Reviewed by Leav Graves

The difference between in the money and out of the money options is one of the first aspects every trader has to understand. While factors like volatility and time matter, the moneyness simply describes the relationship between the option's strike price and the current price of the underlying asset.

KEY TAKEAWAYS

- In the money and out of the money options are defined by what they are worth today. In the money options hold real equity if exercised right now, while out of the money options possess only time value.

- In the money options offer stability for buyers but carry higher assignment risk for sellers. Out of the money options provide cheaper leverage for buyers but require a larger move to profit, often benefiting sellers through a lower probability of being exercised.

- In the money options have the highest premiums, meaning buyers pay a higher upfront cost while sellers collect maximum income. Out of the money options are cheaper, allowing buyers to risk less capital while sellers collect smaller premiums in exchange for a higher probability of keeping it.

The Cheat Sheet: Calls vs Puts

The distinction between in the money and out of the money options tells you whether a contract holds real equity today (ITM) or just the potential for value tomorrow (OTM). Since it is easy to mix up these terms, here is a quick reference guide to keep the definitions straightforward when you are looking at in the money and out of the money examples:

What Are In the Money Options?

When investors talk about in the money options, they are referring to contracts that have crossed the threshold into profitability (on paper).

The defining characteristic here is that in the money options have immediate intrinsic value. If you were to exercise one of these options today, you would pocket the difference between your strike price and the current market price.

However, you don't actually need to exercise them. Instead, you can simply sell the option contract back to the market. Because the contract holds that intrinsic value, you can sell it for a higher premium than you paid, capturing the profit without ever buying (for a call) or selling (for a put) the underlying asset.

