Reviewed by Leav Graves

Most traders know delta, gamma, theta, and vega. But there's a fifth greek that rarely comes up in conversation: rho. It measures how interest rates affect option prices, and most of the time, you can safely ignore it. But when rates are moving or you're trading long-dated options, rho in options starts to matter. Here's what you need to know.

KEY TAKEAWAYS

- Rho in options tells you how much its price changes for every 1% move in interest rates. It is positive for long calls and negative for long puts.

- Rho has a bigger impact on options with longer time to expiration and higher-priced underlying stocks, because the cost of carrying the position over time is greater.

- Rho is often overlooked because interest rates don't change frequently, but it becomes relevant around Federal Reserve meetings or during periods of shifting monetary policy.

Rho Options: How Interest Rates Affect Option Prices

Rho reports the expected change in an option's price for every 1% (one percentage point) move in interest rates. If a call option has a rho of +0.05, its price is expected to increase by $0.05 if rates rise by 1%, with everything else held constant.

But why would interest rates change the price of an option at all?

Options pricing models - like Black & Scholes - include an interest rate component because they assume traders hedge their positions using stock. The model prices an option based on its "hedged value," meaning the theoretical cost of maintaining a delta-neutral position over the life of the contract. Borrowing money to buy stock, or earning interest on the proceeds from selling stock short, both factor into that cost. That's options rho explained at its core - it ties back to hedging.

How rho in options affects calls and puts

When interest rates rise:

- Call premiums increase (positive rho options) - hedging a call involves selling stock, and higher rates make the proceeds from that short sale more valuable.

- Put premiums decrease (negative rho options) - hedging a put involves buying stock, and higher rates make borrowing to buy that stock more expensive.

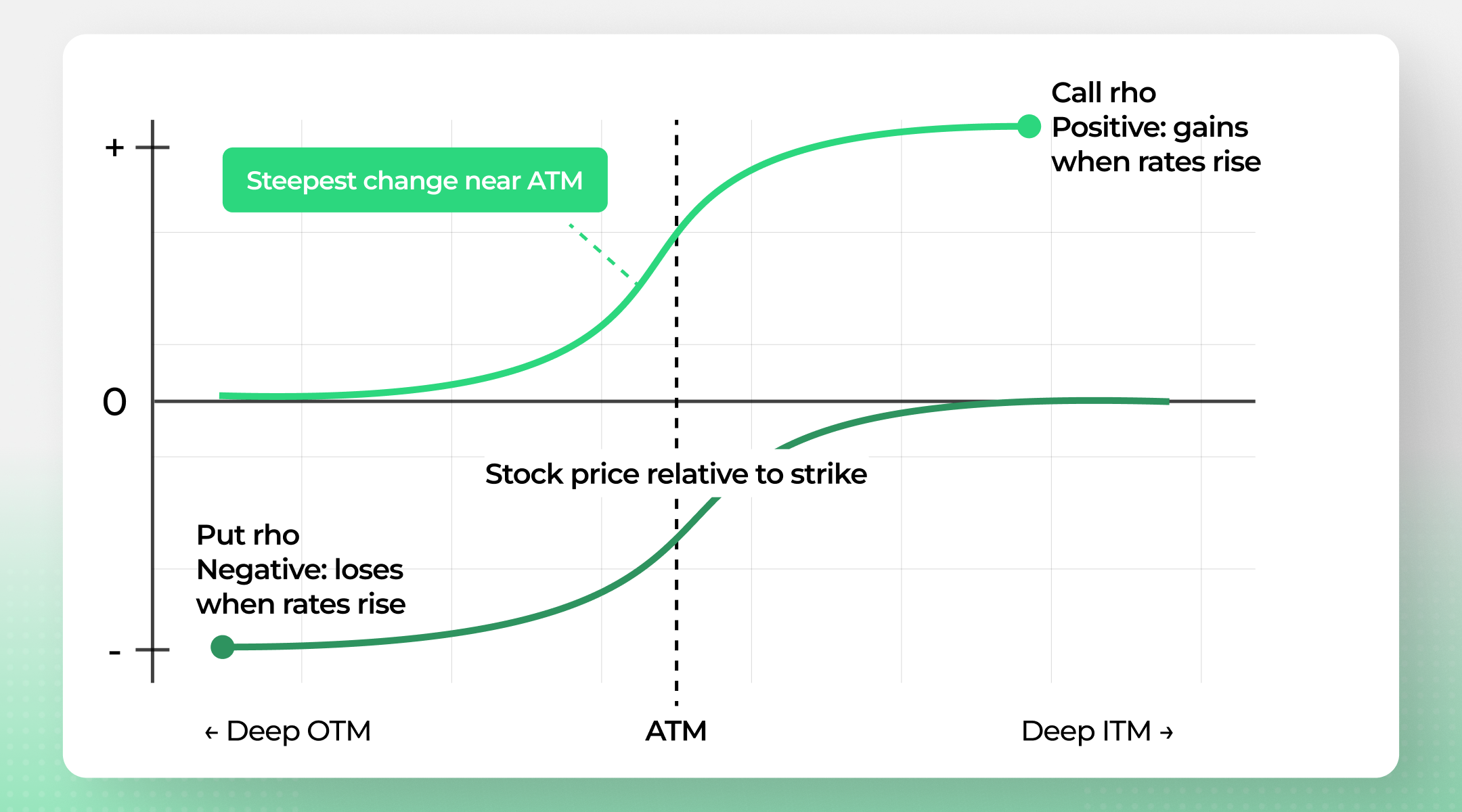

As the chart shows, both curves are steepest near ATM - that's where a rate change has the most impact on price:

