Synthetic Put – What It Is, How It Works, and Why Traders Use It

Published on May 26, 2025(Last updated on April 1, 2026)

Reviewed by Leav Graves

A synthetic put is a way to recreate the payoff of a regular put—long or short—using a mix of stock and options. This article explains how both the synthetic long put and the synthetic short put work, and why traders might choose a synthetic put option over a standard one.

KEY TAKEAWAYS

- A synthetic put is an options strategy that mimics a traditional put option using a combination of a call and the underlying asset. The synthetic long put is bearish, while the synthetic short put is bullish—just like regular long and short puts.

- The synthetic long put combines a short position in the stock and a long call option. It has limited loss and potentially high reward if the stock falls.

- The synthetic short put pairs a long stock position with a short call. It has limited profit and significant downside risk if the stock drops.

What Is a Synthetic Put?

A synthetic put is a strategy that copies the behavior of a regular put option—without using an actual put. It combines a call option and a stock position to create the same payoff. This works because of put-call parity, a pricing relationship between calls, puts, and the underlying asset.

There are two versions:

- A synthetic long put uses a short stock position and a long call. It’s a bearish strategy with limited loss and big upside if the stock falls.

- A synthetic short put uses long stock and a short call. It’s bullish, with limited gain and large downside if the stock drops.

Traders use synthetic put options when the actual puts are too expensive, unavailable, or to get better margin treatment.

You’ll hear terms like options synthetic long in this context—it just means you're building a long put using parts, not buying the put outright.

The Synthetic Long Put

To build a synthetic long put, you sell short the stock and buy a call option at the same strike. Let’s say AAPL is trading at $215. You:

- Sell short 100 shares of AAPL at $215

- Buy one 215-strike call for $6.00

This setup creates a synthetic put that behaves like a standard long put (like the one you could find on our screener for options) at the 215 strike.

