Implied Volatility backtest - Predicting IV Change

Published on October 1, 2020(Last updated on March 20, 2026)

By Leav Graves

[We have just added another article in the series, about the Real Volatility (or Historical Volatility) backtest. Check it at Implied Volatility Backtest 2: Predicting RV Change]

We've often claimed that IV is one of the most important concepts to understand in options trading. IV is a measure if an option is expensive or cheap. The reason this is important is that volatility (and implied volatility) is mean-reverting. This means that after high volatility, we can expect lower volatility, and vise versa - after a period of low volatility, we can expect increased volatility.

To help you know if IV is low or high, we use the IV percentile (we call it rank). If the IV rank is high, we can expect the IV to decrease, and if the IV is low, we can expect the IV to increase. You can read more about the Implied Volatility Percentile in our complete guide.

We have run backtests to prove and measure this point since 2014, and we have updated them since then. It's been a while since we last updated those backtests. Since 2020 was unique, and we also saw a period of unprecedented low volatility before that (during 2019), we thought it would be an excellent time to update and check on the backtest.

The backtest will include data on the IV percentile vs. the IV from 2015 till October 2020 (almost six years).

Backtest IV on stock indexes

The table you see below summarizes the relations between IV percentile and the FUTURE iv change. Each row was the result when the IV percentile was above or below the threshold. Each column indicates the change the IV saw over the average in the next 5,10,20 or 30 TRADING days. This corresponds to a week, two weeks, about a month, and ~45 calendar days.

Example of how to read it: In the table above, you see that when the SPY IV percentile (correlates to the VIX) was above 90%, the IV decreased in the next month by 16.76% compared to the average IV change (SPY table, row >90, column 20 days).

Similarly, the IWM saw an increase in IV in the next two weeks following IV rank was below 10%. The change was 7.31% more than the average IV change over 'normal' two weeks (IWM table, <10 rows, column 10 days)

From this table, we can see that the IV behaves as we expect it to act: it tends to decrease after a high IV percentile and tends to increase after a low IV percentile. This is even more effective as we look at the longer time frames.

However, We can say that the IV shows us a degree of short-term momentum behavior, but longer-term is mean-reverting behavior. This is because of the recent low IV events during market highs (VIX reached 8%!) and high IV during the COVID crush.

For example, if we look at IWM, we can see that when IV rank was high: >50, IV tended to decrease after that. However, when IV rank was extremely high: >90, IV decreased less than it did when the IV rank was >50. As we said - This is due to the extreme environment we had over the last couple of years. Still - the direction is clear.

Key takeaway: IV percentile (we call it rank) is a very reliable indicator on stocks. While it does not guarantee profits, it increases our edge when we trade with the indicator.

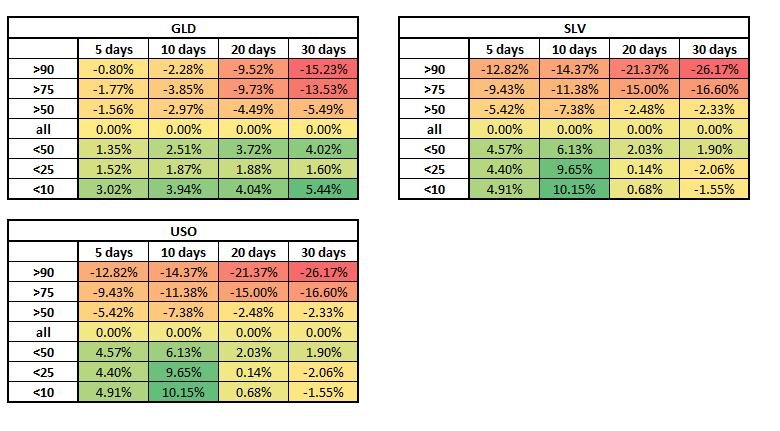

Backtest IV on commodities ETFs

We also ran the backtest on GLD (Gold ETF), SLV (Silver ETF), and USO (Oil ETF) to see if we can see the same behavior in commodities:

As you can see - the indicator behaves as expected on commodities as well: After a period of high IV, we can expect a period of lower IV, and after a period of low IV, we can expect higher IV, which is great if you like the idea of trading implied volatility. This time, we can say that it is more effective in shorter time frames (about 2 weeks) and for IV rank. It is important to remember that USO reached negative oil prices during the COVID-19 crash, so we can understand the divination.

