Synthetic Short: An Options Alternative to Short Selling a Stock

Published on April 23, 2025(Last updated on November 11, 2025)

Reviewed by Leav Graves

A synthetic short offers traders a flexible way to bet against a stock without short selling. But how does a synthetic short position work, and what makes it different from simply short selling shares? From expiration constraints to the elimination of borrowing fees, this article tells you all about synthetic shorts and why they’re a valuable trading strategy.

KEY TAKEAWAYS

- A synthetic short stock position is created by shorting a call and buying a put at the same strike and expiration.

- The risk/reward profile is nearly identical to shorting stock, but with key differences (expiration constraints, no margin requirements, no borrowing fees). This strategy is often used for speculation, hedging, or as part of a collar strategy.

- While it offers substantial potential gains if the stock drops, losses are theoretically unlimited if the stock rises.

Understanding the Synthetic Short Stock Strategy

The synthetic short stock strategy is an options trade setup that mimics the risk and reward of shorting a stock. It involves selling a call option and buying a put option with the same strike price and expiration. This combination creates a synthetic short position, offering traders a flexible alternative to short selling.

How It Works

By shorting a call, you take on the obligation to sell the stock at the strike price if assigned. Buying a put, on the other hand, gives you the right to sell the stock at the same strike price. Together, these positions simulate the profit/loss profile of a short stock position without actually borrowing shares.

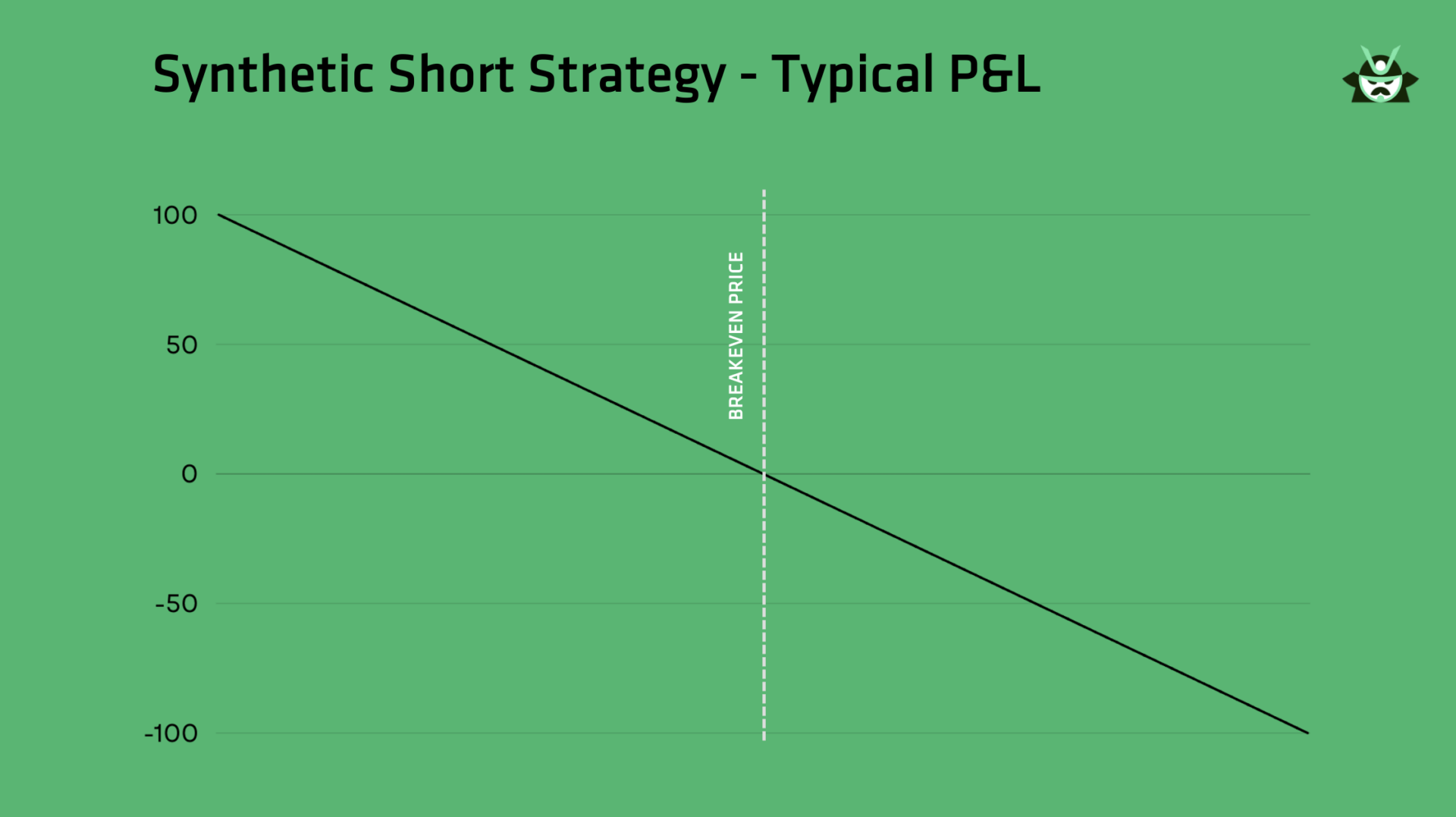

Ideally, the P&L of a synthetic short stock position will look like the graph below:

