Synthetic Straddle – How to Create One Using Long Calls or Long Puts

Published on May 19, 2025(Last updated on November 11, 2025)

Table of Contents

Reviewed by Leav Graves

Table of Contents

A synthetic straddle is a way to mimic a classic long straddle without using both a call and a put. But how exactly does that work? And what's the difference between a long call synthetic straddle and its put-based counterpart? This article breaks down both setups—simply and step by step.

KEY TAKEAWAYS

- A synthetic straddle, either in the long call or long put version, is a two-legged options strategy that mimics a classic long straddle by using synthetic components.

- A long call synthetic straddle involves a short underlying position and two long calls, creating a long volatility setup.

- A long put synthetic straddle uses a long underlying and two long puts, making it a bullish synthetic position with similar long volatility exposure.

What Is a Synthetic Straddle?

A synthetic straddle is a two-legged options strategy that acts like a classic long straddle, but it builds the position using a mix of stock and options instead of a call and a put. The payoff is the same: limited loss, unlimited potential in either direction. Same P&L shape, different construction.

Traders build a synthetic straddle for a few simple reasons:

- It can use less capital, depending on the setup

- Some accounts have better margin rules for stock + options combos

- It allows more flexibility, especially when one leg (call or put) is overpriced

There are two main ways to do it:

- A long call synthetic straddle, which includes a short stock position and two long calls

