

In practice, traders and analysts rarely calculate prices by hand. Instead, the Black and Scholes inputs are fed into platforms, option screeners, and spreadsheets to produce theoretical values and Greeks. Typical uses include:

- Comparing market prices to theoretical prices to spot potential arbitrage opportunities

- Measuring sensitivity to volatility and time decay

- Stress-testing positions under different scenarios

What the Black and Scholes option pricing model does well is consistency. It gives everyone the same baseline. What it does not try to do is describe real market behavior in full detail. Volatility is assumed constant, dividends are simplified, and sudden price jumps are ignored (which is why at some point, Merton extended the model to deal with these jumps). That gap between theory and reality is not a flaw, it is the reason the model is used as a benchmark rather than a trading signal.

Think of it as a ruler. It does not tell you where to trade, but it helps you measure whether a price looks rich, cheap, or fairly aligned.

Why is the Black and Scholes Method so Relevant for Options Traders?

For traders, the value of the Black and Scholes option pricing model comes from how it turns uncertainty into something measurable. The Black and Scholes method starts from a simple idea: prices move in a random way, but that randomness follows patterns that can be modeled. You do not need to guess the direction, you need to price risk.

The model treats price changes as a random process with a known distribution. That sounds abstract, but the payoff is practical. Once price behavior is framed this way, uncertainty can be translated into probabilities. Those probabilities sit inside the Black and Scholes option pricing model formula and drive the final option value. This is how our screener and most brokers show you the probability of an option to expire worthless, for instance.

A key step is risk-neutral valuation (which is also the logic behind strategies like the fiduciary call). In plain terms, the model assumes traders are indifferent to risk when pricing options, as long as they are paid at the risk-free rate. This removes opinions and emotions from the equation. Under this view, the expected payoff of an option is discounted back to today using interest rates, not forecasts. That is why the Black and Scholes option pricing model focuses on fair value, not on market direction.

The Time and Uncertainty Factors

Time and uncertainty are handled together. Time matters because the longer an option lives, the more chances the price has to move. Uncertainty matters because wider price swings increase the odds of a profitable outcome. These effects are captured through the Black and Scholes inputs, especially time to expiration and volatility. Change those inputs and the option price moves, even if the stock price stays the same.

Traders rely on this logic in several ways:

- Comparing market prices to theoretical values

- Understanding how much of an option’s price is time value

- Measuring sensitivity to volatility changes

- Structuring trades with defined risk

The same framework applies to puts. Whether using the Black and Scholes put option formula directly or put-call parity, the logic stays consistent.

The reason this matters is simple. The Black and Scholes option pricing model does not tell you what will happen next. It tells you how likely different outcomes are and what those odds should cost. That shift from prediction to probability is why the model remains a core reference for options traders.

Black and Scholes Inputs

Everything the Black and Scholes option pricing model produces comes from a small set of inputs. Change one of them and the option price changes, even if nothing else moves. That is why understanding the Black and Scholes inputs matters more than memorizing the Black and Scholes option pricing model formula.

At a high level, the model uses six inputs:

Input | What it represents |

Volatility | Expected size of price moves |

Underlying price | Current price of the stock or asset |

Strike price | Price at which the option can be exercised |

Time to expiration | Time left until expiry |

Risk-free interest rate | Baseline return over the same period |

Option type | Call or put |

Volatility is the most influential input. Higher volatility increases option prices because it widens the range of possible outcomes, something especially visible in currency option trading where FX volatility drives premiums directly. In practice, this is usually implied volatility (or “IV”), backed out from market prices, not a forecast. This is why volatility often drives pricing more than direction.

The underlying price sets the starting point. A call becomes more valuable as price rises, while a put gains value as price falls. The strike price defines where the payoff begins. The distance between price and strike helps determine how much of the option is intrinsic value versus time value.

Time to expiration matters because time creates opportunity. More time means more chances for price to move, which increases option value. As time passes, this benefit fades. The Black and Scholes method captures this effect directly, which is why time decay shows up clearly in option pricing.

The risk-free interest rate plays a smaller role, but it still matters. It is used to discount future payoffs back to today. When rates rise, call prices tend to increase slightly, while put prices tend to decrease, which is reflected in both the Black and Scholes option pricing model formula and the Black and Scholes put option formula.

Finally, the option type tells the model which payoff structure to apply. Calls and puts use the same framework, but with different probability weightings.

For traders, these inputs explain why option prices move even when the stock does not. If volatility spikes, time decays, or rates shift, the Black and Scholes option pricing model reacts immediately. That is the real value of the model, it shows what is driving price changes under the surface.