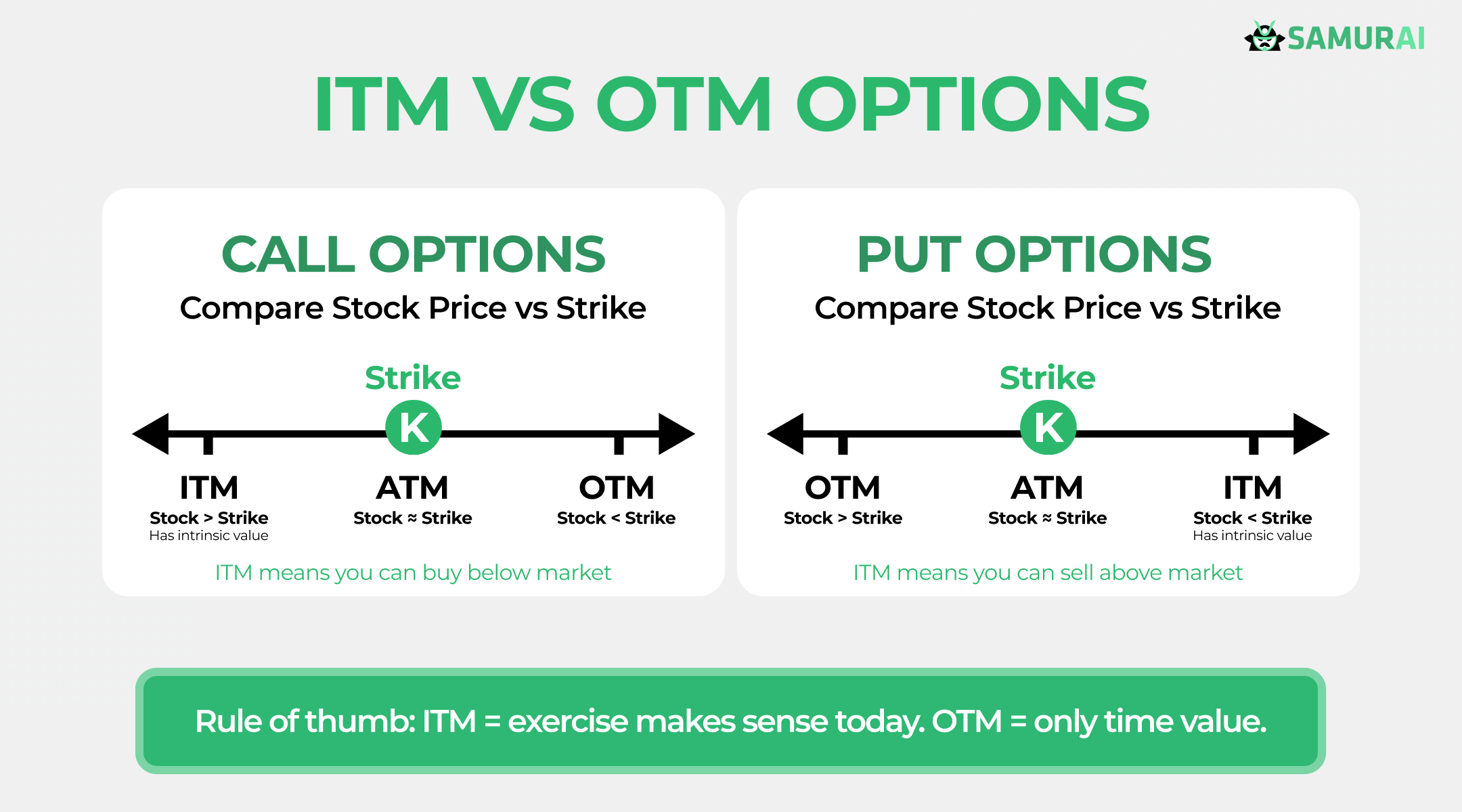

Using a simple in the money and out of the money example, here is how you can instantly spot an ITM contract

- Call Options: The stock price is higher than your strike price. (You can buy low and sell high instantly).

- Put Options: The stock price is lower than your strike price. (You can sell high and buy low instantly).

Pros: In the money options have a statistically high probability of finishing with value. Buyers benefit from high exposure to the stock price (high Delta) with less sensitivity to time decay. Sellers benefit by collecting the largest possible upfront premiums.

Cons: The stakes are higher. Buyers face a steep upfront capital cost to enter the trade. Sellers face the risk of early assignment; because American-style options can be exercised at any time, you may be forced to buy or sell the shares unexpectedly, typically when the time value of the option is low. This is a key risk factor when comparing in the money and out of the money options.

What Are Out of the Money Options?

Out of the money options are pure potential.

If you exercised one of these contracts today, you would lose money immediately. Why would you exercise a right to buy a stock for $50 when it is trading at $40? You wouldn't.

Because they have zero intrinsic value, these options are priced entirely on "potential" and time. They only have value because there is still time left on the clock for the stock price to move favorably.

Using a simple in the money and out of the money example, here is how you can instantly spot an OTM contract

- Call Options: The stock price is lower than your strike price.

- Put Options: The stock price is higher than your strike price.

