Options Greeks - What Are the Greeks in Options and Why They Matter

Published on April 20, 2026 | 7 min read(Last updated on May 26, 2026)

Reviewed by Leav Graves

Every option you look at has a set of numbers attached to it - delta, theta, vega, and more. These are the options greeks, and they tell you how an option's price is expected to react to changes in the market. But what do the greeks mean in options trading, and how should you actually use them? Below, we cover each greek and what it means for your trades.

KEY TAKEAWAYS

- Options greeks are a collection of sensitivity measures - each one capturing how a single input like direction, time decay, or volatility expectation impacts the cost of an option.

- Understanding what the greeks mean in options helps you evaluate risk before entering a trade - delta, gamma, theta, vega, and rho each measure a different dimension of risk.

- Options greeks are theoretical values derived from pricing models like Black-Scholes. They change constantly as market conditions shift, so use them as a guide rather than a guarantee.

What Are the Greeks in Options?

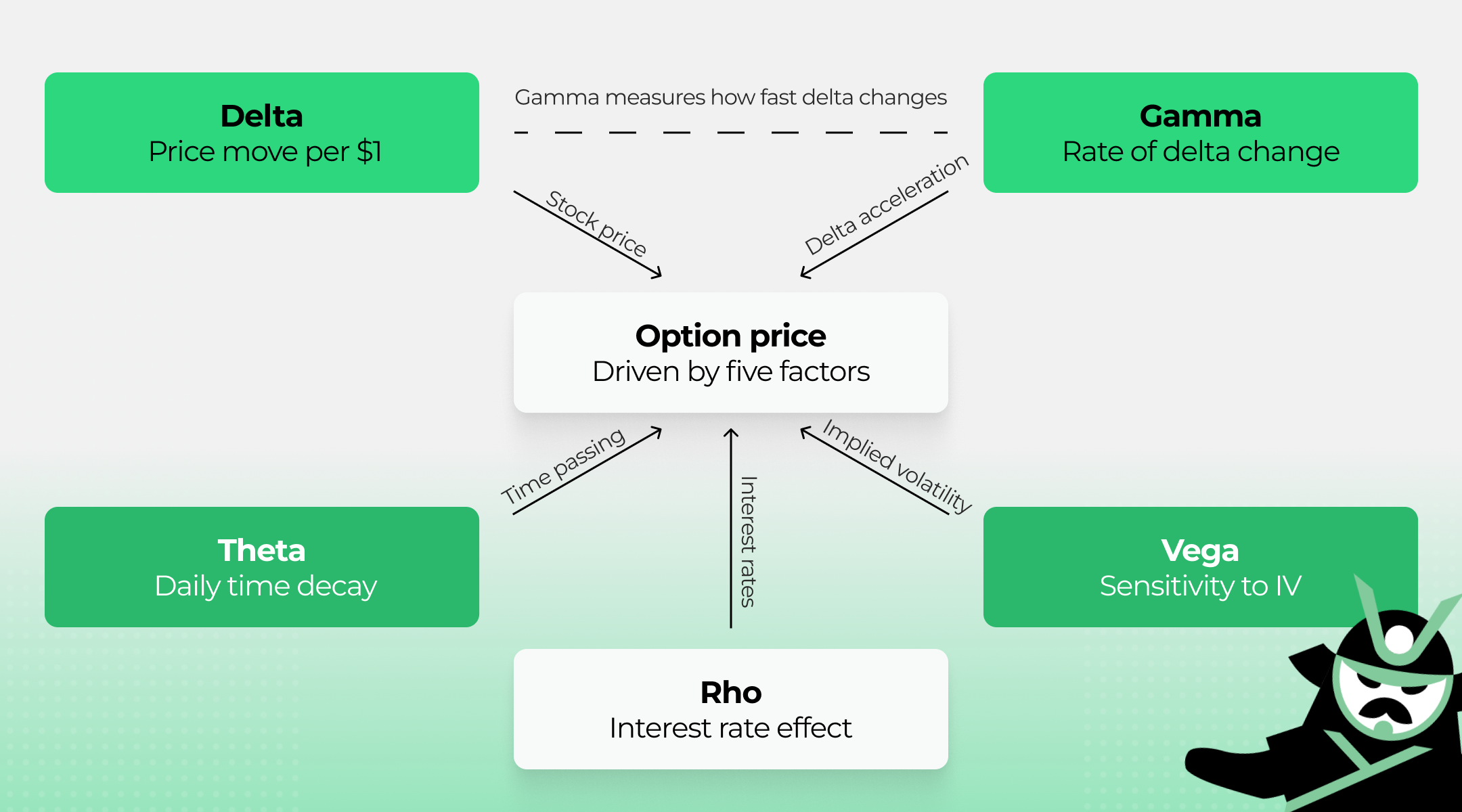

Options greeks are a collection of sensitivity measures - each one capturing how a single input like direction, time decay, or volatility expectation impacts the cost of an option. Instead of looking at an option's price as one number, the greeks break it into parts you can actually analyze.

The greeks on which options traders rely are five key metrics:

- Delta - how much the option's price moves when the stock moves $1

- Gamma - how fast delta itself changes

- Theta - how much value the option loses each day

- Vega - how the option reacts to changes in implied volatility

- Rho - how interest rate shifts affect the price

Each greek isolates one factor, which makes it easier to understand what's driving your position. But the real value comes from reading them together. Delta might tell you the direction looks good, but theta could be eating your profits while you wait, and vega might be working against you if volatility drops.

One thing to keep in mind: these are theoretical values, calculated from pricing models like Black-Scholes. They're not predictions - they're estimates based on current conditions. The options greeks change constantly as the stock price, time to expiration, and volatility shift. So when you see options greeks explained as exact numbers on your screen, treat them as a guide, not a guarantee.

Now let's look at what the greeks mean in options trading, one by one.

Options Greeks Explained: A Breakdown of Each Greek

Here's what each of the greeks options traders use actually tells you, and why it matters for your positions.