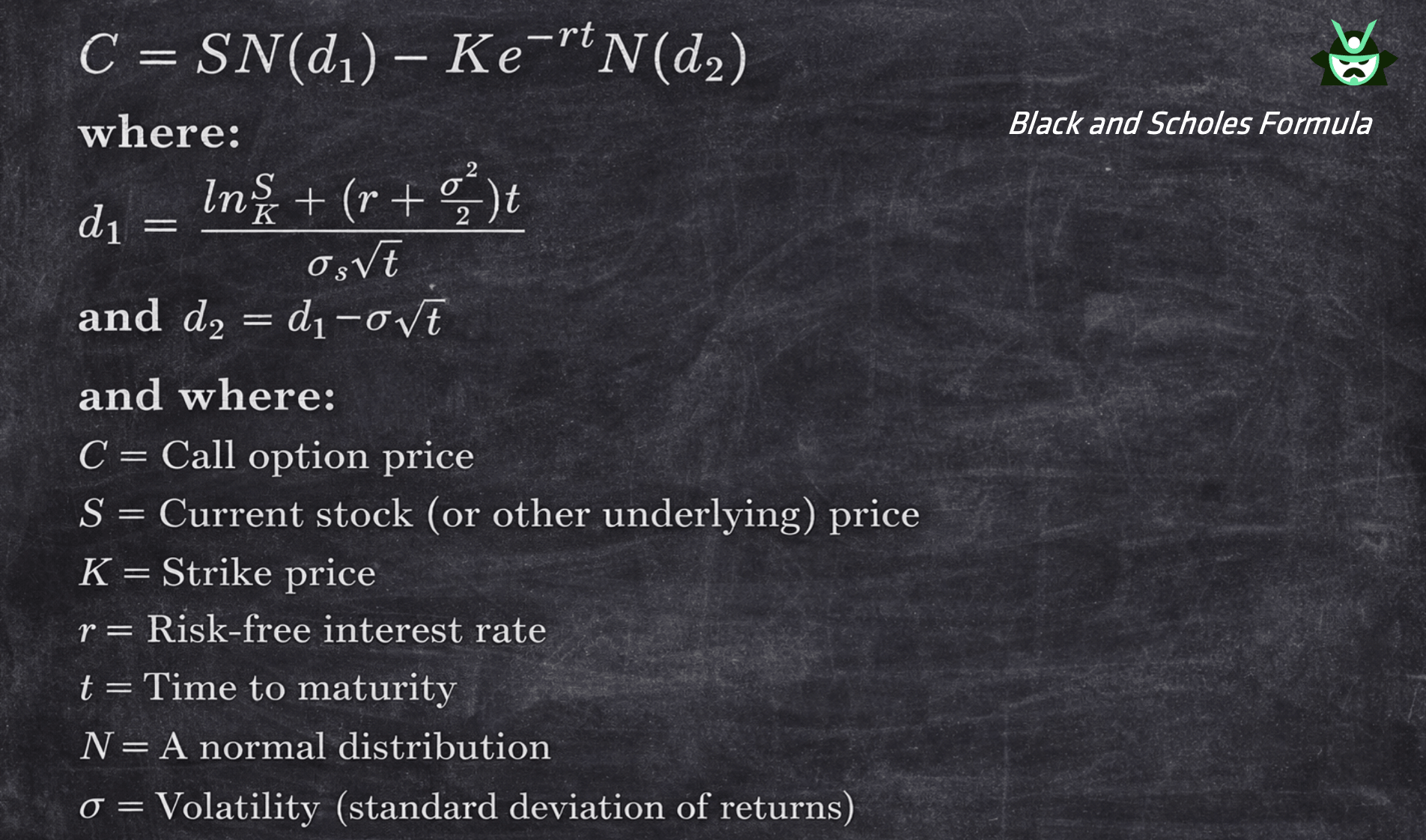

Black and Scholes Option Pricing Model Formula

The formula is where the Black and Scholes option pricing model turns theory into a number. At first glance it looks heavy, but the logic behind it is simple. The Black and Scholes option pricing model formula is generally written as follows:

The formula prices a call option by combining the expected benefit of owning the underlying asset with the present cost of exercising the option later.

Conceptually, the Black and Scholes option pricing model formula splits the option into two pieces. One part represents the value of potential upside if the stock finishes above the strike. The other part represents the cost of paying the strike price in the future, discounted back to today. The option price is the difference between those two values.

The probability terms inside the formula come from the normal distribution (which is why you see an “N” in the formula above). These terms answer practical questions, not predictive ones. They estimate how likely it is that the option expires in the money under the model’s assumptions. This is why the Black and Scholes method works with probabilities rather than forecasts. You are not guessing direction, you are pricing odds.

Each element of the formula maps directly to the Black and Scholes inputs. Price and strike define where the option sits today. Time and volatility define how wide the range of possible outcomes is. The risk-free rate adjusts future cash flows back to present value. Put together, these inputs allow the formula to balance opportunity against cost.

The Black and Scholes Model Made Simple

A simple way to think about the call option formula is this:

- The stock price is weighted by the probability of finishing above the strike

- The strike price is discounted and weighted by a related probability

- The difference between the two gives the call value

As time increases or volatility rises, those probabilities shift, which is why option prices change even when the stock does not move.

The same structure applies to puts. The Black and Scholes put option formula uses the same inputs and probability logic, just with the payoff flipped. Many traders rely on put-call parity instead of calculating puts directly, but the pricing logic stays consistent across both.

In practice, traders almost never compute the formula by hand. The math is exact and small input changes can materially affect results. Instead, platforms, scanners, and spreadsheets handle the calculations instantly using the Black and Scholes option pricing model. This allows traders to focus on what matters:

- How expensive volatility is

- How much time value remains

- Whether market prices look rich or cheap

The formula itself is not a trading signal. It is a measuring tool. Once you understand what it is measuring, you can use it to make faster and more informed decisions.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.