Comparing Synthetic Shorts to Short Stocks

Synthetic shorts come with several advantages over shorting stocks directly, such as:

- No need to locate or borrow shares, eliminating constraints of availability.

- No dividend payments for borrowed shares.

- No margin interest on the position.

However, synthetic shorts have a key limitation—the position only lasts until the options’ expiration. After that, the synthetic short position disappears unless you roll it into a new term.

While this strategy replicates shorting stock using options, other synthetic strategies exist. For example, a synthetic short call can be created by selling short shares and selling a put, while a synthetic short put involves buying shares and selling a call. These variations serve different trading goals but share the concept of using options to replicate directional exposure.

Going back to the synthetic short position, this strategy is ideal for traders who anticipate a short-term decline in a stock’s price, offering flexibility without some of the hassles tied to traditional short-selling.

Max Gain, Max Loss, and Breakeven

Moving on, let’s see how the profit, loss, and breakeven points work for a synthetic short strategy. These three factors are critical to understanding the risks and rewards when entering a synthetic short position.

Max Gain

The maximum gain in a synthetic short occurs if the stock price drops to zero by the expiration date. This is the best-case scenario because you have the right to sell the stock at the strike price through your long put. Since the stock becomes worthless, you can effectively buy it at $0 and sell it at the strike price, resulting in a substantial profit.

The formula for your max profit with the synthetic short stock position is the following:

Profit = Strike price – Net debit paid(if you paid upfront).Profit = Strike price + Net credit received(if you received upfront).

Max Loss

The maximum loss is unlimited, just like with actual short selling. If the stock’s price skyrockets, the short call gets assigned, forcing you to sell at the strike price while buying at the soaring market price. This creates significant losses.

For instance, let’s say the stock rises to $200 while your strike price is $100. You’re obligated to sell at $100, incurring a massive loss on each share. If the trade was set up for a net debit, this adds to your loss. If for a net credit, it reduces the loss slightly.

Theoretically, losses can be infinite if the stock price keeps rising.

Breakeven

This strategy breaks even depending on whether you entered for a net debit or net credit:

- If set up for a net debit:

Breakeven = Strike price – Net debit paid - If set up for a net credit:

Breakeven = Strike price + Net credit received

What You Should Keep in Mind

- Max Gain: Stock at $0; profit depends on the net debit/credit.

- Max Loss: Unlimited if the stock price surges.

- Breakeven: Strike price adjusted by the net debit/credit at entry.

Understanding these metrics will help you evaluate if a synthetic short position aligns with your risk tolerance and trading goals.

