Straddle Option Strategy - Two Option Strategies for Handling Market Volatility

Published on August 1, 2024(Last updated on April 13, 2025)

Reviewed by Leav Graves

Once you learn how a simple long call and long put trades work, you'll likely want to explore more advanced trading strategies. In fact, this guide will focus on the straddle option strategy, a popular setup in options trading, showing both long and short versions. Let's see how these setups can benefit from market volatility or stability with a detailed straddle option example.

KEY TAKEAWAYS

- The straddle option strategy is a trade setup that lets you either benefit from large price movement in the underlying stock in its long version or a sideways trend in its short version.

- Long straddles offer unlimited profit potential in volatile markets but can incur losses if the expected price movement doesn't occur.

- Short straddles provide limited profit potential in stable markets but come with unlimited risk if the underlying asset's price moves significantly beyond the breakeven points.

What Is the Straddle Option Strategy?

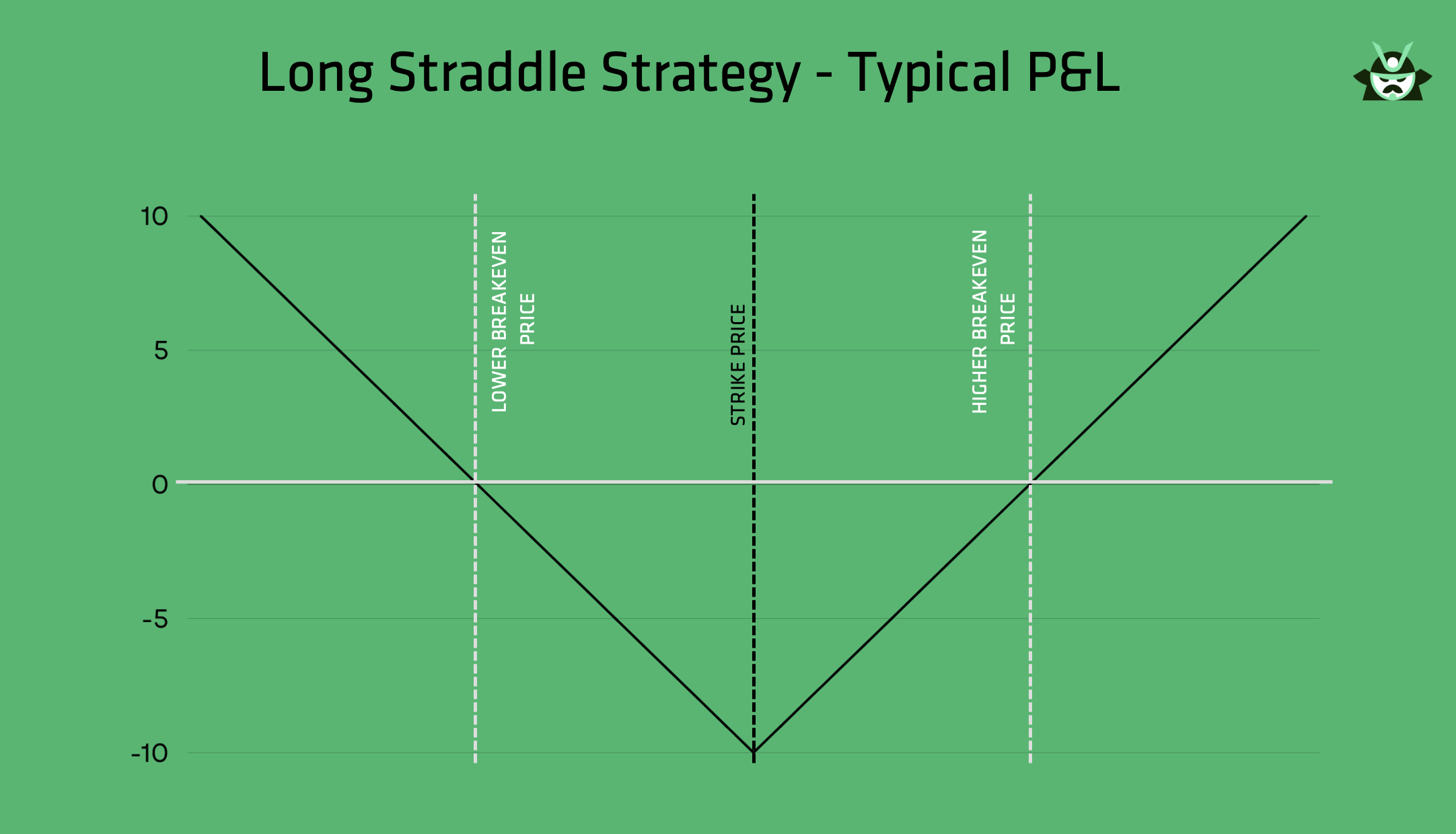

The straddle option strategy involves buying both a call and a put option for the same underlying asset, with the same strike price and expiration date. The straddle option strategy allows traders to profit from significant price movements in either direction.

A straddle option strategy is surely similar to a strangle, but it often uses ATM options instead of OTM, meaning that the whole strategy setup is generally more expensive to buy, but the break-even points are closer (assuming you are looking at the long version of the trade).

In a long straddle option, the trader buys both a call and a put option. This approach offers unlimited profit potential if the price of the underlying asset moves significantly in either direction.

However, if the price does not move much, the trader can incur losses equal to the total premiums paid for both options. The strategy’s P&L has this typical shape:

- Long Case - Buying Both a Call and a Put Option: In a long straddle position, you purchase both a call option (betting the price will go up) and a put option (betting the price will go down). Note that, with this straddle option strategy, you’ll normally look for options with low implied volatility (IV), as an increase in IV will likely increase the value of your options.

- Short Case - Selling Both a Call and a Put Option: In contrast, when you sell both a put and a call option, you are dealing with what is known as a short straddle, betting on price stability. Note that, with this straddle option strategy, you’ll normally look for options with high implied volatility (IV), as a decrease in IV will likely decrease the value of the options you are short-selling.

