Covered Straddle - How It Works and When to Use It

Published on May 12, 2025(Last updated on January 30, 2026)

Reviewed by Leav Graves

A covered straddle strategy can generate income by combining stock ownership with short options. In this setup - also known as a covered short straddle - you own the stock while simultaneously selling a call and a put at the same strike. But is this approach worth the risk? Learn how it works and when to use it.

KEY TAKEAWAYS

- The covered straddle strategy combines long stock ownership with a short call and a short put to generate premium income but exposes traders to significant downside risk.

- This strategy profits if the stock price remains stable or slightly increases but has limited profit potential and virtually unlimited losses that accelerate as the stock falls below the breakeven price.

- The strategy can also be used for long-term stock accumulation, collecting premiums and dividends while averaging down, but requires strong conviction in the stock’s bullish scenario.

What Is a Covered Straddle?

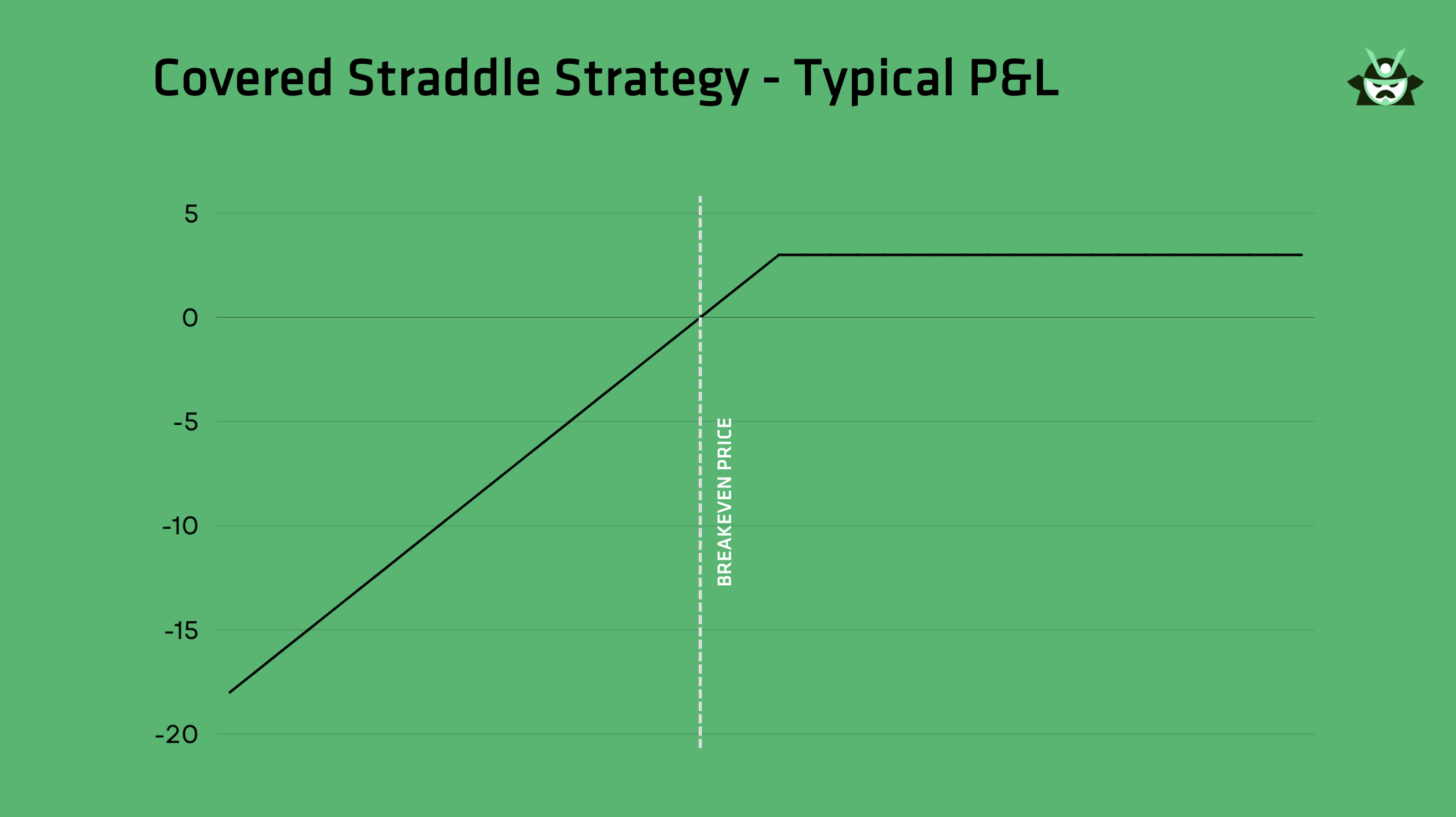

A covered straddle combines owning 100 shares of stock with selling an at-the-money (ATM) call and an ATM put, both with the same strike price and expiration date. This strategy, also called a covered short straddle, aims to generate income from the premiums of the options you sell. However, it carries significant risks, as you can see from the typical profit and loss (P&L) chart of the covered short straddle strategy below:

Key characteristics of a covered straddle include:

- Premium income from selling both the call and put.