The effect works in reverse when rates fall. For most short-term trades, this impact is small enough to ignore. But it adds up on longer-dated positions, which is why understanding what rho means in options matters if you trade LEAPS or hold positions for months. In short, rho in options is all about the relationship between interest rates and option premiums.

Options Rho Explained: The Cost of Carrying a Position

The reason interest rates show up in options pricing comes down to one thing: the cost of carry. Pricing models account for the money required to hedge a position with stock over time, and interest rates determine how much that costs.

A market maker theoretical case

Say a market maker buys a deep in-the-money put with a delta near -1.00. To become delta neutral, they need to buy 100 shares of the underlying. That stock purchase requires either borrowing cash or tying up capital that could otherwise earn interest.

If interest rates go up, the expense of holding that long stock position increases. The put buyer, knowing this, is willing to pay less for the option to offset those higher carrying costs. That's why puts have negative rho.

Now flip it. A market maker buys a deep ITM call with delta near +1.00 and sells 100 shares short to hedge. The proceeds from that short sale sit in an account earning interest. If rates rise, those proceeds earn more, which makes the hedged call position more attractive. That's why calls have positive rho. With options rho explained through these hedging scenarios, the direction for any position becomes easier to remember.

The general rule

- If hedging requires buying stock: rising rates increase carrying costs and hurt the position (negative rho options).

- If hedging requires selling stock: rising rates boost income from short sale proceeds and help the position (positive rho options).

Position | Rho in Options |

Long call | Positive |

Short call | Negative |

Long put | Negative |

Short put | Positive |

One more thing to keep in mind: interest rates are not uniform across the industry. They vary from clearing firm to clearing firm, brokerage to brokerage, and even account to account. The rate used in your platform's pricing model might not match what another trader sees.

Focus

Rho is the greek you can ignore most of the time, until the day you can't. When rates move or your positions stretch months out, it can quietly shift your P&L around FOMC events, so keep it in mind.

Rho Options - A Practical Example

Let's say interest rates are currently at 3%. You're looking at a call option priced at $5.00 with a rho of +0.45, and a put option priced at $4.50 with a rho of -0.45.

If rates jump from 3% to 4% (a 1% increase), here's what happens - assuming everything else stays the same:

- The call price rises by $0.45, from $5.00 to $5.45.

- The put price drops by $0.45, from $4.50 to $4.05.

That "assuming everything else stays the same" part is important. In reality, delta, theta, vega, and implied volatility are all moving at the same time. Rho's effect gets blended in with everything else, which is one reason it often goes unnoticed. Still, once you have options rho explained in dollar terms like this, it clicks.

Where Rho Fits Among the Options Greeks

When most traders talk about the options greeks, they focus on delta, gamma, theta, and vega. These four cover directional risk, acceleration, time decay, and volatility sensitivity - the factors that move the needle on most trades. Rho sits at the bottom of that list for a reason: interest rates just don't change as often or as dramatically as the other inputs.

But that doesn't mean it's irrelevant. During 2022 and 2023, when the Fed raised rates at a pace not seen in decades, rho in options quietly shifted premiums on longer-dated contracts. Traders who ignored it saw their LEAPS positions behave differently than their models suggested.

Think of it this way: delta, gamma, theta, and vega handle the day-to-day. Rho is the greek that matters when the macro environment shifts. If rates are stable, you can put it aside. If they're not, and you're holding options months out, it pays to understand what rho is in options and how it fits into the bigger picture alongside the other greeks.

What Does Rho Mean in Options Based on Price and Expiration?

Not all options react to interest rate changes equally. Two factors amplify rho's impact:

- Higher stock price: the cost of carrying a $250 stock position is much greater than a $50 one, so rho options on expensive underlyings are more sensitive.

- Longer time to expiration: more time means more carrying cost accumulates. This is similar to how vega behaves - longer-dated options are more sensitive.