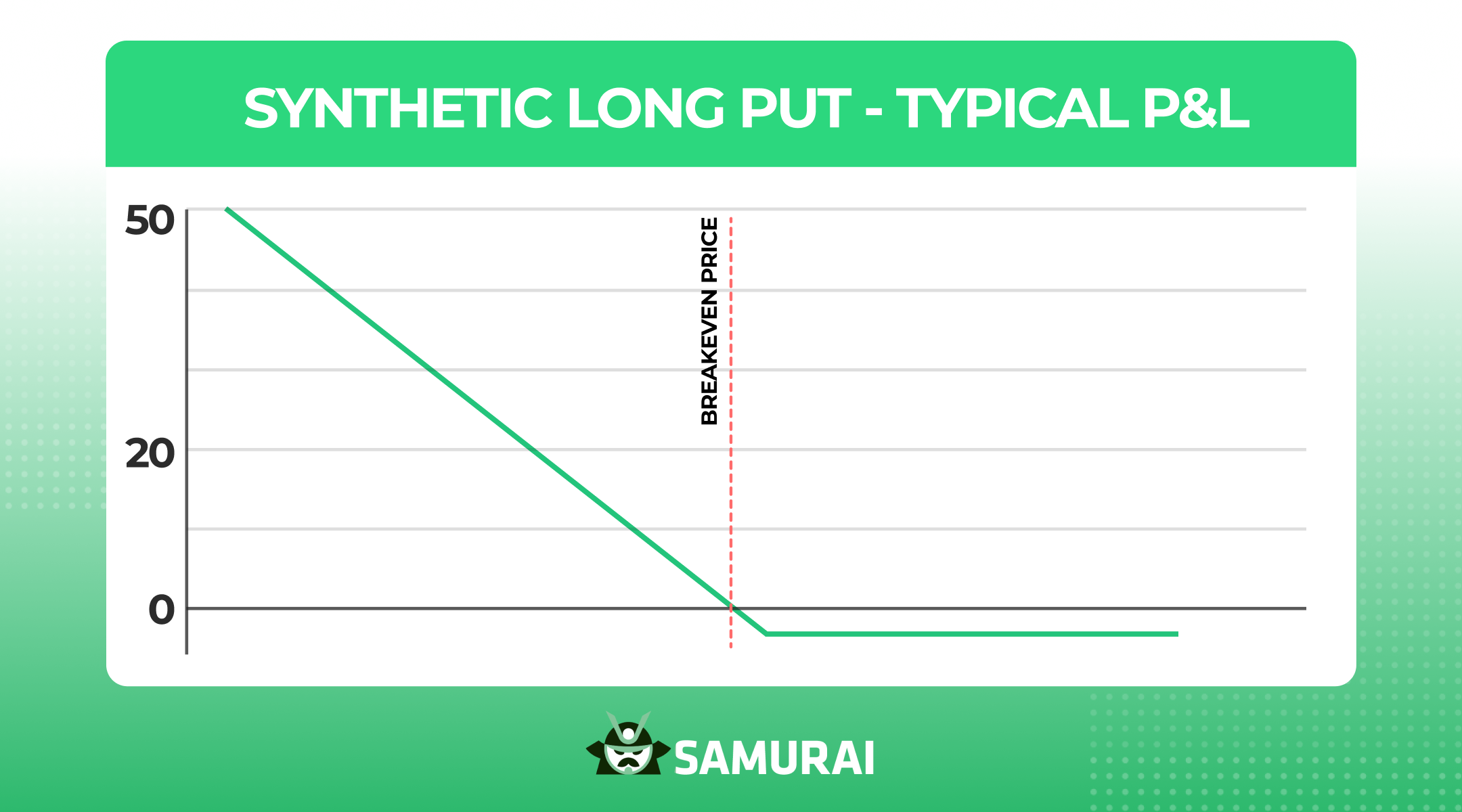

Payoff and Risk Profile

The P&L of a synthetic long put strategy will normally look like this:

The synthetic put option profits if AAPL drops. The strategy has limited loss—equal to the cost of the call—and unlimited profit potential if the stock keeps falling.

- Max loss: $6 per share

- Break-even: $215 – $6 = $209

- Profit grows as AAPL drops below $209

Cash Flow Considerations

This position starts with positive cash flow: you collect $21,500 from the short sale and spend $600 on the call. But margin is required, and you’ll need cash to buy back the stock later.

Practical Considerations

Because you’re short the stock, this options synthetic long setup:

- Requires margin

- Comes with dividend liabilities (remember: you are shorting a stock)

- Is often used when regular puts are overpriced

Synthetic Long Put Example

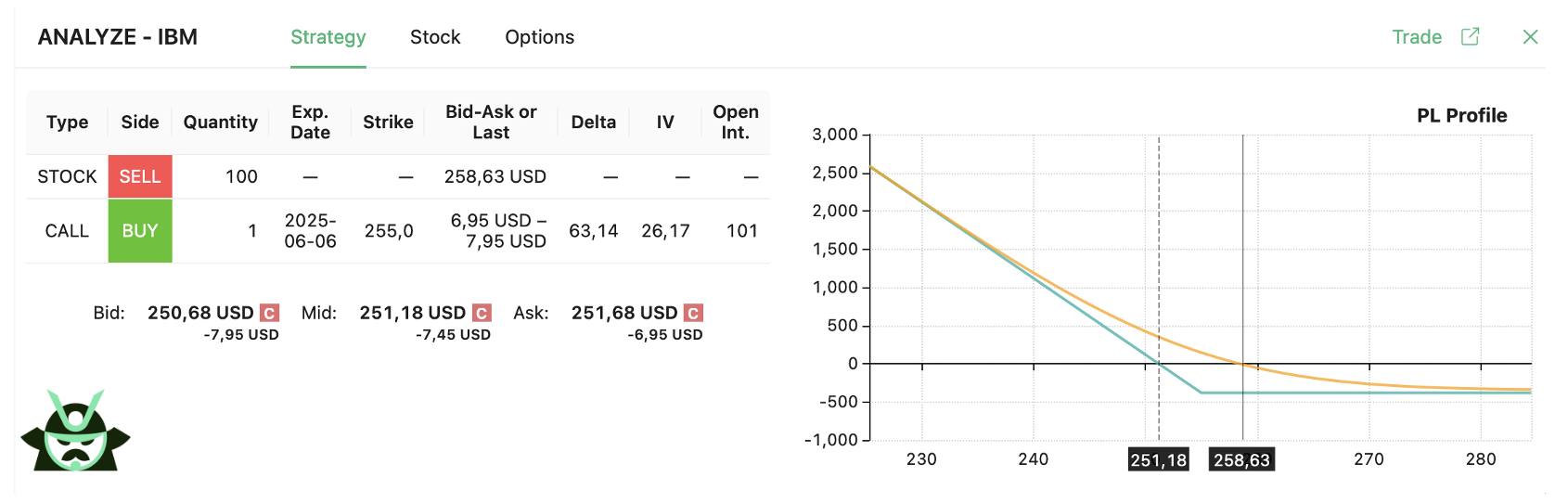

To create a synthetic long put on IBM, you could rely on our married call feature and:

- Sell short 100 shares of IBM at $258.63

- Buy one 255-strike call expiring in 2 weeks

The P&L chart of your synthetic long put would look like this:

As the P&L chart shows, this strategy profits if IBM drops below $251.18 by expiration. The maximum loss is below $500, while profits increase in a linear way as the stock continues to fall.