- Limited profit potential when the stock price rises above the strike price.

- Unlimited downside risk, as losses accelerate quickly if the stock price falls below the breakeven point.

The breakeven is calculated by taking the stock’s purchase price minus the total premiums collected. Losses can mount rapidly, often doubling compared to a covered call strategy. For every $1 decline below breakeven, losses grow by $2 per share, your owned stock loses value while the short put incurs additional losses.

As an example, you could imagine the following case:

- Buy 100 shares of XYZ at $120

- Sell 1 XYZ 120 Call at $4.50

- Sell 1 XYZ 120 Put at $4.35

The covered short straddle works best in stable markets or when stock prices stay slightly above breakeven. But traders should approach it cautiously, given the downside risks and complexity of managing open positions.

Maximum Profit, Maximum Risk & Breakeven

Having explained what the covered straddle strategy is, we can dig a bit deeper into its key features, including its profit potential, risks, and breakeven calculation. Understanding these factors is essential for evaluating if this approach fits your trading objectives.

Maximum Profit

The profit potential of a covered straddle (as you can see with the custom scan feature on our screener for options) is capped at the total premiums you receive when you sell call and put options. Let's go back to our previous example:

- Stock purchase price: $120

- Premiums received: $4.50 (call) + $4.35 (put) = $8.85

If the stock price equals the strike price at expiration, there are no gains or losses from the stock. The maximum profit is capped on the right-hand side of your trade, as you can see from the P&L above.

This capped profit highlights that most of the earnings come from premiums, not stock price movement.

Maximum Risk

The downside risk of a covered short straddle is significant. Below the breakeven point:

- For every $1 stock price drop below breakeven, the loss increases by $2 per share.

- Losses come from both declining stock value and the short put option.

The worst-case scenario? The stock drops to zero, resulting in massive losses from your long stock holding and short put.

Breakeven Price Calculation

To calculate the breakeven point for a covered straddle, you need to account for the fact that on the downside, losses come from both your long stock and the short put. This effectively creates double downside exposure - it’s like being long 100 shares and simultaneously agreeing to buy another 100 if the stock drops.

Because of that, the premium you collect from selling both the call and the put doesn’t protect you dollar-for-dollar on the way down. Instead, losses accelerate at twice the rate below the strike, so your premium “lasts” only half as long.

Example:

- Stock purchase price: $120

- Total premiums collected: $8.85 ($4.50 call + $4.35 put)

- Breakeven price = $120 – ($8.85 ÷ 2) = $115.58

In other words, for every $1 the stock drops below the strike, your losses increase by $2 - so the $8.85 in premium only offsets a $4.42 drop. That’s why the breakeven sits at $115.58, not $111.15 like it would in a simple short put.

Staying above this level is key - below it, your losses can accelerate fast. This makes the covered short straddle a strategy best suited for traders who fully understand the downside mechanics and have a clear plan for managing risk.