- A long put synthetic straddle, made of a long stock position and two long puts

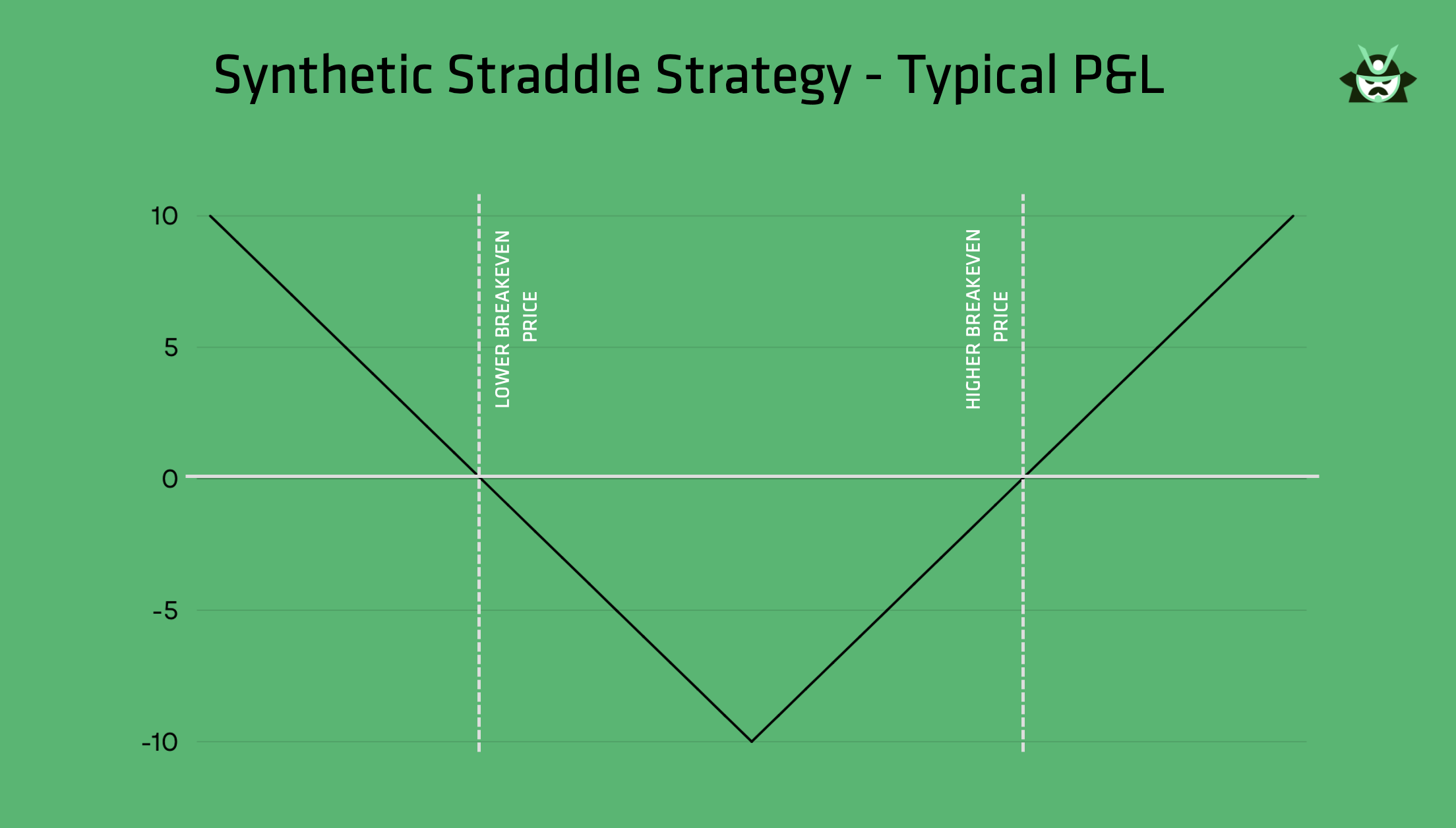

In both cases, the typical profit and loss (P&L) chart of your synthetic straddle will look like this:

As you can see, the P&L has the same “V” shape that we saw when we talked about the long straddle strategy (which, by the way, is one of the strategies available on our screener for the options market). You get the same exposure, just with different tools. If you’d like a quick refresher on the traditional setup, our full guide on the straddle option strategy covers how it works, when to use it, and how its payoff compares to synthetic versions like this one.

Long Call Synthetic Straddle

A long call synthetic straddle combines two long calls with a short position in the underlying. It mimics a regular straddle but builds the “put side” synthetically. Here’s how the math works:

- Classic straddle = long call + long put

- Synthetic put = short stock + long call

- Long call synthetic straddle = short stock + 2x long call

To build it:

- Short 100 shares of the stock

- Buy 2 call option contracts (assuming each covers 100 shares)

Correct sizing is key. Your short stock position should cover half the exposure of your long calls. If you’re long 2 call contracts (200 shares total), you short 100 shares.

Market Outlook and Use Case

This version of the synthetic straddle is often used when:

- You expect a large move (up or down)

- You’re fine with having a bearish bias

- You want to receive cash upfront from the short sale

Pros and Cons

Here are the main pros and cons to know regarding the long call synthetic straddle strategy:

Pros | Cons |

Can be cheaper than a traditional straddle | Shorting may be restricted or come with extra costs |

Generates upfront cash from the short position | You’ll be on the hook for dividends if the stock pays them |

Limited loss with potentially unlimited profit | Requires active monitoring due to short stock risk |