Pros: Buyers can control large positions with very little capital using out of the money options, offering the potential for massive returns. Sellers benefit from a high statistical probability that the option will expire worthless, allowing them to keep the full premium without assignment.

Cons: Buyers suffer from rapid time decay and are statistically likely to lose their entire investment. Sellers collect significantly smaller premiums compared to in the money options, offering less downside protection if the market moves against them.

Breaking Down the Option Premium: Intrinsic vs. Extrinsic Value

Now that you know the definitions of in the money and out of the money, let's look at why the prices are so different.

An option’s price, known as the premium, isn't arbitrary. While professional investors use mathematical models like Black-Scholes to calculate it down to the cent, the concept is actually quite simple. The price is just the sum of two specific components of value.

To understand the difference between in the money and out of the money, you just need to know which of these two components you are paying for.

How to Calculate the Intrinsic and Extrinsic Values

Here is a simple table to help you calculate these values for any in the money/out of the money examples:

Value Component | Call Option Formula | Put Option Formula |

Intrinsic Value | Stock Price - Option Strike Price (If result is negative, value is $0) | Option Strike Price - Stock Price (If result is negative, value is $0) |

Extrinsic Value | Option Premium - Intrinsic Value | Option Premium - Intrinsic Value |

Option Premium = Intrinsic Value + Extrinsic Value

1. Intrinsic Value (The "Real" Value)

This is the concrete value built into the contract right this second. It is simply the difference between the current Stock Price and your Strike Price.