- Same Expiration Date and Strike Price: Both options must have the same expiration date and strike price to form a straddle.

A Long Straddle Option Example: Long Straddle

Suppose a trader buys a call and a put option for stock XYZ, both with a strike price of $100 and an expiration date one month away. If the total premium paid for both options is $10, the breakeven points are $110 and $90. If there's a significant price change beyond these breakeven points, the trader stands to make a profit.

A Short Straddle Option Example: Short Straddle

In contrast, a trader might sell both a call and a put option for stock ABC, each with a strike price of $50 and a total premium received of $6. The breakeven points are $44 and $56. The trader profits if the stock price remains within this range.

Max Risk and Max Profit in the Straddle Position

Understanding the maximum risk and maximum profit of any option strategy is crucial before entering a trade. Since this article covers both the long and short straddle setups, let’s break down the payoff potential for each:

Long Straddle – Max Loss and Max Gain

- Max Loss: The maximum risk in a long straddle is limited to the total premium paid for the call and put options. This happens if the underlying asset stays exactly at the strike price at expiration, making both options expire worthless.

- Max Gain: The long straddle offers unlimited profit potential. If the asset makes a significant move in either direction, one leg of the trade will become highly valuable, potentially offsetting the premium paid and generating large returns.

Short Straddle – Max Loss and Max Gain

- Max Loss: The short straddle comes with unlimited risk. If the underlying asset moves far above or below the strike price, the loss can grow indefinitely on the uncovered side.

- Max Gain: The maximum gain is limited to the total premiums collected from selling both the call and put options. This occurs if the underlying asset closes exactly at the strike price on expiration.

How to Use the Straddle Option Strategy

There are two main ways to use the straddle option strategy, and the choice on the approach merely depends on your market volatility outlook:

- Long Case - Market Expectations of Significant Volatility: The long straddle option strategy is most effective when you expect the underlying asset to experience significant volatility. This could be due to upcoming earnings reports, regulatory decisions, or major economic events.

- Short Case - Market Expectations of Low Volatility: In the short straddle version, you would sell both a call and put option if you expect the underlying asset to trade within a specific price range or remain relatively stable.