Long Call Synthetic Straddle Example

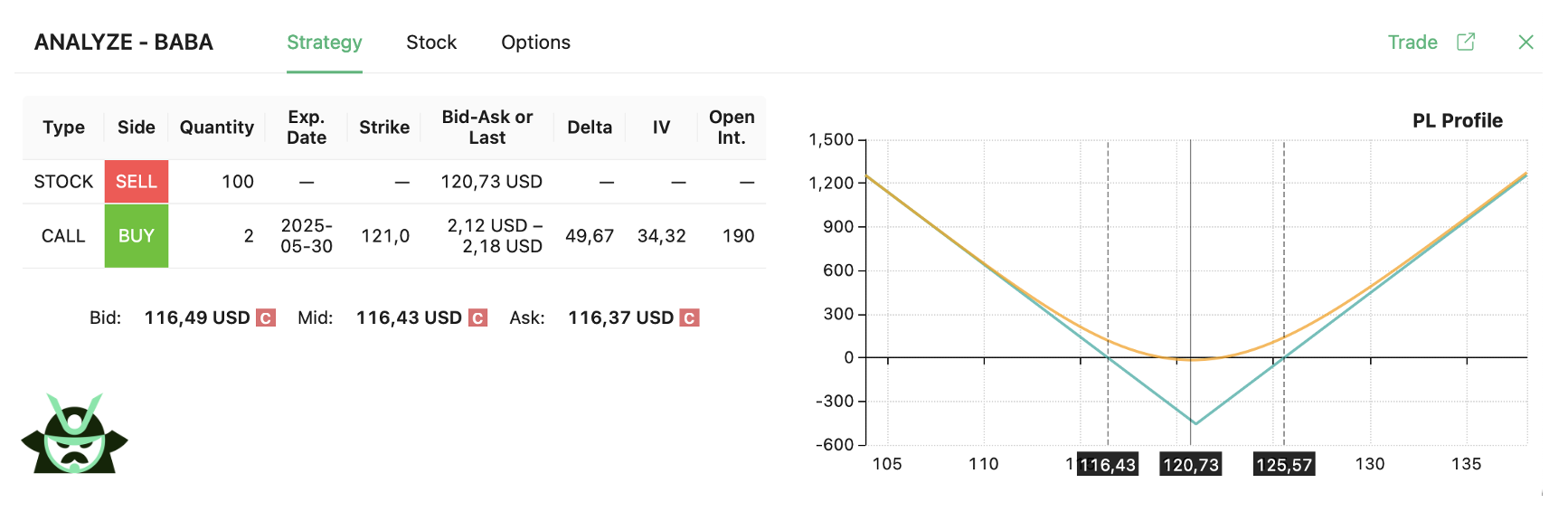

You can trade a long call synthetic straddle like this using our custom scan feature. Let’s say BABA is currently trading at $120.73. To build the strategy at the 121 strike:

- Short 100 shares of BABA

- Buy 2 BABA 121-strike call options, expiring in a week

This setup mimics a traditional long straddle using short stock and calls, as you can see in the P&L below:

If BABA makes a big move in either direction, the trade profits. If the stock stays flat, you hit max loss - visible at the bottom of the “V” in the chart. As shown in the P&L chart, the breakeven points are $116.43 and $125.57. If BABA moves outside this range, your profit potential increases with no cap.

Long Put Synthetic Straddle

A long put synthetic straddle, instead, uses a long stock position and two long puts. This time, you’re mimicking the call side of a regular straddle with a synthetic call. The structure looks like this:

- Classic straddle = long call + long put

- Synthetic call = long stock + long put

- Long put synthetic straddle = long stock + 2x long put

To build the position:

- Buy 100 shares of the stock

- Buy 2 put option contracts (each covering 100 shares)

Make sure the sizing is correct: 2 puts give you 200-share exposure, which pairs with 100 shares long.

Market Outlook and Use Case

This setup still bets on volatility. The difference is you're long the stock, so there’s a natural bullish bias. It’s also easier to manage for most retail traders, since no shorting is required. That alone makes it the preferred version in many cases.

Pros and Cons

Here’s a quick pros and cons table regarding the long put synthetic straddle:

Pros | Cons |

Easy execution | May require large initial capital (buying stock) |

Dividend collection from long stock | Cash tied up in the underlying position |

Limited loss and unlimited profit potential | Requires full exit of stock and options to close position cleanly |