Delta

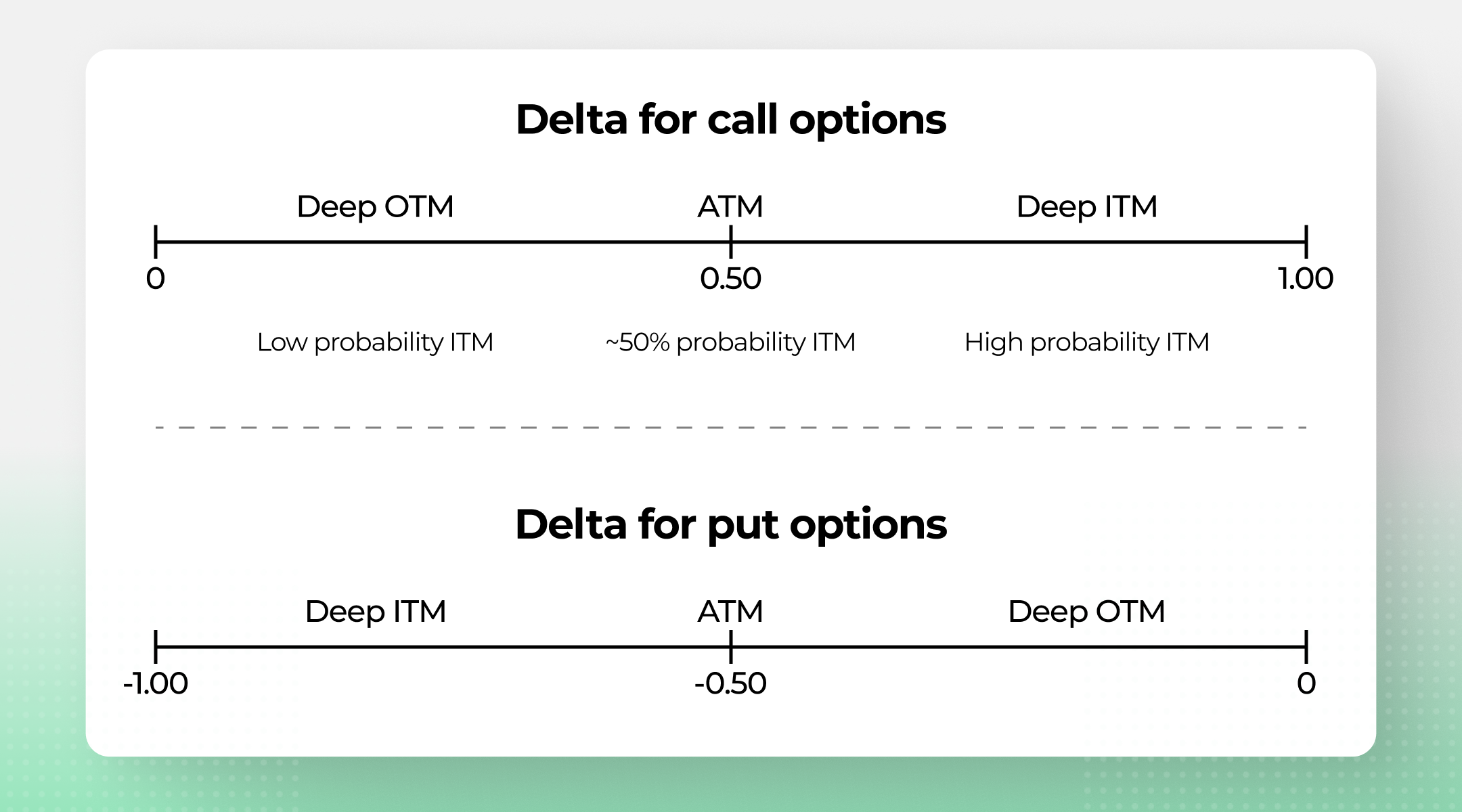

Delta in options measures how much a contract’s price is expected to move for every $1 change in the underlying stock. If a call option has a delta of 0.60, you can expect it to gain roughly $0.60 when the stock rises by $1.

The range for the delta options greek works like this:

Specifically:

- Call Options: delta between 0 and 1.00

- Put Options: delta between 0 and -1.00

At-the-money options tend to sit near 0.50 (or -0.50 for puts). The deeper in-the-money an option goes, the closer delta gets to 1.00. The further out-of-the-money, the closer it drops to 0.

There's also a useful shortcut: delta roughly approximates the probability of an option expiring in the money. A 0.30 delta call has about a 30% chance of finishing ITM. It's not exact, but it's a quick way to gauge how likely your trade is to pay off. Keep in mind that, on our options screener, we show delta in 100s so that it is easier to read (e.g., 30.94 will be better to read than 0.3094).

