Disclaimer: The trades discussed in this blog reflect the author's personal strategies and decisions. These are not financial advice and should not be considered recommendations to buy, sell, or hold any financial instruments. The author is not a licensed financial advisor. Options trading carries significant risk, and readers should perform their own research or consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

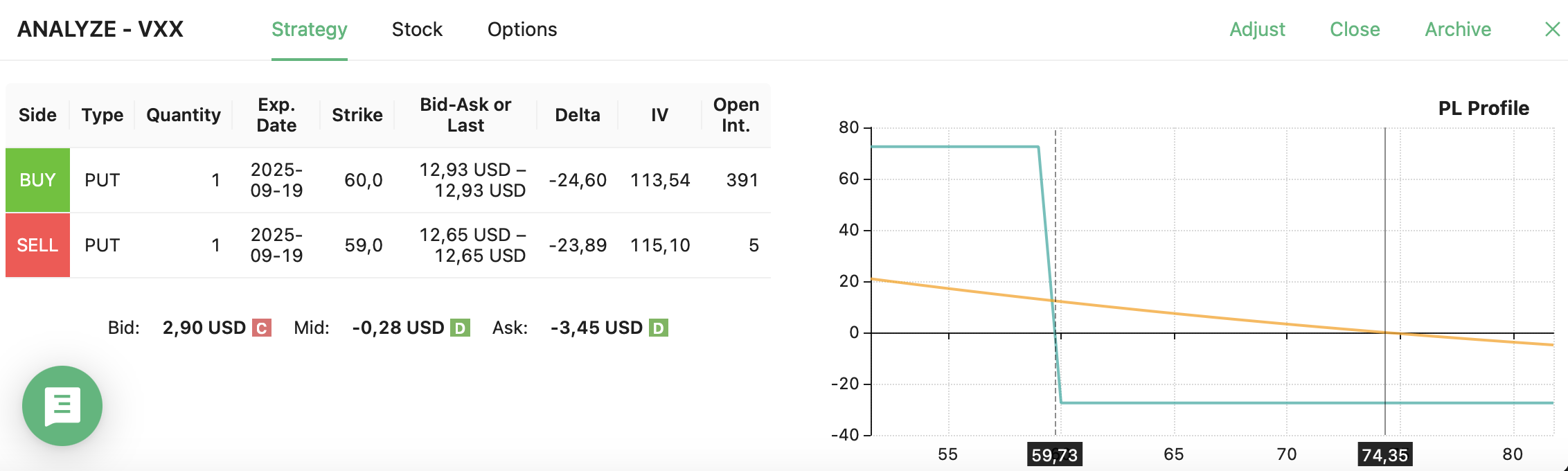

Yesterday at the close, I opened a bearish position on the iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX), which settled at $74.35. This trade was designed to express my view that the recent surge in market volatility, driven by renewed trade war fears and geopolitical anxieties, is likely to fade over time.

Rather than shorting VXX outright or purchasing naked puts, I opted for a defined-risk bearish strategy: a bear put spread. This is what I did:

- Buy 1 Put Contract: Strike Price $60, Expiration September

- Sell 1 Put Contract: Strike Price $59, Expiration September

Or, if you prefer, here is the daily price chart of the underlying asset:

This setup allows me to benefit if VXX retreats toward its historical mean or even overshoots to the downside, while capping my maximum loss to the net debit paid. My break-even sits just above $59, and I’ll likely look to close this position much earlier if the volatility crush plays out as anticipated.

Why This Strategy Makes Sense

From a macro perspective, I believe this recent volatility spike has been an emotionally driven overreaction. The ongoing trade war rhetoric, particularly between the U.S. and China, echoes familiar patterns from Trump’s first presidency. While tensions there may remain elevated, I expect de-escalation on other fronts—especially with the EU and Western allies. Any signs of normalization on these fronts should help restore market calm.

Moreover, in the unlikely event that things spiral into a deeper economic downturn or even stagflation (a scenario marked by low growth and persistent inflation), I believe the Federal Reserve’s dual mandate will guide its actions toward stabilizing the economy rather than aggressively targeting inflation. In such a policy environment, risk assets could find a supportive backdrop again, leading to reduced demand for volatility hedges like VXX.