Long Put Synthetic Straddle Example

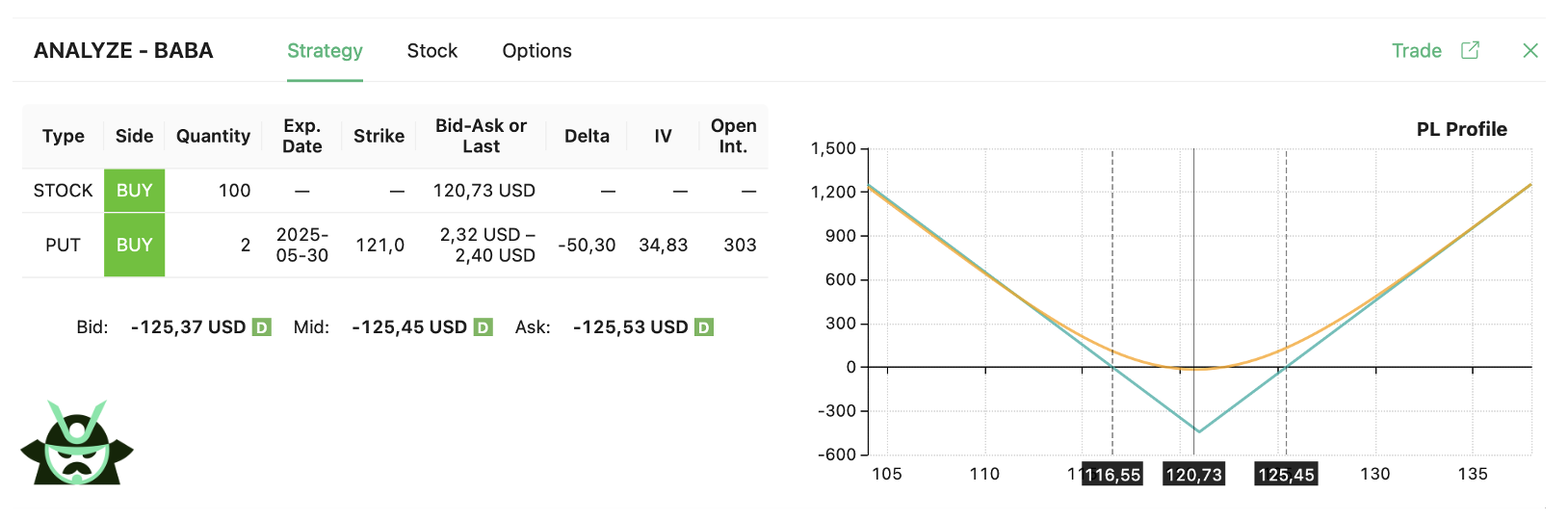

You can also trade a long put synthetic straddle using our custom scan feature. In this case, BABA is still trading at $120.73, and you want to build the strategy at the 121 strike:

- Buy 100 shares of BABA

- Buy 2 BABA 121-strike put options, expiring in a week

This structure uses long stock and puts to create a synthetic long straddle. Once again, you can take a look at the strategy’s P&L chart below:

Once again, you gain from strong moves in either direction. If the price stays near the strike, you’ll experience the maximum loss.

As shown in the P&L chart, the breakeven points are $116.55 and $125.45. As BABA moves beyond those levels, the position becomes profitable.

Synthetic Straddle vs Classic Long Straddle

Both strategies aim for the same outcome: profit from big moves in either direction. The classic straddle uses a long call and a long put. The synthetic straddle swaps one of those with a synthetic equivalent—either short stock + long call (like in a long call synthetic straddle) or long stock + long put.

The payoff diagram is nearly identical, showing limited loss and unlimited profit in both cases. However, there are a few key differences (especially if you're trading a synthetic short straddle, which takes the opposite view and benefits when the underlying stays near the strike):

- Synthetic versions involve stock positions

- Margin and capital needs can vary a lot (synthetic positions are typically more expensive, since you are adding an extra stock leg)

Long Call vs Long Put Synthetic Straddle

We told you that the P&L profile of both strategies is nearly identical—but the way they’re built matters. A long call synthetic straddle uses short stock, while the long put version uses long stock.

That changes a few things:

- Shorting stock isn’t always easy or available

- Long stock ties up more cash but collects dividends

- Short stock gives cash upfront but requires paying dividends (this is something few traders know: if you short the stock, any dividends paid will be pulled from your account and passed on to the actual owner).

In practice, the choice depends on your access to capital, margin terms, and broker rules. Same strategy on paper—different trade in real life.

When to Use a Synthetic Straddle

A synthetic straddle makes sense when you expect a big move in the stock and want more control over how the position is built. It’s often used around earnings or macro events, when volatility might surge.

Traders might choose it when:

- They want a mix of volatility exposure and directional bias

- They’re limited by account type, margin rules, or capital

- One leg of the traditional straddle is overpriced, and a synthetic offers a better entry

The last case is probably our favorite as it is the most frequent case in which a trader would prefer a synthetic straddle to a regular one.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.