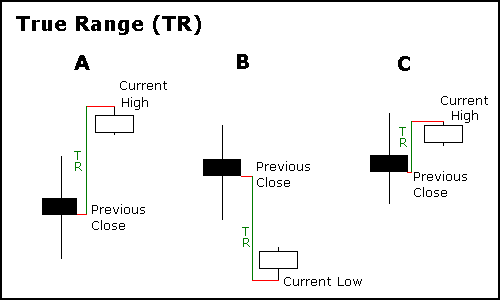

Average True Range is a stock volatility measure developed by Welles Wilder in his book "New Concepts in Technical Trading Systems". The goal of the indicator is to find the "true" movement range for a stock in order to assess its volatility. The calculation of the True Range (TR) is:

TR = The maximum of: 1. Current High - Current Low 2. Yesterday's close - Current High (Absolute value) 3. Yesterday's close - Current Low (Absolute value)

True Range Example

The ATR is usually a 14 days average of the TR value. In Option Samurai we add the ATR measure as a percent of stock price to help users understand the volatility of the stock and compare it to other stocks with different prices.

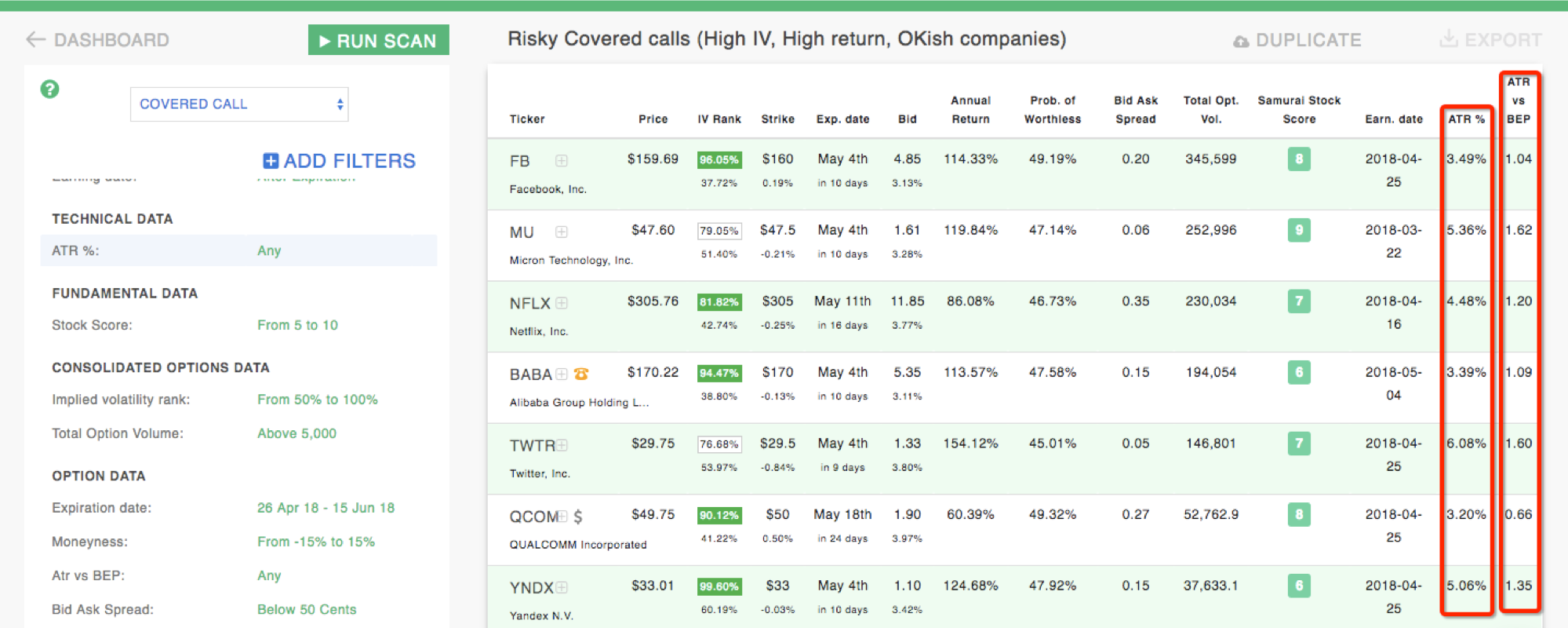

We also built 2 unique indicators:

ATR vs breakeven point - compares the ATR to breakeven point to see how many 'units' of volatility we need to pass the BE point. This is useful when buying options. and you can read more here https://blog.optionsamurai.com/the-edge-of-trading-with-atr/ .

The idea is that the higher the ATR compared to the break-even point the greater the chances of profit (even on an intraday basis). In addition, you can scan the results to find only the trades where the ATR is significantly (2x,3x,4x etc) is greater than the break-even point.

ATR Vs Strike - Compares the ATR to the strike distance to see how many 'units' of volatility we need to touch the strike. It is useful mainly to find strikes to sell in covered calls and naked puts strategy.

Leav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.

Leav GravesCEO

Leav GravesCEO