The Synthetic Short Put

To create a synthetic short put, you:

- Buy the stock

- Sell a call option at the same strike

Say MSFT is trading at $375. You buy 100 shares and sell one 375-strike call for $10. This setup mimics the payoff of a regular short put at the 375 strike.

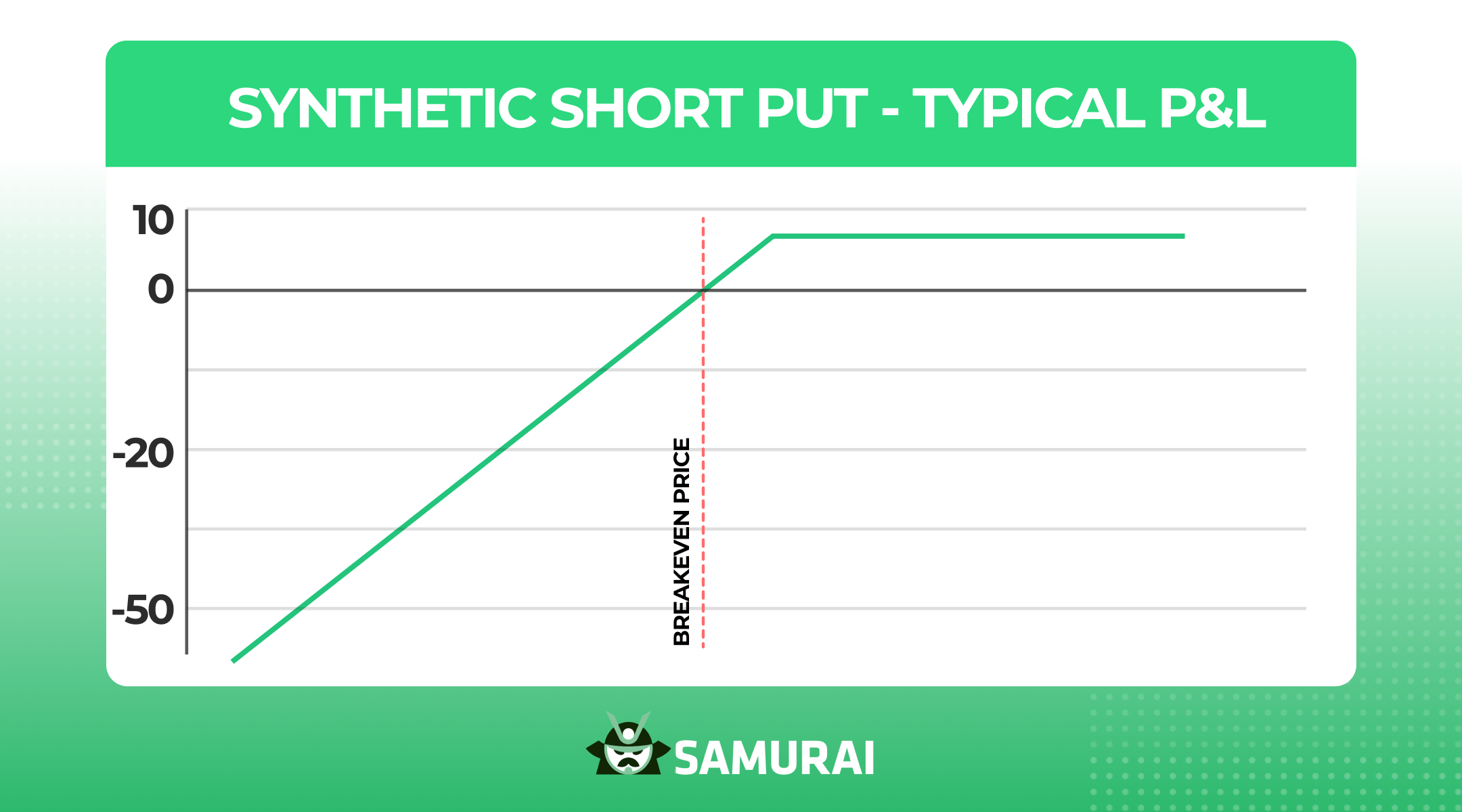

Payoff and Risk Profile

Normally, the P&L chart of a synthetic short put strategy will have this shape:

This synthetic put has limited profit—the $10 premium from the call—and unlimited downside risk if the stock collapses. If MSFT stays above $375, you keep the shares and the premium. But if it drops:

- Your loss grows as the stock falls

- Break-even = $375 – $10 = $365

- Max loss happens if MSFT goes to zero (you lose your full initial investment minus the call premium). However, realistically, the broker will close your position at some point due to the margin call system.

