Reviewed by Leav Graves

Vega in options measures how much an option's price moves when implied volatility changes. But what does vega mean in options on a practical level, and why should you pay attention to it? This article has options vega explained in plain terms - what drives implied volatility, how vega in options works with real numbers, and how it impacts your long and short positions.

KEY TAKEAWAYS

- Vega in options tells you how much its price changes for every 1% move in implied volatility.

- Long options positions have positive vega and benefit when implied volatility rises. Short options positions have negative vega and benefit when implied volatility drops.

- Vega is highest for at-the-money options with more time to expiration, and only affects an option's extrinsic value, not its intrinsic value.

Vega Options - What Is It?

Vega in options is a direct way to measure how much the price of your option will change every time implied volatility (IV) will shift 1% up or down. So, before you can understand what vega is in options, you need to understand IV.

IV is an annualized estimate of how much a stock is expected to move, based on one standard deviation. For example, if a $100 stock has 20% IV, the market expects it to trade roughly between $80 and $120 over the next year.

When IV is high, options are more expensive. When IV is low, they're cheaper. This makes sense: if the market expects bigger price swings, options carry more potential value, and sellers demand a higher premium.

Vega tells you the exact dollar impact of those IV changes. If an option has a vega of 0.20, its price will increase by $0.20 for every 1% rise in IV, and decrease by $0.20 for every 1% drop (all else being equal). That's what vega in options comes down to - a direct measure of your IV exposure.

Keep in mind that IV is not a guarantee. It reflects what the market expects, not what will actually happen. A stock with 30% IV doesn't have to move 30% - it's just what the options market is pricing in. To fully understand what vega is in options, remember: it connects IV changes to actual dollar changes in your option's price.

Options Vega Explained: What Drives Implied Volatility?

Each of the options greeks measures a different risk factor - delta tracks direction, theta tracks time, and so on. With the basics of vega options covered, the next question is: what causes IV to move in the first place?

The short answer is uncertainty. When traders don't know what's coming, they pay more for options as protection, and that demand pushes IV higher. When the uncertainty fades, IV tends to drop.

Here's what typically moves IV:

- Macro events - job reports, CPI releases, and interest rate decisions from the Fed can shift IV across the entire market. Everyone is watching the same data, so the impact is broad.

- Company-specific events - earnings announcements are the classic example. IV in that stock's options tends to spike before the event, because nobody knows which direction the stock will go.

- Post-event IV crush - once the event passes and uncertainty is resolved, IV often collapses. This can happen fast, sometimes overnight.

Leav's Insight

The hardest lesson with vega is that you can be completely right on direction and still lose money. I've seen it play out countless times around earnings: a trader buys calls because they're convinced the stock goes up, the stock does go up, and the position still ends the day red because IV collapsed the moment the report dropped. Once you've been on the wrong side of an IV crush, you will likely remember it for a long time and think about vega before you trade options.

— Leav Graves, CEO

Tools like expected move and IV help traders see what the options market is pricing in before a big event. This is where vega in options becomes practical - if IV is about to shift, vega tells you how much that shift will cost or benefit your position. With options vega explained in these terms, IV events stop being abstract and start being something you can trade around.

Vega Options - A Practical Example

Let's put vega in options into real numbers. Say you buy a call option with a vega of 0.20. If IV rises by 1%, the option price goes up by $0.20 per share, or $20 per contract. If IV drops by 1% instead, you lose that same $0.20 per share.

That might not sound like much, but IV swings of 5-10% (or even more) may be common as the market approaches major events. A 5% IV increase on that same option adds $1.00 per share, or $100 per contract, just from the volatility change alone - no stock movement needed. If someone asks you what vega is in options, this is the example to give them.

Vega Around Earnings

Compare a put option on the same stock two weeks before earnings versus during earnings week. The option expiring during earnings week will have a much higher vega because it carries the full weight of the uncertainty around the announcement.

After the earnings report drops, IV collapses, and with it, vega's impact shrinks. This is why some traders sell vega options right before earnings - they're betting on the IV crush reducing option prices, regardless of the stock's direction.