- Who has it? Only in the money options.

Think of it this way: If you have a contract to buy a stock for $20, and the stock is trading at $30, your contract has $10 of real, tangible value. If you exercised that option today, you would capture that value instantly. This acts as a "floor" for the price; the option won't trade for less than this amount.

2. Extrinsic Value (The "Time" Value)

This is the "extra" cost you pay for the time remaining on the contract and the implied volatility (IV) (the chance the stock might move). It represents the possibility that the option could become more valuable in the future.

- Who has it? All unexpired options have some extrinsic value, but out of the money options are made of 100% extrinsic value.

This value is much more fragile. It decays, meaning it disappears as the expiration date gets closer. If the stock price doesn't move, this component drops to zero by the expiration date.

The Summary

- ITM Options are Expensive: You are paying for intrinsic value (real equity) plus extrinsic value (time).

- OTM Options are Cheap: Their intrinsic value is zero. You are only paying for extrinsic value (time/potential).

Real-World In the money and Out of the money examples

Let's use the analyzer feature on our options screener to look at a specific in the money vs out of the money example using Apple (AAPL).

- Current Stock Price: ~$285.00

- Expiration Date: March 20, 2026

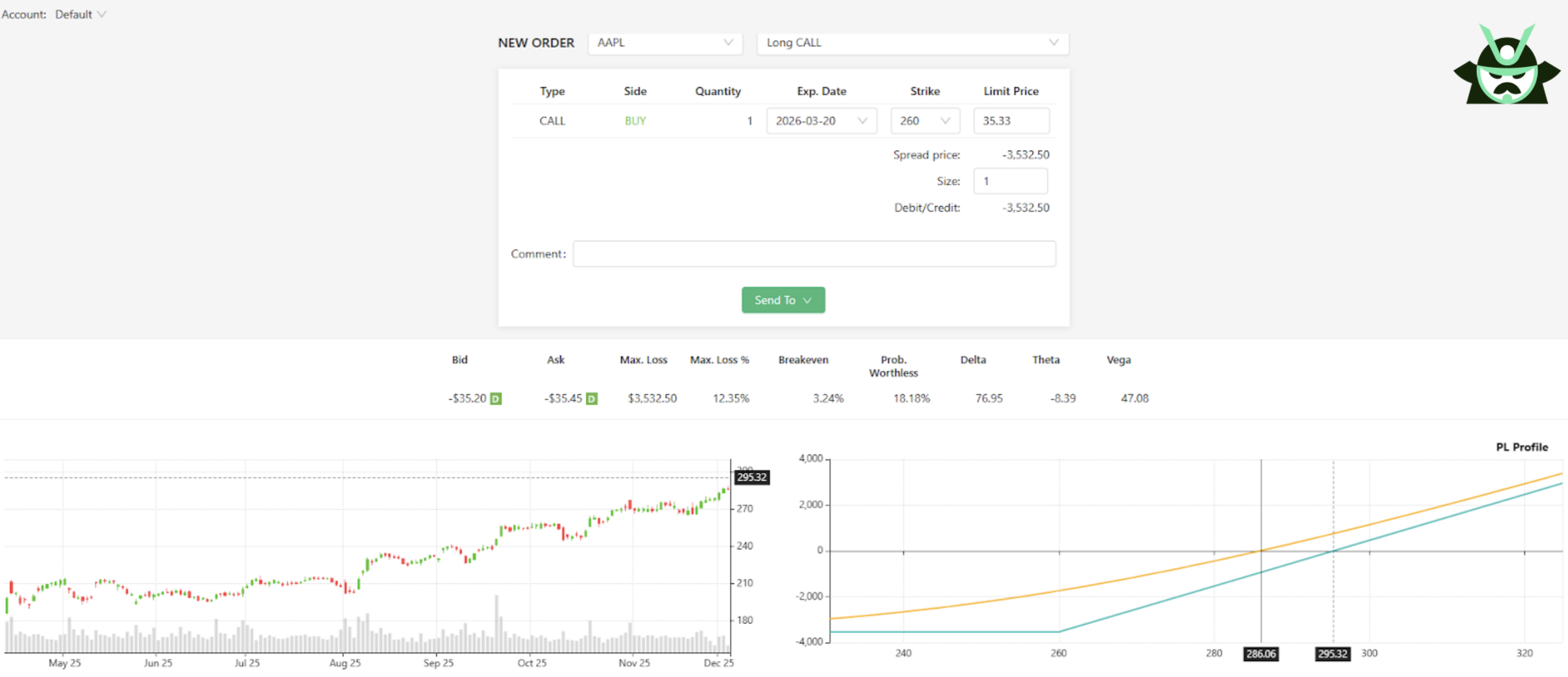

Scenario A: Buying The ITM Call ($260 Strike)

Let’s analyze a trade on the $260 strike call. Since the strike ($260) is lower than the stock price ($285.00), this is an in the money (ITM) option.

Cost: $35.33 per share ($3,533 total).

The Math: $25.00 of this price is intrinsic value ($285.00 stock price - $260.00 strike). Only $10.33 is time value (extrinsic).

The Concept: This trade is usually taken as a "stock replacement" strategy, especially when taken on a longer timeframe. With a delta close to 1 (0.77), the option mimics share ownership for a fraction of the cost ($3,533 vs $28,500 for 100 shares). Because much of the premium is real value rather than "time" value, the trade requires only a moderate move to breakeven roughly 3.6% to reach the $295.33 which is the breakeven price ($260 strike + $35.33 premium) by expiration.

Exercise vs. Sell: As the buyer, you hold the right to choose your exit. You can exercise the option to convert your contract into 100 shares of AAPL for a long-term hold, or more commonly, sell the contract back to the market to realize your profits as cash without ever touching the underlying shares.

The Risk: You are putting a large amount of capital at risk ($3,533) compared to a cheaper OTM strike, meaning you face a larger dollar loss if the stock crashes below the strike. However, because you are starting with intrinsic value, your probability of profit is statistically higher than buying speculative, cheaper calls.