Gamma

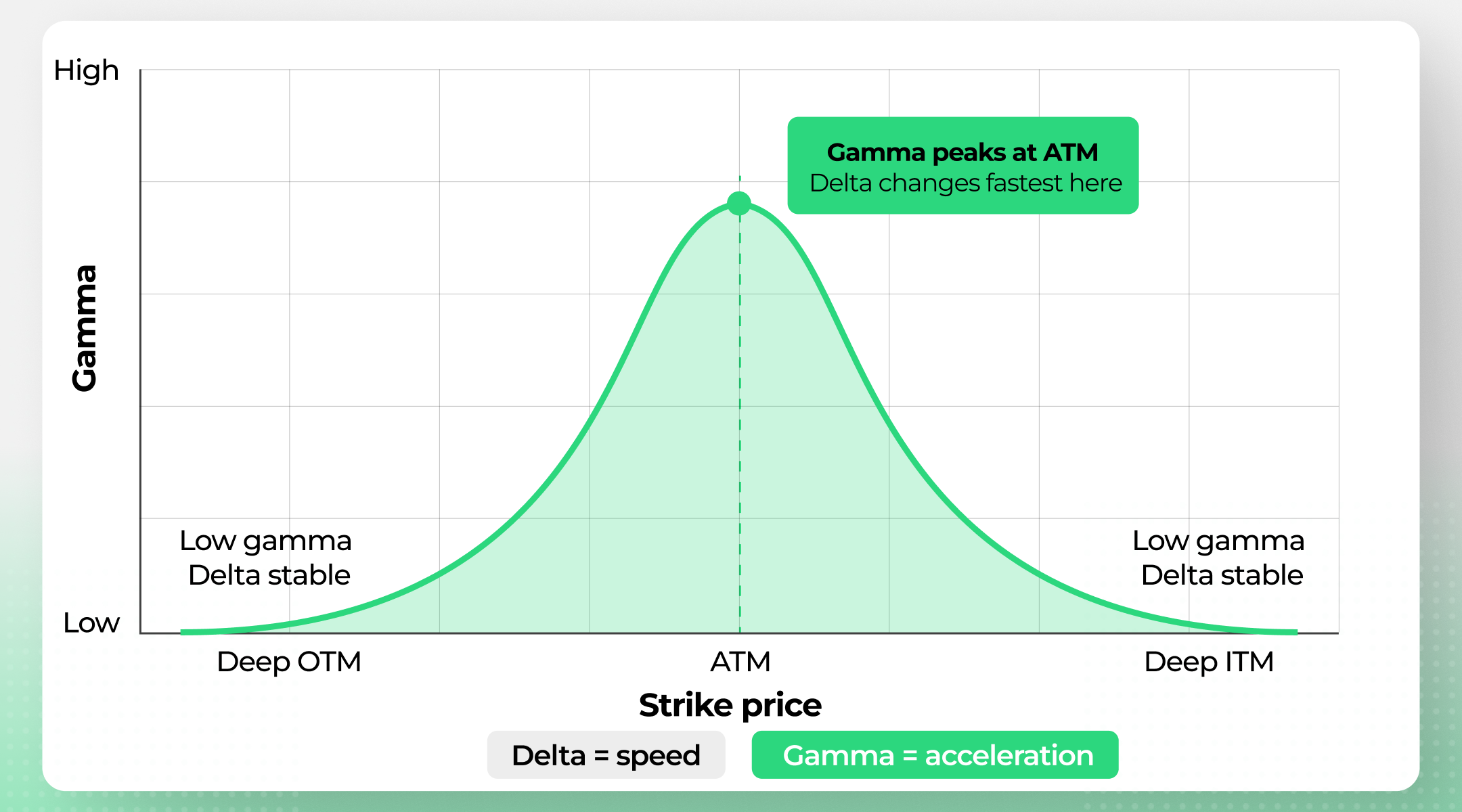

Gamma in options measures how fast delta changes when the stock moves $1. If delta is speed, gamma is acceleration.

Say you own a call with a delta of 0.50 and gamma of 0.08. If the stock goes up $1, your new delta becomes roughly 0.58. That matters because it means your option is gaining sensitivity to the stock's movement as it goes your way, and losing sensitivity when it doesn't.

Gamma is highest for at-the-money options and drops off as you move deeper in-the-money or out-of-the-money. You can see this in the chart below:

It also increases as expiration gets closer, which is why short-dated ATM options can behave unpredictably - small stock moves cause big swings in delta.

As far as options greeks go, gamma is the one that can change your position's character fastest. That's great when the move is in your favor, but it works both ways.