Cash Flow and Capital

You need capital upfront to buy the stock. The call premium helps, but doesn’t offset much. Compared to a standard short put, this version requires more cash and carries real stock risk.

Use Cases and Drawbacks

This synthetic put option setup works for bullish traders who want extra income. But it’s risky in falling markets. It’s not like an options synthetic long—here, your loss can be huge if the stock tanks. It works best when you expect the stock to stay flat or go up.

Synthetic Short Put Example

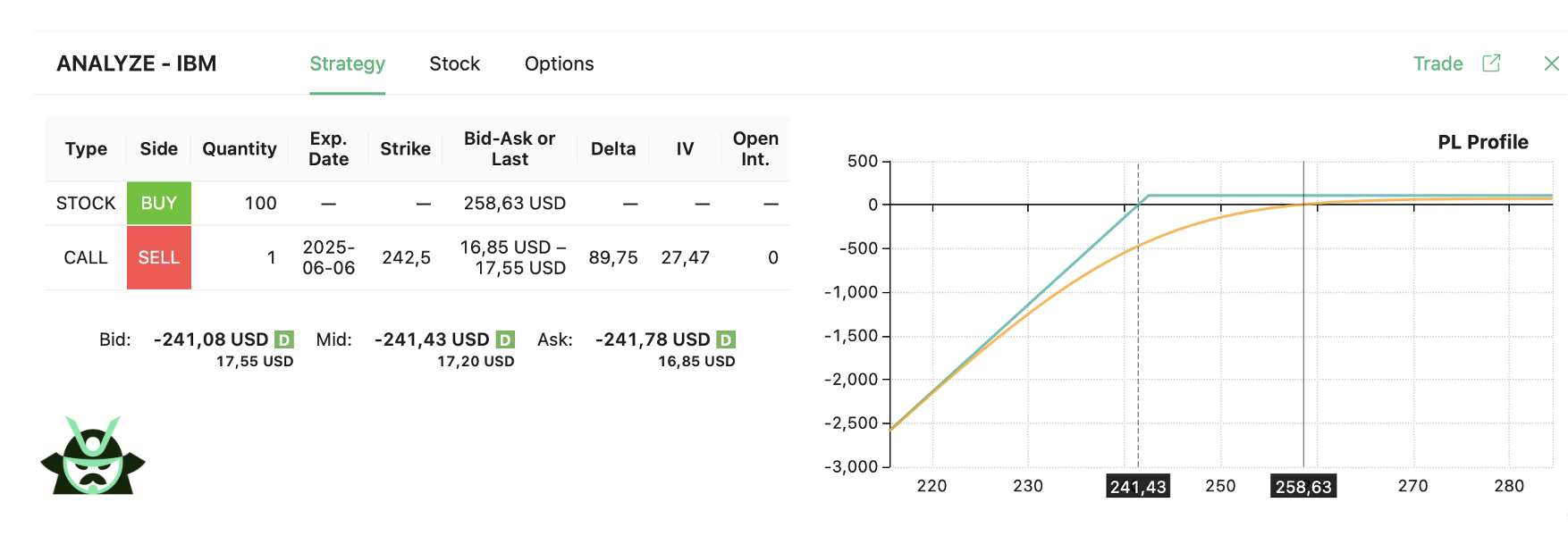

To create a synthetic short put on IBM, you could rely on our custom scan feature and:

- Buy 100 shares of IBM at $258.63

- Sell one 242.5-strike call expiring in 2 weeks

The P&L chart of your synthetic short put would look like this:

As the P&L chart shows, this strategy profits if IBM stays above $241.43 by expiration. The maximum gain is close to $100, while the losses increase in a linear way below your breakeven point.

Comparing Synthetic Long and Short Puts

First of all: a synthetic long put is bearish, while a synthetic short put is bullish. Same structure—stock plus call—but totally different direction and risk profile.

Here’s how they compare:

Feature | Synthetic Long Put | Synthetic Short Put |

Directional Bias | Bearish – profits if stock falls | Bullish – profits if stock rises or stays flat |

Capital Outlay | Positive cash flow upfront | Requires cash to buy the stock |

Risk/Reward | Limited loss, theoretically unlimited profit | Limited profit, unlimited loss (with likely margin call if things go wrong for you) |

Pick your version based on the setup that fits your view. If you're bearish and can short, the synthetic put option built with a long call and short stock (the options synthetic long) might suit you. If you want income and expect the stock to hold up, the short version works—but be ready for the downside if you’re wrong.

You can read about different synthetic options strategies on our blog, such as the synthetic short straddle and others.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.