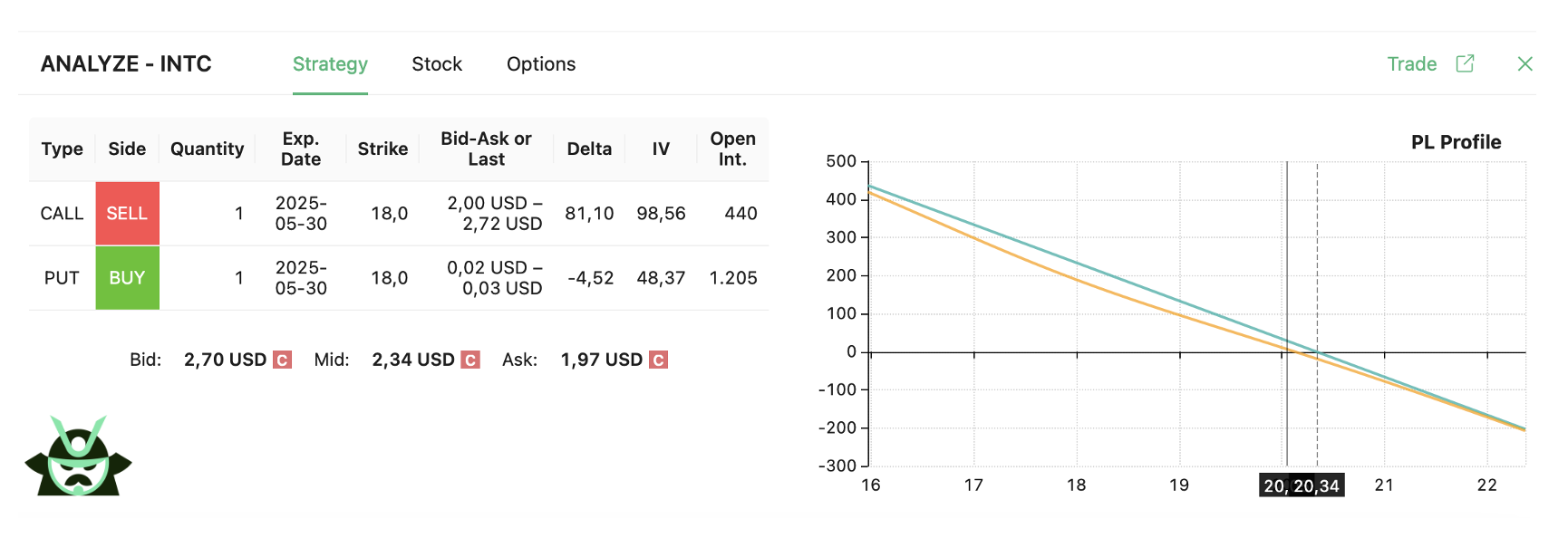

Real Market Example: Synthetic Short on INTC

Here’s a real example of a synthetic short trade found using our custom scan feature. Let’s say INTC is trading at $20.05. You could create a synthetic short stock position by:

- Selling 1 INTC 18-strike call expiring in one week

- Buying 1 INTC 18-strike put expiring in one week

The P&L chart of your synthetic short strategy would be the following one:

This setup simulates a short position in the underlying. As shown in the P&L profile, your losses grow as INTC rises, while profits build steadily if the stock drops below $20.34. Your max loss is unlimited to the right, but so is your profit on the other side of the chart.

Volatility, Time Decay, and Risks

There are other factors to consider beyond the mere price of the underlying asset in a synthetic short stock position. Volatility, time decay, and risks like early assignment or expiration uncertainty play important roles in how this strategy operates.

Volatility

Volatility is typically not a significant consideration for synthetic shorts. Since the strategy involves both a long and short option at the same strike and expiration, any changes in volatility levels tend to offset each other. This balance keeps volatility from having a major impact on the position’s performance.

Time Decay

Time decay, or the gradual loss of an option’s value as expiration nears, usually cancels itself out in a synthetic short. The loss in value from the short call matches the gain in value from the long put, assuming the underlying stock isn’t moving. However, if the stock price is declining, the put may gain value faster than the call loses value, giving the position an edge.

Assignment and Expiration Risks

Assignment risk is more significant in this strategy. The short call may be assigned early, requiring you to deliver shares. This commonly happens shortly before a stock’s ex-dividend date. If you’re not prepared for an early assignment, this could lead to unexpected complications or losses.

With expiration, risks can arise if one leg of the synthetic short position is exercised (or assigned) while the other expires. This could inadvertently leave you with a short stock position. Additionally, you won’t know for certain whether assignment has occurred until the Monday following expiration. Such scenarios demand careful attention to expiration details, especially if you're not using protective tools like an OCO bracket, which can automate exits and reduce the risk of assignment surprises.

When to Use the Synthetic Short Stock Strategy

With a better idea of how the synthetic short stock strategy works, we can take another step to identify when it might be the right choice for your trading needs—and when it’s best to avoid.

When to Consider It

A synthetic short can be a great option in a few situations:

- If you expect a stock to decline but don’t want the complexities of shorting shares. Unlike traditional short selling, there are no stock borrow fees or the need to locate shares.

- If you need an alternative to short futures contracts. This strategy can offer a similar outcome without involving futures markets.

- If you seek a temporary hedge for an existing stock position. Synthetic shorts can effectively manage short-term downside risks.

If you prefer a more conservative bearish setup that still benefits from limited downside movement, check out our guide on the short put, where we explain how selling puts can generate income while positioning you to buy quality stocks at a discount.

When to Avoid It

Despite its benefits, the synthetic short isn’t always the right fit:

- If you’re uncomfortable with assignment risk. The short call in this strategy could be assigned early, potentially forcing you into a short stock position at an inopportune time.

- If stock borrow fees aren’t a factor. When borrowing shares to short is cheap and simple in your trading account, traditional short selling might make more sense.

- If options bid-ask spreads are too wide. Large spreads can significantly eat into your profits, making this strategy less appealing.