Theta

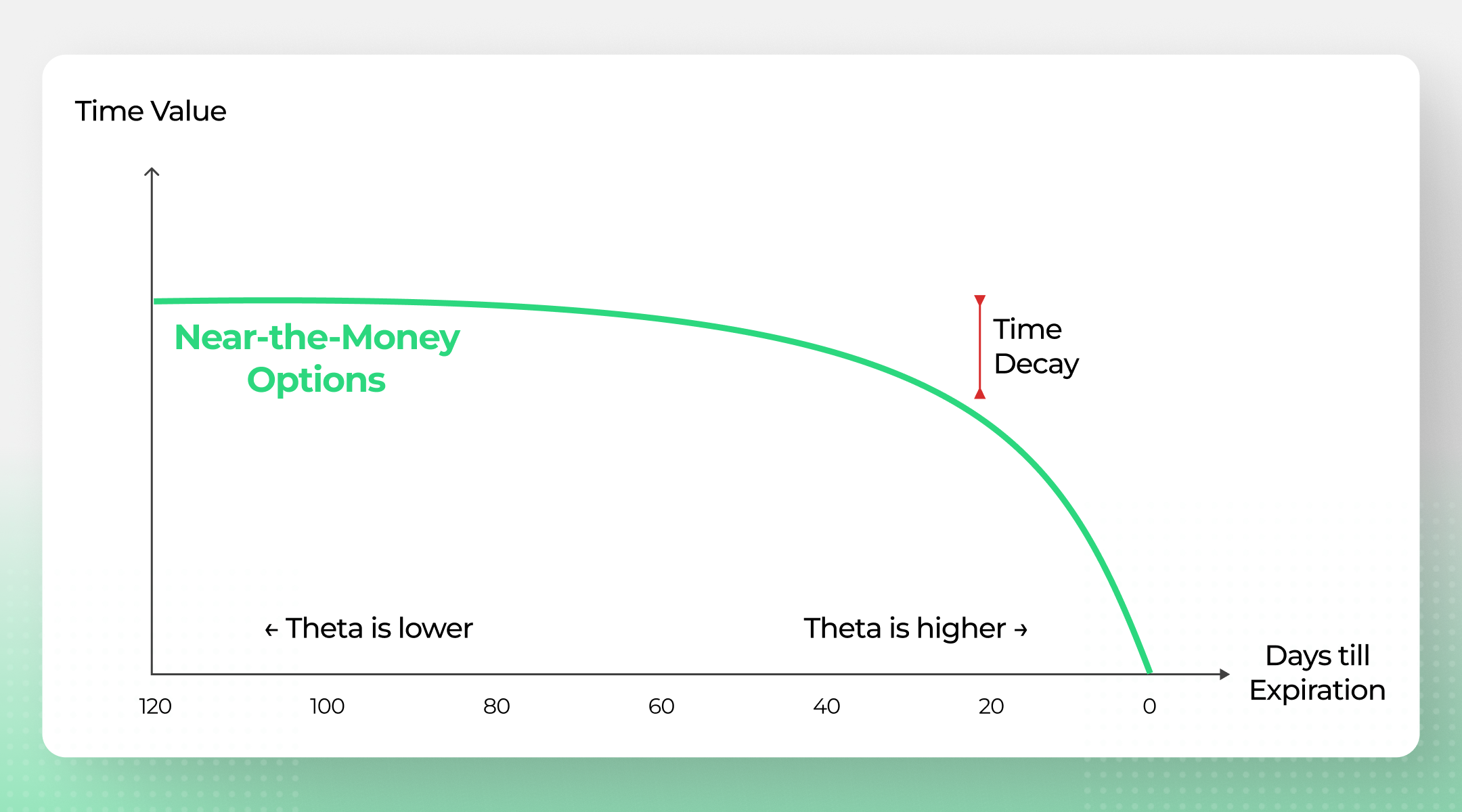

Theta in options tells you how much value your contract loses each day just from time passing. A theta of -0.05 means the option drops about $0.05 per day, all else being equal.

To understand what the greeks mean in options from a buyer's perspective, start with theta (it's always a cost): your position bleeds value every day you hold it. For sellers, it's the opposite: theta is how you earn income. Every day that passes works in the seller's favor.

The key thing to know is that theta accelerates, as you can see from the chart below:

An option with 60 days left might lose a few cents per day. That same option with 5 days left could be losing 10x that amount. This is why many traders avoid buying options too close to expiration unless they expect a quick move.