The Long Straddle Option Strategy

Let's begin with the long straddle option strategy. This trade setup consists of buying both a call option and a put option for the same underlying asset, with the same strike price and expiration date.

The goal of this investment strategy is to profit from significant price movements in either direction, making it ideal for volatile markets (think, for instance, of those traders opening a long straddle position the day before a company's earnings announcement).

Your strategy will work best in the following cases:

- High Volatility: The long straddle strategy works best when there is high volatility in the underlying asset. If the stock price swings significantly, the trader can benefit from substantial gains. More precisely, you would generally need the stock to experience higher volatility than what the current option prices imply.

- Significant Price Movements Expected: This straddle option strategy is most effective when you expect significant price movements but are unsure of the direction. Events like earnings reports, regulatory news, or economic data releases can cause such movements.

In terms of risk and reward profile, here is what you get:

- Unlimited Profit Potential on the Call Leg: If the price of the underlying asset rises significantly, the call option can generate unlimited profits. There’s no cap on how much the asset can appreciate.

- Limited Profit Potential on the Put Leg: While the call offers unlimited upside, the put option provides limited profit potential. The maximum gain from the put option occurs if the asset price drops to zero (which is generally a purely theoretical scenario).

- Premium Cost as a Risk Factor : One of the main risks of the long straddle option strategy is the cost of the premiums paid for both options. If the underlying asset's price doesn’t move enough to cover these costs, the trader faces a maximum loss equal to the total premium paid.

- Time Plays Against You: Since you are buying options, time decay (the “theta” greek in the Black & Scholes pricing model, if you don’t mind us being slightly technical) erodes the value of your straddle position.

How to Create a Straddle for High Volatility - A Long Straddle Option Example

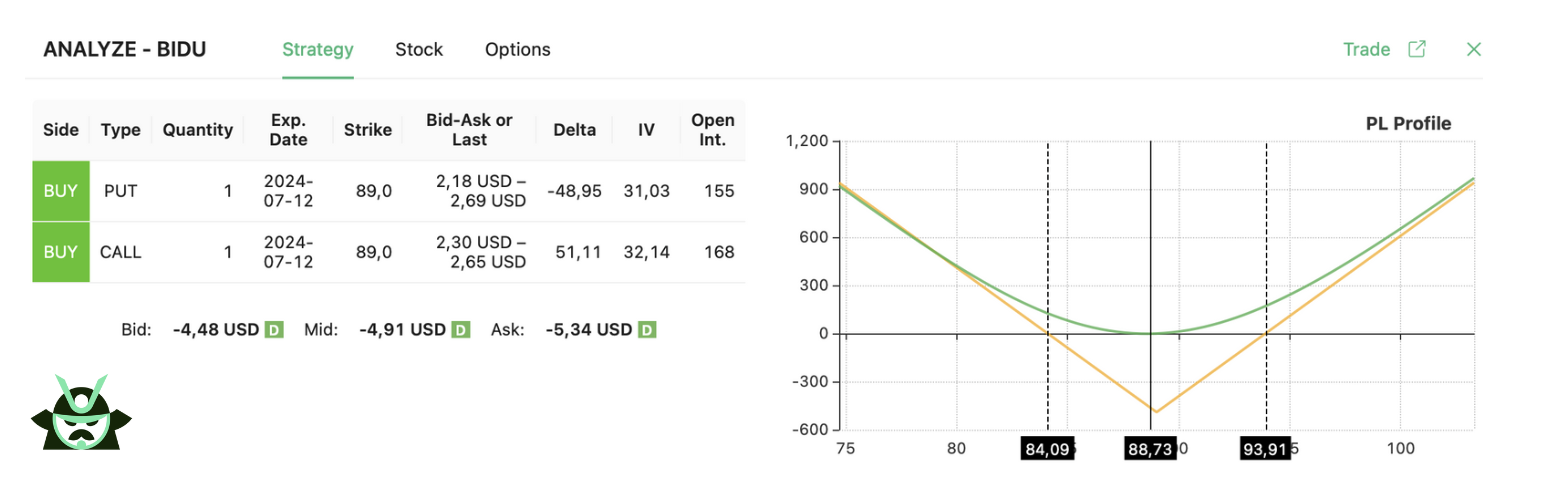

Perhaps an example will clarify how the straddle option strategy works in practice. Let’s consider a potential trade opportunity on BIDU. Imagine that, for whatever reason, you expect BIDU to experience a strong price movement.