Example Trade – Covered Straddle

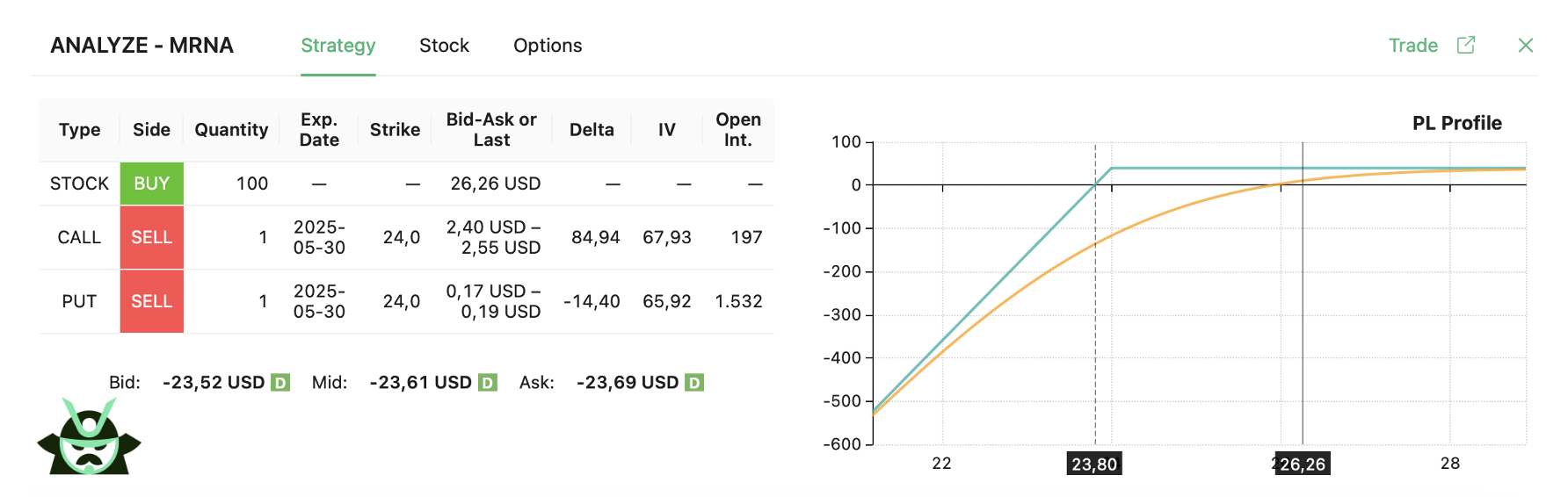

Here’s a real-world example found using our custom scan feature—something you won’t find on most platforms. The underlying stock is Moderna (MRNA), currently trading at $26.26. The trade is structured as follows:

- Buy 100 shares of MRNA at $26.26

- Sell 1 MRNA $24 call expiring in one week

- Sell 1 MRNA $24 put expiring in one week

This creates a covered short straddle with short options positioned at the $24 strike, with the following P&L chart:

As the P&L chart shows, your maximum profit is capped below $40, which occurs if MRNA closes at $24. Meanwhile, the breakeven is around $23.80, and losses begin to accelerate quickly if the stock falls below that level.

This type of setup - available through our scanner - helps you uncover advanced opportunities with specific risk-reward profiles that are nearly impossible to surface manually.

Why Trade a Covered Straddle?

Let's go a little bit beyond the technicalities and ask ourselves: "Why trade a covered straddle?" Keep in mind that you don't necessarily have to use the covered short straddle strategy and, in fact, this is far from our favorite options setup. In fact, while we can tolerate having a part of our portfolio exposed to unlimited loss risk, we’d normally give higher preference to a simpler strategy like the naked put to achieve a similar goal (assuming we’re not interested in owning the stock immediately). Remember, a covered straddle consists of owning stock while selling both a call and a put, with all the pros and cons that come with this approach.

When Is a Covered Straddle Useful?

We can think of at least two situations in which a covered straddle may be useful:

- Neutral-to-slightly bullish outlook: A covered straddle works best if you expect the stock to stay stable or rise modestly above breakeven.

- High implied volatility (IV): When IV is elevated, option premiums are higher, making the covered short straddle more attractive.

Risks to Consider

There are, however, some obstacles to consider before trading the covered straddle:

- Magnified downside exposure: Losses are amplified compared to a simple covered call. Both the declining stock price and the short put can create losses.

- No cash collateral for the short put: This leaves you exposed to margin calls if the put is assigned at unfavorable prices.

Strategy Considerations

While the potential for reward exists, the risks are substantial - making the covered short straddle srategy best suited for experienced traders who can manage volatility and downside pressure effectively. Proper timing and market analysis are essential for success.

Discipline is critical when managing a covered short straddle. If the stock price moves against you, cutting losses promptly is vital to prevent significant damage. You also need to monitor margins closely to avoid liquidation risks. Some traders prefer a hands-off approach, using a covered call ETF to automate the income process while keeping downside exposure limited.

Choosing a broker that offers tight spreads and advanced risk tools (like those compared in our Tastytrade vs Interactive Brokers review) can make this easier to manage.

Impact of Stock Price, Volatility & Time

Next, you should know that there are several factors that can significantly impact the profitability and risk of a covered straddle, including stock price movements, volatility, and time decay. Here’s how these elements influence the strategy:

Impact of Stock Price Changes (Delta)

Delta measures how much a position’s value shifts with stock price changes. For a covered straddle, the combined delta falls between +0 and +2, depending on where the stock price stands relative to the strike price:

Scenario | Delta Behavior | Explanation |

Near the strike price | Around 1 | Long stock (+1) and a balance between the short call (-0.5) and the short put (+0.5). |

Above the strike price | Decreases toward 0 | Long stock offsets the short call. Short put delta approaches 0. |

Below the strike price | Increases toward +2 | Long stock and short put both contribute a positive delta, while the effect of the short call decreases. |

Impact of Volatility

Volatility plays a big role in the success of a covered straddle. Since you’re selling both a call and a put, you want option prices to go down after entering the trade.