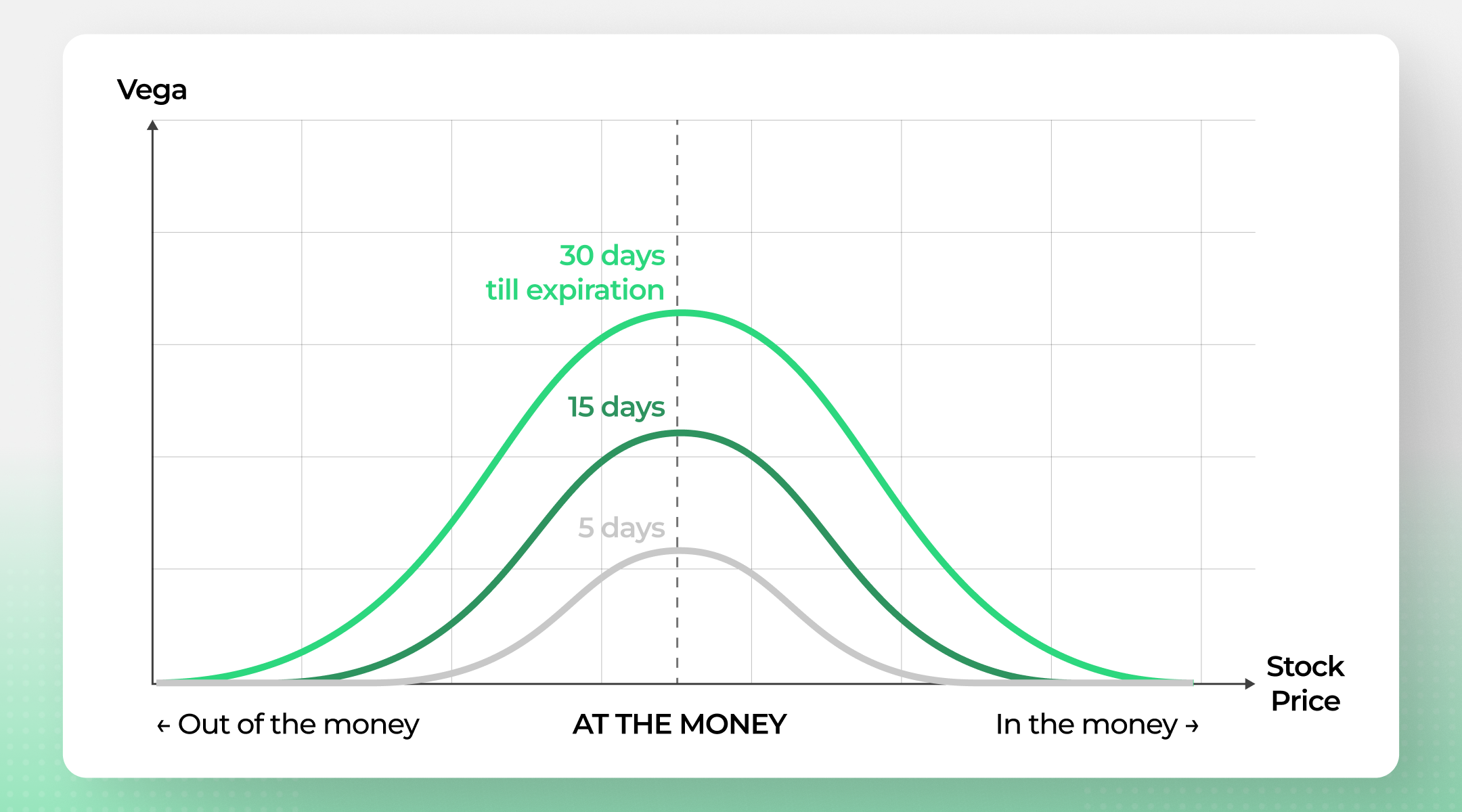

Vega

Vega in options measures how much a contract price changes when implied volatility moves by 1%. A vega of 0.12 means the option gains $0.12 if IV rises by one percentage point, and loses $0.12 if IV drops by one point.