However, you are not sure about the direction of the movement: things may go really well or really bad, depending on an earnings report that will soon be released.

In this case, our options screener would highlight the possibility of opening a long straddle option on BIDU. Consider that BIDU is now trading at $88.73. You could, for instance, buy an $89 put and an $89 call, both expiring in 3 weeks:

As you can see, your trade works as follows:

- Call Option: Strike price at $89 with mid-price equal to $2.44 (hence, you'd pay $244 for this leg of the trade)

- Put Option: Strike price at $89 with mid-price equal to $2.47 (hence, you'd pay $247 for this leg of the trade)

- Expiration: 3 weeks from now

- Total Premium Paid: $4.91 or $491 if you multiply it by 100 shares (which is just the sum of $244 and $247)

- Upper Breakeven: $89 + $4.91 = $93.91

- Lower Breakeven: $89 - $4.91 = $84.09

This means you need the price of BIDU to move either above $93.91 or below $84.09 to earn a profit. The return on your investment would entirely depend on how much BIDU moves above or below these breakeven prices, as it is technically unlimited.

The potential outcome of this long straddle option strategy are fairly easy to analyze:

- Significant Price Increase: If BIDU's price rises significantly above $93.91, the call option increases in value, potentially yielding large profits.

- Significant Price Decrease: If BIDU's price falls significantly below $84.09, the put option increases in value, again providing substantial gains.

- Minimal Price Movement: If BIDU's price remains around $89, neither option will gain enough value to cover the premiums paid. In the worst-case scenario, with the stock priced exactly at $89 when the options expire, you’d lose the total premium paid for both options, which is $491. However, in most cases, you will be able to close before expiration and recover some of the value.

The Short Straddle Option Strategy

We saw what happens with a long straddle in the two sections above, but what about the short straddle option strategy? This approach involves selling both a call option and a put option for the same underlying asset, with the same strike price and expiration date.

First of all, consider that there are at least two conditions for effectiveness:

- Low Volatility: The short straddle strategy is most effective when the underlying asset is expected to experience low volatility. This means the asset's price is unlikely to move significantly, staying within a tight range.

- Minimal Price Movement Expected: Traders use the short straddle position when they expect minimal price movement. Events like stable earnings reports or an absence of major market news can create such conditions.

In terms of risks and rewards, here is what you need to know:

- Unlimited Risk if the Market Moves Significantly: One of the significant risks associated with a short straddle is the unlimited potential for loss. If the underlying asset's price moves significantly in either direction beyond the breakeven points, the losses can be substantial.

- Breakeven Points and Risk Management: The breakeven points are calculated by adding and subtracting the total premiums received to and from the strike price. Effective risk management is crucial, including the potential use of stop-loss orders and constant monitoring of the market.

- Premium Collected as Initial Profit: The primary reward of a short straddle option strategy is the premium collected from selling both the call and put options. This premium represents the maximum profit potential if the asset’s price remains stable.

- Time Plays in Your Favor: Since you are selling options, you want their value to decrease. Time decay will erode the options value, a desirable scenario for your short straddle.