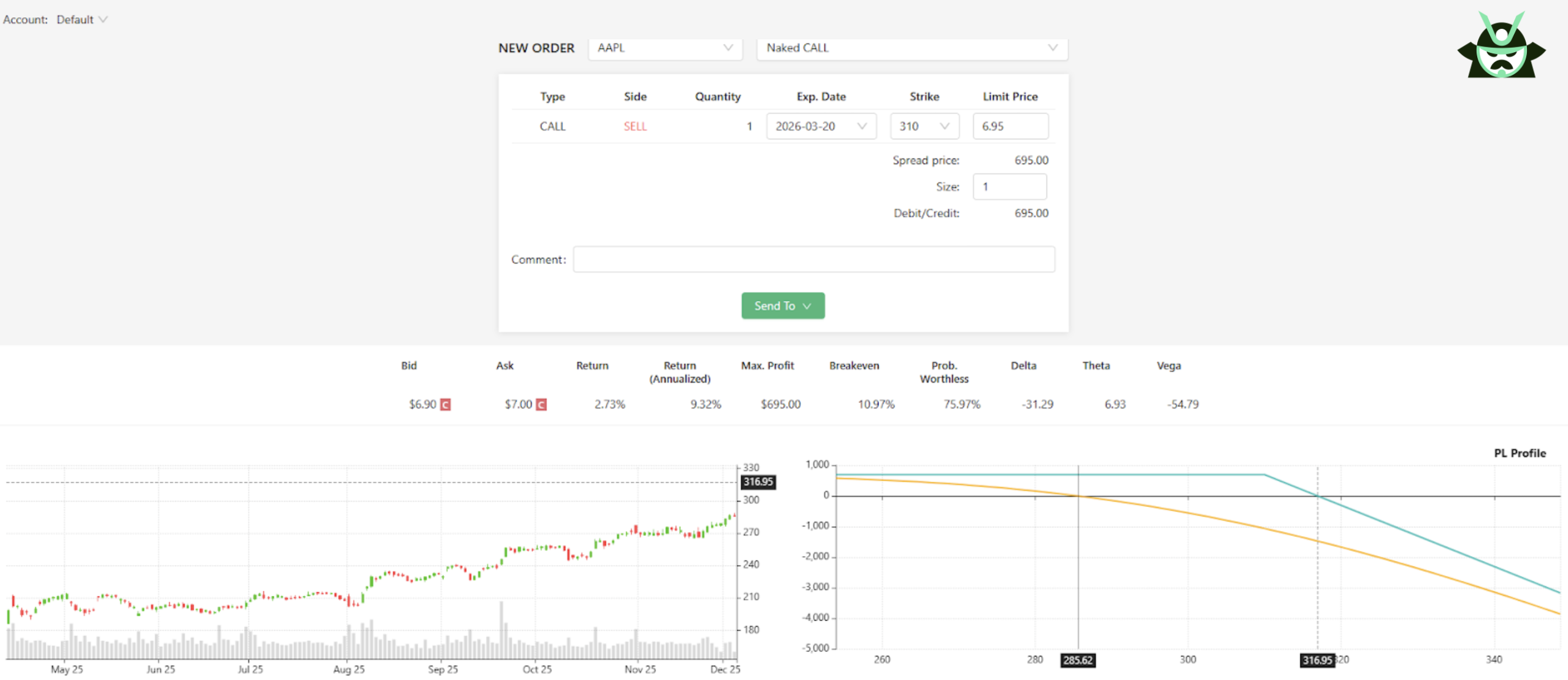

Scenario B: Shorting The OTM Call ($310 Strike)

Let’s analyze a “naked call” trade shorting the $310 strike call. Since the strike ($310) is significantly higher than the stock price ($285.00), this is an out of the money option.

Credit: You receive $6.95 per share ($695 total credit).

The Math: This option has $0.00 intrinsic value. The entire $6.95 credit is extrinsic value (time value). You are essentially selling "hope" to the buyer; your goal is to let time pass so that this value decays to zero and you can keep the initial credit as a profit.

The Concept: This is a neutral to bearish income strategy. The option has a low delta (-0.31), meaning you have a strong statistical advantage. You are expressing a view that the stock won't make a massive move upward. Based on the current options pricing, the data supports this view, with a 76% probability that the option expires worthless. As long as the stock stays flat, drops, or rises slowly, you keep the premium paid (Credit).

Assignment vs. Closing: Unlike selling an in the money option, there is no immediate risk of assignment because it makes no sense for a buyer to exercise an out of the money option. Your goal is generally to let the option expire worthless to keep the full $695 (but, in practice, you will often find yourself closing the trade earlier if you have already collected a significant profit). However, if the stock rallies and threatens the $310 strike, you can “buy to close” for a loss to exit the obligation, or "roll" the position, meaning you sell another call at a higher strike price or at a later expiration, or both.

The Risk: The risk remains theoretically unlimited if the stock experiences a large move upwards, but you have a much wider margin of error. The stock can rally roughly 11% to reach your breakeven price of $316.95 ($310 strike + $6.95 credit) and you will still not lose money if it remains below at expiry. However, once that line is crossed, your losses can accumulate rapidly with no cap.

The Tradeoff: In the Money vs Out of the Money

As we have seen in these in the money and out of the money examples, there is no single "best" option, only the right tool for the specific market outlook.

When comparing in the money vs out of the money, the primary difference lies in the probability of assignment and the premium exchanged.

In the money options carry higher premiums because they hold intrinsic value. For investors, this means higher capital requirements but a greater statistical probability of the option expiring with value. They function as high-probability instruments for buyers seeking equity exposure and sellers willing to accept assignment risk.

Out of the money options are comprised entirely of extrinsic (time) value. This results in lower premiums and lower capital requirements. However, they carry a lower statistical probability of finishing in the money, requiring a significant price move to gain intrinsic value before expiration. Ultimately, successful investing relies on mastering this in the money and out of the money relationship.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.