Like gamma, vega is highest for at-the-money options. But it also depends on time. Options with more days to expiration have higher vega - they're more sensitive to volatility changes. As expiration approaches, vega shrinks, meaning short-dated options barely react to IV shifts. You can see this clearly in the chart below:

Fun fact: vega isn't actually a Greek letter. But it's one of the most important options greeks explained in any trading course, because volatility often drives option prices more than the stock itself.

Once you have options greeks explained in context, the practical takeaway for vega is:

- When IV is below its normal range, options are relatively cheap - better conditions for buying

- When IV is above its normal range, options are expensive - better conditions for selling

This is why many traders check IV rank or IV percentile before entering a trade. You want to know whether you're paying a premium or getting a discount.

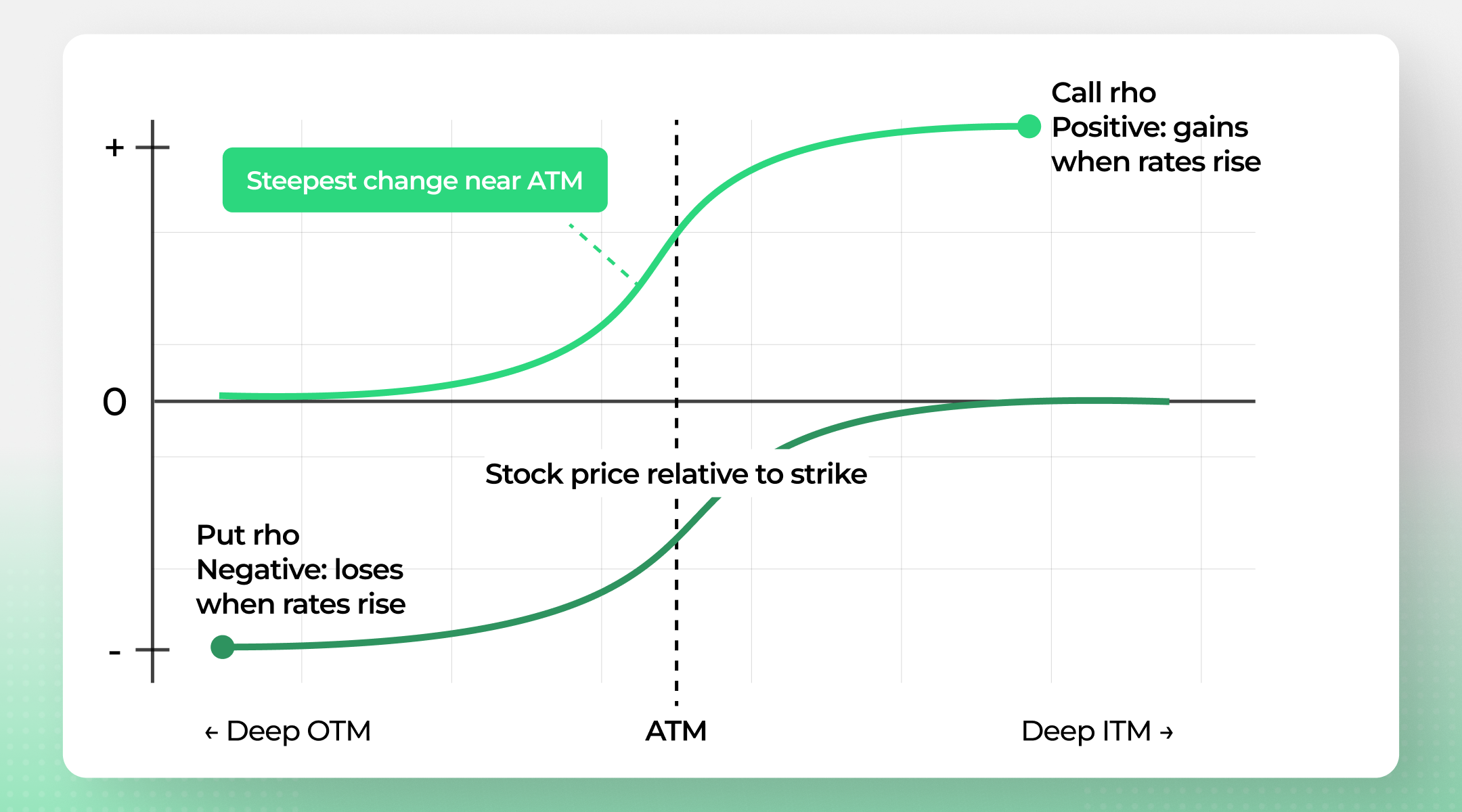

Rho

Rho in options measures how much a contract price changes when interest rates shift by 1%. Calls have positive rho (they gain value when rates rise), and puts have negative rho (they lose value when rates rise).

Most of the time, rho is the least noticed of the options greeks, and you can often ignore it. But there are two situations where it starts to matter:

- Before FOMC meetings, when rate decisions can move expectations quickly

- On LEAPS (long-dated options), where the longer timeframe gives interest rates more room to compound

As the chart shows, both curves are steepest near ATM - that's where a rate change has the most impact on price:

When rates rise, the cost of carrying stock increases. This makes calls slightly more attractive relative to puts, widening the price gap between call and put options at the same strike. It's a subtle effect, but on a 2-year LEAP, the difference can be noticeable.

How Implied Volatility Connects to the Options Greeks

Implied volatility (IV) isn't something you can observe directly - it's an inference based on what market participants are willing to pay for options right now. And it touches almost every greek. Vega measures your direct exposure to IV changes, but shifts in volatility also affect delta, gamma, and theta.