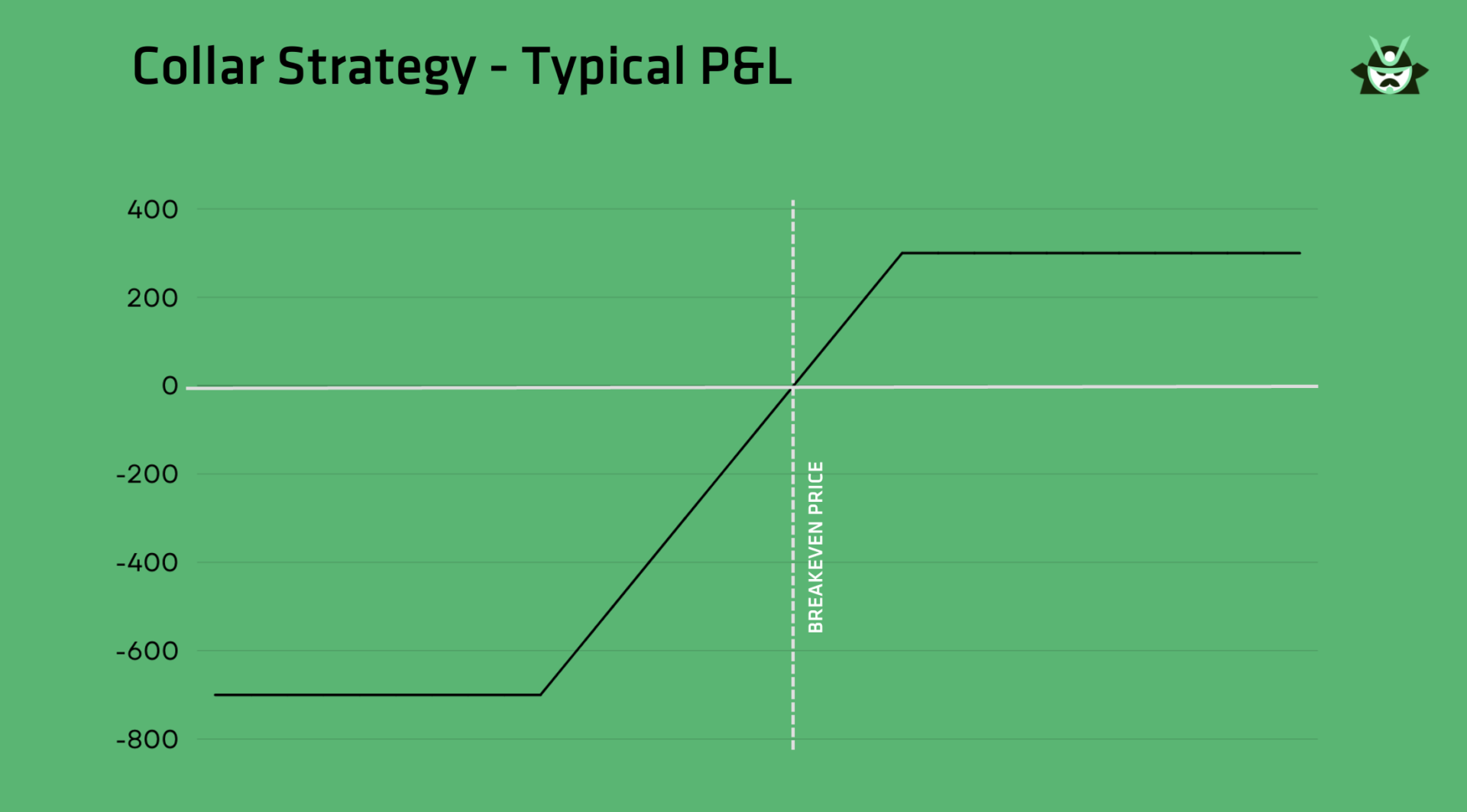

Synthetic Short Stock vs. Collar Strategy

One additional point we’d like to address is to show you how you could tweak your open synthetic short stock strategy to adapt if the market turns against you. While you may not have included an out-of-the-money (OTM) call in your initial setup, you always have the option to adjust by transitioning your synthetic short into a collar (a strategy available on our screener for the options market).

A synthetic short stock typically involves selling a call and buying a put at the same strike price, effectively mimicking the behavior of shorting a stock. However, if the trade starts moving against you and the risks become uncomfortable, you can add 100 long shares of the stock to create a collar options strategy. By doing so, you limit your losses while accepting that your potential profits are capped.

The P&L graph of your newly-established collar would look like this:

Here’s the adjusted structure:

- Synthetic Short Stock: Short call + long put. A purely bearish position.

- Transition to Collar: Add 100 long shares to the synthetic short. This cushions potential losses by combining options with stock ownership.

This adjustment works similarly to a safety net. It allows you to manage downside risk while maintaining some control over the position. For instance, even though you didn’t sell an OTM call initially, converting your setup into a collar can provide a hedge if the stock rises unexpectedly.

The ability to shift your synthetic short position into a collar gives you flexibility. It’s ideal for managing unexpected moves in the market while still working within the framework of your options strategy. For traders looking to profit when prices stay within a range rather than move sharply, the short strangle offers another powerful way to collect premium with defined boundaries for risk and reward.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.