- If volatility decreases → option premiums shrink → you can buy them back cheaper or let them expire worthless → this is good

- If volatility increases → option prices rise → your short positions become more expensive → this is bad

That’s why covered straddles work best when you expect volatility to fall, not rise. Entering the trade during periods of high implied volatility can give you an edge, but only if that volatility drops afterward.

If you're comparing this setup with a purely neutral volatility trade, our guide on the straddle option strategy explains how a stock-free straddle behaves when implied volatility rises or falls.

Impact of Time Decay

Time decay is a covered straddle’s friend since both options are short positions. As expiration nears, the time value of the options erodes, benefiting the trade if the stock remains near the strike price. This effect accelerates in the last few weeks before expiration, offering a potential double advantage through rapid value decay. If you're evaluating the trade-offs between premium income and directional exposure, reviewing how the covered call strategy works can provide a useful benchmark.

Assignment & Expiration Risks

The last matter we'd like to mention is the assignment and expiration risks associated with a covered straddle. Knowing how these risks play out helps avoid surprises and manage your positions effectively.

Short Call Assignment Risk

- Early assignment: Short calls in a covered straddle can be exercised early, especially the day before the stock’s ex-dividend date. If assigned, the stock is sold at the strike price, locking in a profit.

- Avoiding assignment: If holding the stock is your priority, you can buy back the short call before the ex-dividend date.

Short Put Assignment Risk

- Possibility of assignment: Short puts are at risk of being assigned any time they’re in-the-money. Assignment means you’ll have to purchase additional shares at the strike price, effectively doubling your exposure.

- Covering margin needs: Ensure your margin can handle the added stock position, or you'll face a margin call.

Expiration Considerations

- Market movements: Sudden price swings near expiration can push short options in-the-money, triggering assignment.

- Closing positions early: To reduce risks, it’s often wise to close your short call and put options before expiration if the stock price is hovering near the strike price. Using GTD orders (Good 'Til Date) can help automate this process, giving you better control over trade duration and exit timing.

By managing these risks, you can better handle the challenges of trading a covered straddle.

Advanced Application: the Long‑Term Accumulation Covered Straddle

Some traders use a covered straddle not only for premium income but also as a way to deploy idle capital while seeking to accumulate shares at a discount. The logic is simple:

- Buy (or already own) 100 shares of a stock you like at today’s price.

- Sell one ATM straddle dated far enough out (12–18 months is common) so that, if assigned, the holding period on the shares can qualify for long‑term capital‑gains tax treatment.

- Collect three cash flows up front:

- The call premium

- The put premium

- Any dividends paid while you hold the shares

As an example, let’s take into account Target (TGT):

- Current price: $96.37

- Jun 18 2026 $100 call bid ≈ $14.10

- Jun 18 2026 $100 put bid ≈ $20.20

- Annual dividend: ≈ $4.48 (yield ≈ 4.6 %)

Selling that straddle against 100 shares provides ≈ $34.30 in option premium today, which is about 36% of the share price plus four dividend payments totaling roughly $4.48. If TGT finishes above $100 at the June‑2026 expiration, the stock is called away and the trader keeps the premiums, the dividends, and a $3.63 capital gain on the shares, for a total return of roughly 44% on capital deployed (where, by “capital deployed,” we refer to the money you invested in the 100 shares).

Under OCC margin guidelines, the short put ties up about $3,584, 20 % of the underlying value (20 % × $96.37 × 100) minus its out-of-the-money amount (($100 – $96.37) × 100) plus the $2,020 option credit, so total funds at risk sum to roughly $13,221 ($9,637 cash for shares + $3,584 margin).

If, instead, TGT finishes below $100, the put assignment adds another 100‑share lot at an effective cost of $100 strike minus $34.30 premium collected, which equals $65.70.

Combining the original 100 shares at $96.37 with the new 100 shares at $65.70 results in a blended cost basis of about $81.04 per share, which is around 16 % beneath the initial purchase.

Screening for candidates

When evaluating stocks for this approach, you may want to focus on:

- Rich long‑dated ATM straddle premium as a percentage of share price (e.g., ≥ 20%).

- Sustainable dividend yield, since a steady cash component cushions short‑term price drift.

- Robust balance sheet and sector outlook, meaning you must be willing to own more shares if the price declines.

Keep margin tolerances front‑of‑mind. The strategy is compelling only if your account can absorb successive assignments without forcing an untimely liquidation.

Note that, because each put assignment hands you an extra 100 shares, many traders respond by hedging the new lot, either with a covered call or by selling a fresh ATM straddle. That keeps the position hedged but also doubles both share count and short-option exposure; a second assignment forces the same decision again, driving the position size to 2 to the n-th power lots after n assignments. Without a firm recovery thesis and ample margin, this compounding can quickly outrun risk tolerance.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.