The practical question is: is IV high or low compared to normal? A useful way to measure this is IV rank (also called IV percentile), which tells you where the current IV sits relative to the past year. An IV rank of 90% means the stock's IV is higher than 90% of the days over the last year - in other words, options are expensive right now. An IV rank of 10% means they're cheap.

IV rank tends to be mean-reverting. After a high reading, IV usually drops. After a low reading, it tends to rise. This gives you a practical edge: when IV rank is high, consider strategies that profit from a decrease in volatility, like selling options. When IV rank is low, buying options gives you room for IV to expand in your favor.

IV doesn't stay constant either. It can spike around earnings announcements, M&A rumors, product launches, or any event that creates uncertainty. When you see the greeks options chains display, keep in mind that those numbers are only as stable as the IV behind them. A sudden volatility shift can change what the options greeks mean in practice, even if the stock hasn't moved at all.

Gianluca's Insight

The greeks are useful on their own, but I've found that the real edge comes from reading them as a group. A trade can look great on delta alone, but if theta is working against you and IV is already elevated, you're fighting the position from day one. Over time, I've learned to check IV rank before anything else: it frames everything that follows.

— Gianluca Longinotti, Finance Writer - Traders Education

What Do the Greeks Mean in Options Trading? Practical Tips

Now that you have options greeks explained, here's a quick reference for how to use each one when scanning trades. Option Samurai displays these greeks directly in the scanner, so you can filter by them before entering a position.

Options Greeks | What to check | When it matters most |

Delta | Directional exposure and probability of expiring ITM | Choosing strike prices |

Gamma | How fast delta will change | Trading short-dated ATM options |

Theta | Daily time decay cost or income | Holding options near expiration |

Vega | Sensitivity to IV shifts | Before buying into high-IV setups |

Rho | Impact of interest rate changes | LEAPS and around FOMC meetings |

No single greek tells the full story - combine them for a more complete risk view. That's what the greeks in options are really for.

AUTHOR

- Gianluca LonginottiFinance Writer - Traders Education

Gianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.