Key takeaway: The IV percentile indicator is a reliable indicator on commodities ETFs as well, more effective in the 2-week time-frame.

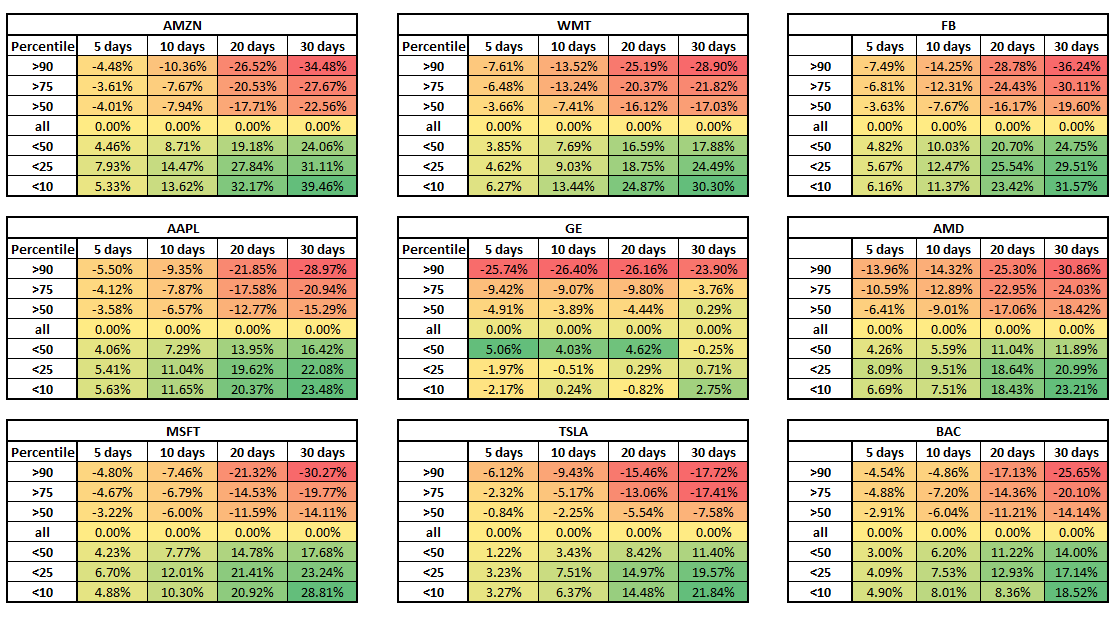

Backtest IV on popular stocks

We also ran tests on some of the most popular stocks (if you have a favorite stock, let us know, and we will run it for you).

When testing individual stocks, we can see that the mean-revision effect is, even more, emphasized, and we can see a direct link between how extremely high (or low) the IV percentile is to how strong the IV will decrease (or increase). Again, we see that this indicator is more effective on more extended time frames.

GE is a notable example where the extremely low IV has less effect. We can still see the expected behavior of the IV, but it is less strong in the low IV percentile. We can explain it when we remember that GE dropped from around $30 per share to $6, and this extreme movement affected the IV percentile indicator.

You can read our summary about The Edge of Implied Volatility Percentile here.

Summary

In this article, we summarized the effect of the IV percentile indicator on future IV changes. We can see a very consistent behavior of mean revision: When IV rank is high, we can expect future IV to decrease, and when IV rank is low, we can expect future IV to increase. However, we have to remember that extreme conditions in the asset (such as negative oil prices) can also affect the implied volatility behavior.

You can use the IV percentile edge is in your trading right now:

In Samurai, you can use the IV rank filter to find only trades with high or low IV percentile so you can build the right trades for you. BTW - we use the same data in the scanner and the research, so we expect similar results.

See how:

AUTHOR

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.