How to Create a Straddle for Low Volatility - A Short Straddle Option Example

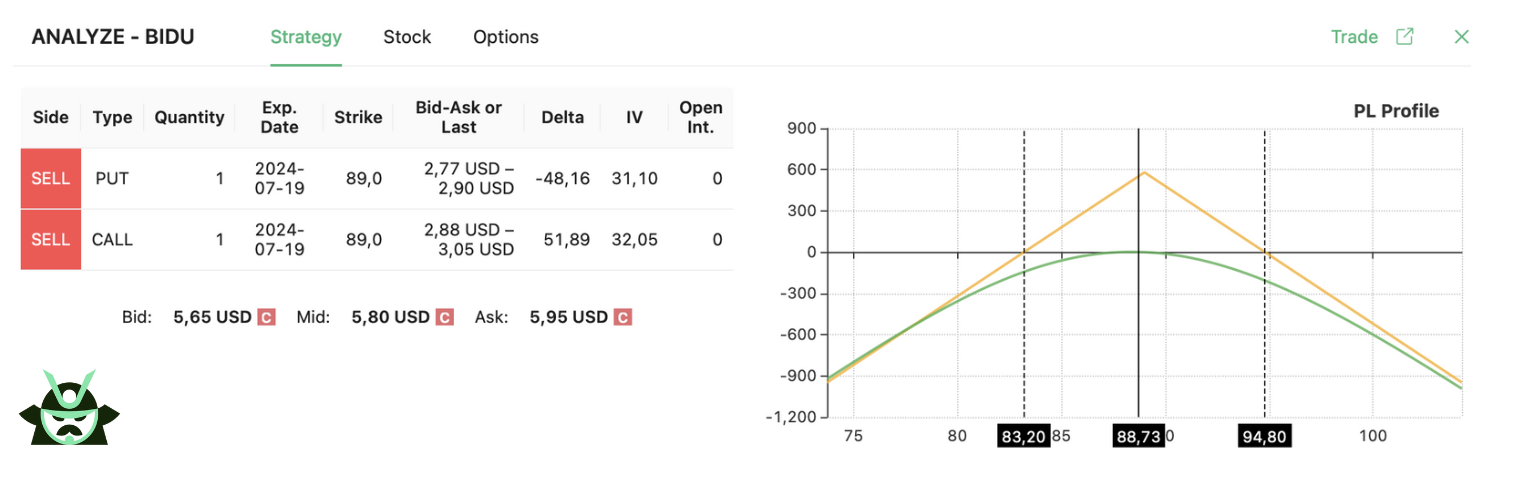

Just like we did for the long straddle strategy, let’s now consider a different potential trade opportunity on the same stock previously mentioned, BIDU.

Imagine that, for whatever reason, you now expect BIDU to remain close to $89 (remember, BIDU is trading at $88.73) for the next few weeks. In this case, our options screener would highlight the possibility of opening a short straddle option on BIDU.

You could, for instance, sell an $89 put and an $89 call, both expiring in a month:

If you take a look at the graph, here is what you should focus on:

- Call Option: Strike price at $89 with mid-price equal to $2.97 (hence, you'd collect $297 for this leg of the trade)

- Put Option: Strike price at $89 with mid-price equal to $2.83 (hence, you'd collect $283 for this leg of the trade)

- Expiration: 1 month from now

- Total Premium Received: $5.80 or $580 if you multiply it by 100 shares (which is just the sum of $297 and $283)

- Upper Breakeven: $89 + $5.80 = $94.80

- Lower Breakeven: $89 - $5.80 = $83.20

This means you need the price of BIDU to remain between $83.20 and $94.80 to earn a profit. The best-case scenario for you would be for the stock to close exactly at $89 to earn the sum of the two options premiums.

The potential outcomes of your short straddle option strategy are:

- Minimal Price Movement: If BIDU's price remains around $89, both options will expire worthless, allowing you to keep the entire premium received, which is $660. However, in most cases, you will need to close earlier and not collect the whole premium (as the stock will not expire on the exact strike).

- Price Increase: If BIDU's price rises but stays below $94.80, the call option will retain some value, but the put option will expire worthless, allowing you to keep part of the premium.

- Price Decrease: If BIDU's price falls but stays above $83.20, the put option will retain value, but the call option will expire worthless, again allowing you to keep part of the premium.

- Significant Price Movement: If BIDU's price moves significantly beyond the breakeven points, you could face unlimited losses. For instance, if BIDU's price rises above $94.80 or falls below $83.20, the losses could be substantial.