Let’s also not forget the structural nature of VXX itself. As an ETN tracking short-term VIX futures, VXX is inherently prone to decay in calm or sideways markets due to futures roll costs. This decay accelerates in times of backwardation reversal or contango, making it an ideal candidate for bearish spreads once panic-driven spikes appear unsustainable.

Defined Risk, Asymmetrical Payoff

The beauty of the 60/59 bear put spread is that it offers a favorable risk/reward profile. My upside is limited to the $1 spread width minus the debit paid, while my downside is capped. It’s a concise expression of a broader market view, with clear exit parameters and minimal capital at risk.

If volatility fades as expected and VXX trades back toward the 50s—or lower—I plan to close the position well ahead of September expiration, locking in profits and redeploying capital into new setups.

Also, if things go spectacularly wrong for me, I will only lose less than $30 per contract, which is more than acceptable compared to a $72 potential profit.

For transparency, you can find all my trades in the public trade log.

Update – Trade Closed

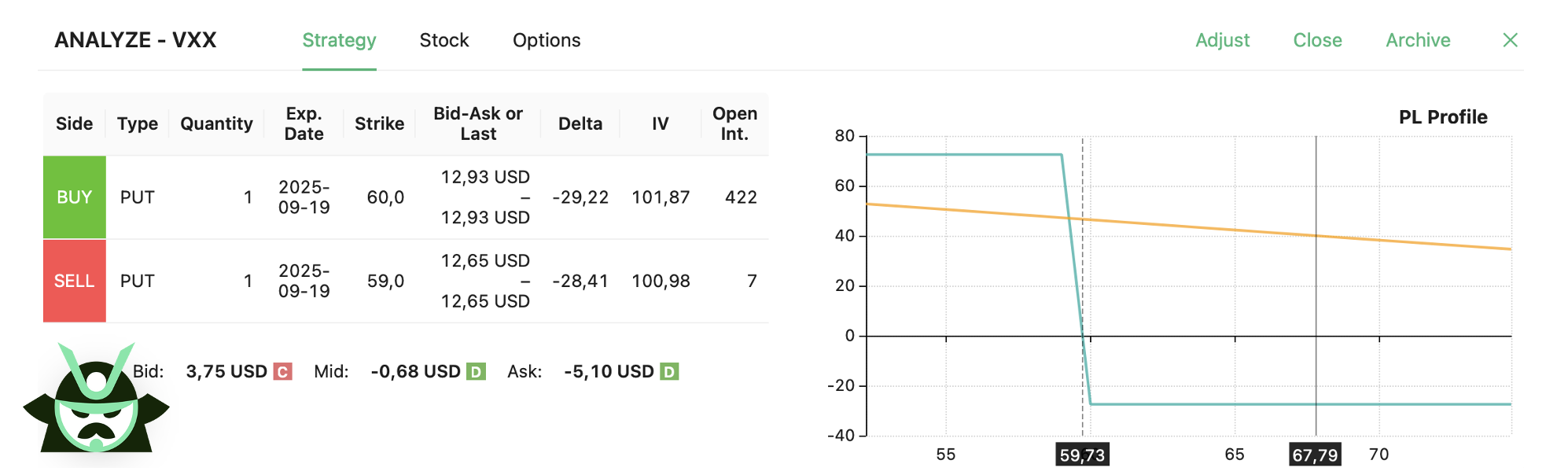

Well, that was fast. I closed the trade following Trump’s sudden U-turn on tariffs—specifically, the White House's decision to pause most tariffs for 90 days. This policy shift triggered a sharp drop in market volatility, with the VIX falling over 30% in just a few sessions. The result? A $40 profit per contract on this bear put spread in a matter of few hours.

Given that our options expired in September, the 90-day reprieve introduced new timing risks. Rather than hold and speculate on unpredictable geopolitical outcomes, I chose to lock in the win and exit cleanly while the trade was in my favor.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.