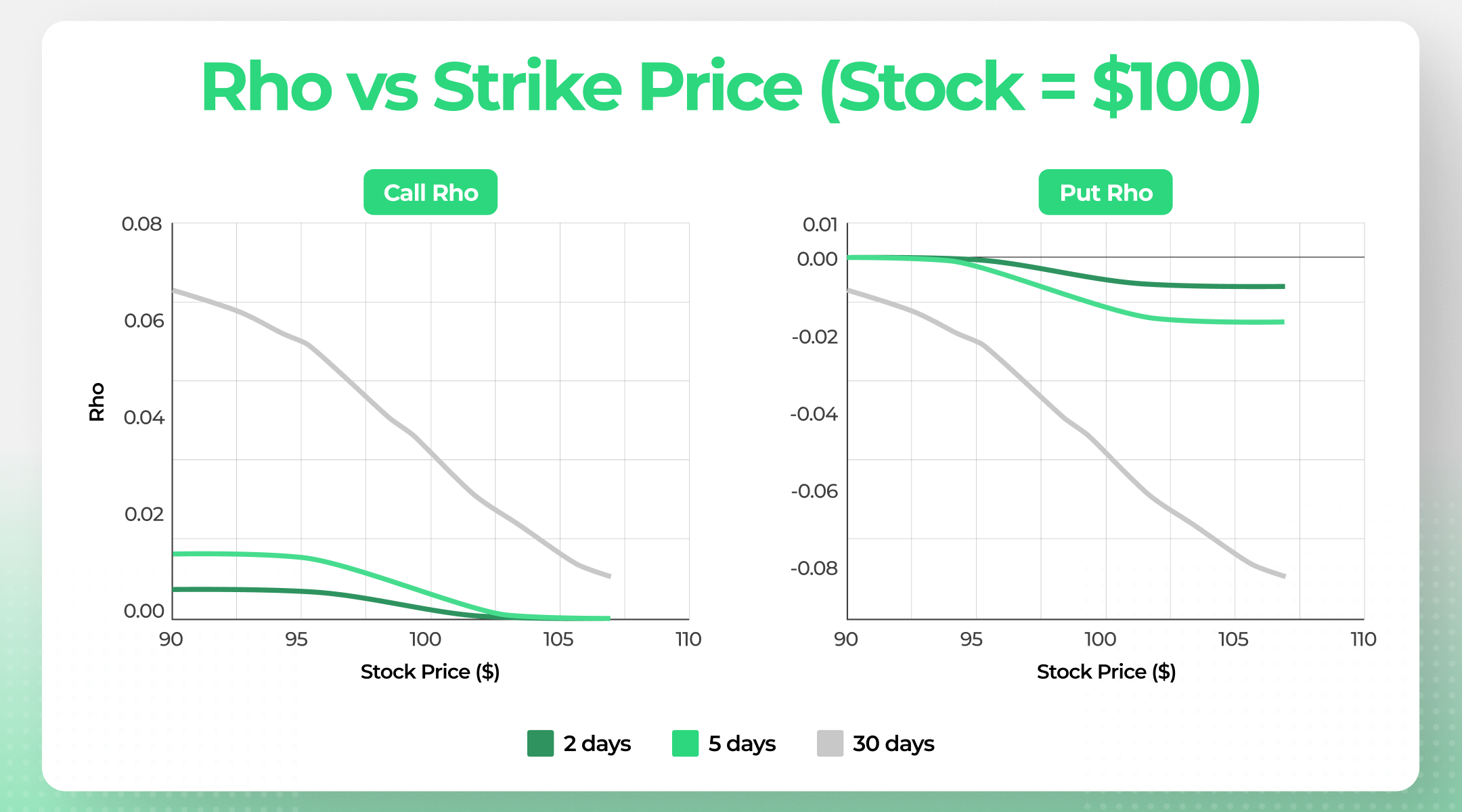

You can see both effects at once in the chart below. Each panel holds the stock price fixed at $100 and plots rho across strikes from $90 to $110, for three different expirations:

Two things jump out:

- First, the 30-day curves dwarf the 5-day and 2-day ones. Short-dated options barely react to interest rates at all, while a month of time to expiration already produces meaningful rho.

- Second, calls and puts are near-mirror images: calls have the highest positive rho at lower strikes (deep ITM), and puts have the most negative rho at higher strikes (also deep ITM).

That's the hedging logic from earlier showing up in the numbers: the deeper the option, the closer its delta to ±1, and the more stock the market maker has to carry.

Extend those 30-day curves out to a year or two, and you get LEAPS. These are the options where rho becomes most noticeable. Also, a LEAPS contract on a $250 stock will have a significantly higher absolute rho than a weekly option on a $50 stock. For short-dated options on low-priced underlyings, rho is often so small you can safely ignore it.

Rho becomes especially relevant around FOMC meetings or when the market is pricing in rate changes. If you trade LEAPS or high-priced underlyings, it's worth keeping an eye on rho in options and interest rate expectations as part of your trade evaluation. With options rho explained, you can factor rate expectations into your trading positions instead of being caught off guard.

Gianluca's Insight

I usually think of rho as a quiet risk, not something that drives most trades by itself. But when I look at longer dated options, I want to know what assumptions are sitting underneath the price. It is not about predicting the next rate move perfectly. It is about knowing when the trade is exposed to something most traders are not watching.

— Gianluca Longinotti, Finance Writer - Traders Education

AUTHOR

- Gianluca LonginottiFinance Writer - Traders Education

Gianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.