Pros and Cons of the Straddle Option Strategy

The straddle option strategy—in its long and short form—offers unique opportunities and challenges for traders. We summarized the matter in the table below:

Straddle Option Strategy | Pros | Cons |

Long Straddle | Potential for high returns | High premium costs + time plays against you |

Flexibility in volatile markets | Risk of limited movement leading to losses | |

Short Straddle | Potential for consistent income from premiums + time plays in your favor | Unlimited risk in volatile markets |

Effective in stable markets | Difficulty in picking the right timing |

Pros and Cons - Long Straddle Option Strategy

Pros:

- Potential for high returns: The long straddle option can yield unlimited profit if the underlying asset's price moves significantly in either direction.

- Flexibility in volatile markets: This straddle option strategy is ideal for traders expecting high volatility but uncertain about the direction of the price movement.

Cons:

- High premium costs: High premium costs and time decay can work against you, unlike the covered call strategy, which focuses on generating consistent income with lower risk.

- Risk of limited movement leading to losses: If the underlying asset's price remains stable, the trader may incur losses due to the premiums paid.

Pros and Cons - Short Straddle Option Strategy

Pros:

- Potential for consistent income from premiums: The short straddle option strategy allows traders to collect premiums from selling both call and put options. The good thing here is that time will play in your favor, contrary to what happens for the long strategy version.

- Effective in stable markets: This straddle option strategy works best when the underlying asset is expected to remain within a narrow price range.

Cons:

- Unlimited risk in volatile markets: If the asset's price moves significantly beyond the breakeven points, the trader faces unlimited potential losses.

- Difficulty in picking the right timing: While there are technical indicators that show when a stock is in a range-bound market, there's no guarantee of accuracy.

Straddle and Strangle Options Strategies Compared

The last aspect we want to tell you about is the comparison between the straddle and the strangle option strategy. Both methods aim to capitalize on market volatility, but they have distinct structures and risk profiles:

Basic Structure and Strike Prices

- Straddle Option Strategy: This involves buying or selling both a call and a put option with the same strike price and expiration date on the same underlying asset. A classic example is the long straddle option, where a trader buys both options, betting on significant price movements in either direction.

- Strangle Option Strategy: This straddle option strategy also involves buying or selling both a call and a put option, but with different strike prices. Typically, the call option has a higher strike price, and the put option has a lower strike price than the current market price of the underlying asset.

- Differences in Strike Prices:

In a straddle position, both options share the same strike price, creating a symmetrical setup around the current market price.

In a strangle position, the strike prices are set apart, requiring larger price movements for profitability but incurring lower overall premiums.

Long and Short Variations

Long Straddle vs. Long Strangle

The easiest way to understand the main differences between a long straddle and a long strangle is by comparing the respective pros and cons:

- Long Straddle:

- Pros: Potential for high returns if the underlying asset's price moves significantly in either direction.

- Cons: High premium costs and risk of limited movement leading to losses.

- Example: Buying a call and put option for stock XYZ at a $100 strike price.

- Long Strangle:

- Pros: Lower premium costs compared to the long straddle.

- Cons: Requires more substantial price movements to reach profitability.

- Example: Buying a call option at a $105 strike price and a put option at a $95 strike price for stock XYZ.

Short Straddle vs. Short Strangle

Here is a snapshot on the main differences you should know before trading a short straddle and a short strangle:

- Short Straddle:

- Pros: Potential for consistent income from premiums.

- Cons: Unlimited risk in volatile markets.

- Example: Selling a call and put option for stock ABC at a $50 strike price.

- Short Strangle:

- Pros: Lower risk compared to short straddle due to wider breakeven points.

- Cons: Still carries significant risk if the underlying asset moves dramatically.

- Example: Selling a call option at a $55 strike price and a put option at a $45 strike price for stock ABC.

Risk Profiles and Strategic Summary

Key Differences in Risk Profiles and Potential Rewards

- Straddle Option Strategy: More aggressive due to the higher premiums involved. Potential for substantial profits in highly volatile markets but comes with a higher risk if the expected price movement does not materialize.

- Strangle Option Strategy: Less aggressive with lower premiums but requires larger price movements to achieve profitability. Suitable for traders expecting significant market moves while managing cost risks.

So, you basically have two different ways to invest in similar market signals. You will opt for a long trade if you expect a high price movement and a short trade if you don't. Ultimately, this is as simple as it gets.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.