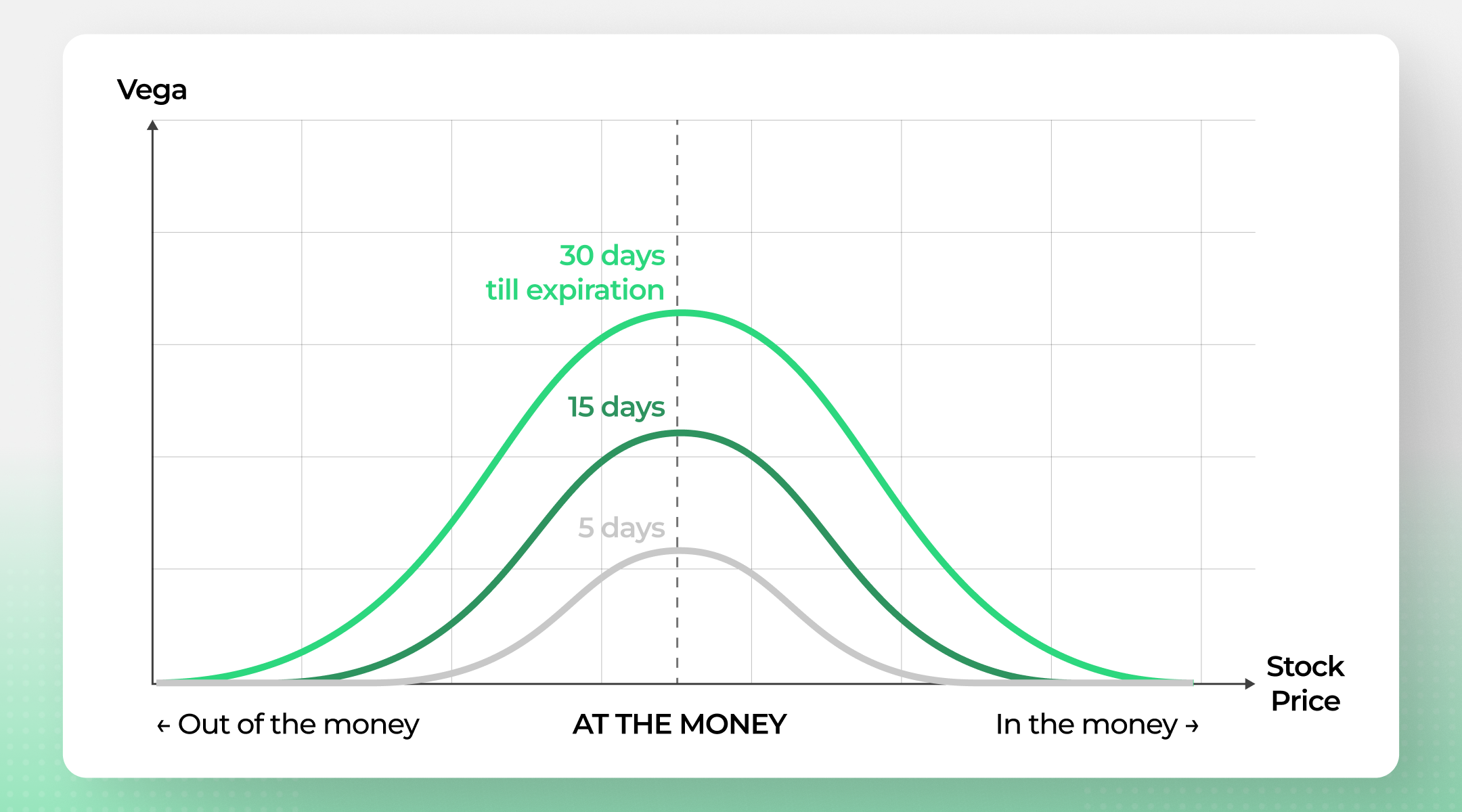

The chart below shows how vega in options behaves across different expirations:

Vega peaks at the money and increases with more time until expiration. The 30-day option has significantly higher vega than the 5-day option at every point along the curve. This visual is a quick way to understand what vega means in options - ATM, longer-dated contracts are the most sensitive to IV changes.

What Does Vega Mean in Options for Long and Short Positions?

Every option position is either long vega or short vega. To really understand what vega means in options, you need to know which side of the trade you're on. Here's what vega means in options for both sides.

Long Vega Positions

These are trades entered for a net debit:

- Long calls

- Long puts

- Debit spreads

- Long straddles and strangles

Long vega trades tend to be directional. You're looking for a sharp move in the stock. If IV rises, your position benefits because the options you own become more expensive. If IV drops, even a move in the right direction can be offset by the loss in extrinsic value.

Short Vega Positions

These are trades entered for a net credit:

- Naked calls or puts

- Credit spreads

- Short straddles and strangles

Short vega traders are betting that the market is overstating future volatility. They sell options they believe are overpriced and profit if IV collapses after entry. If IV rises instead, their positions lose value.

Understanding whether your position is long or short vega in options helps you anticipate how a shift in volatility will affect your trade before it happens.

Vega in Options - How It Works and What Affects It

When you look at an options chain, vega in options displays as a positive number. That's because options chains quote from a long perspective. If you're long the option, your vega matches what's shown. If you're short, flip the sign - your vega is negative.

Here's what affects how large vega is:

- Time to expiration - options with more time have higher vega. A LEAPS contract is far more sensitive to IV changes than a weekly option.

- Moneyness - at-the-money options have the highest vega. OTM and ITM options have lower vega because their prices are less influenced by IV shifts.

- Extrinsic value only - vega affects only the extrinsic (time) value portion of an option's price. If you own a deep ITM call, most of its value is intrinsic, and vega has less influence on the total premium.

This is why options become noticeably more expensive during periods of uncertainty. It's not that the stock has moved - it's that the extrinsic value inflates due to higher IV. Vega in options is the greek that captures this relationship. With options vega explained across strikes, expirations, and position types, you have a complete picture of how vega options pricing affects your trades.

See Vega in Action: IV Shifts on Real Strategies

Numbers on a page only get you so far. The easiest way to internalize what vega means in options is to watch a P&L curve reshape itself as IV moves. Option Samurai's IV change control lets you do exactly that: drag the implied volatility slider up or down and see how your strategy's payoff diagram responds in real time.

Long Straddle (Long Vega)

A long straddle is one of the purest long vega trades out there. You're buying both a call and a put at the same strike, so you have no directional bias: you're betting on a big move or a rise in IV.

Watch what happens when IV rises: the entire P&L curve shifts upward, even with the stock price sitting still. That's positive vega doing its job. Now imagine the opposite: an IV crush after earnings. As you can imagine, the curve would drop the same way. This is why long straddles entered before an earnings event can lose money even when the stock moves, if the post-event IV collapse is sharp enough.

Iron Condor (Short Vega)

An iron condor shows you a very different image. You're selling a call spread and a put spread, collecting premium, and hoping the stock stays between your short strikes. It's a textbook short vega trade.

Notice how rising IV pushes the curve down. Even if the stock hasn't moved an inch, your position is losing value because the options you sold have become more expensive to buy back. Falling IV does the opposite: the curve lifts, and you can close the trade for a profit before expiration.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

- Leav GravesCEO

Leav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.