An Asian option is like a standard option, but instead of settling at a single final price, it settles at the average price over a set period. Why does that matter? It changes the cost, the risk, and who should use it. In this article, we cover the Asian option definition, how it compares to standard options, and a practical example.

KEY TAKEAWAYS

An Asian option is a contract where the payoff depends on the average price of the underlying during a set period

Asian options vs. standard options differ because standard options use one final price, while Asian options use an average, which often lowers cost and reduces extreme outcomes

Asian options are classified as “exotic options” and are often used in commodities and FX to smooth volatility and reduce the impact of short-term price spikes

Asian Option Definition and Core Characteristics

An Asian option is a contract where the payoff is based on the average price of the underlying asset over a set period, not a single price at expiration. That average is calculated using price observations taken at specific intervals, such as daily, weekly, or monthly, depending on what the contract specifies.

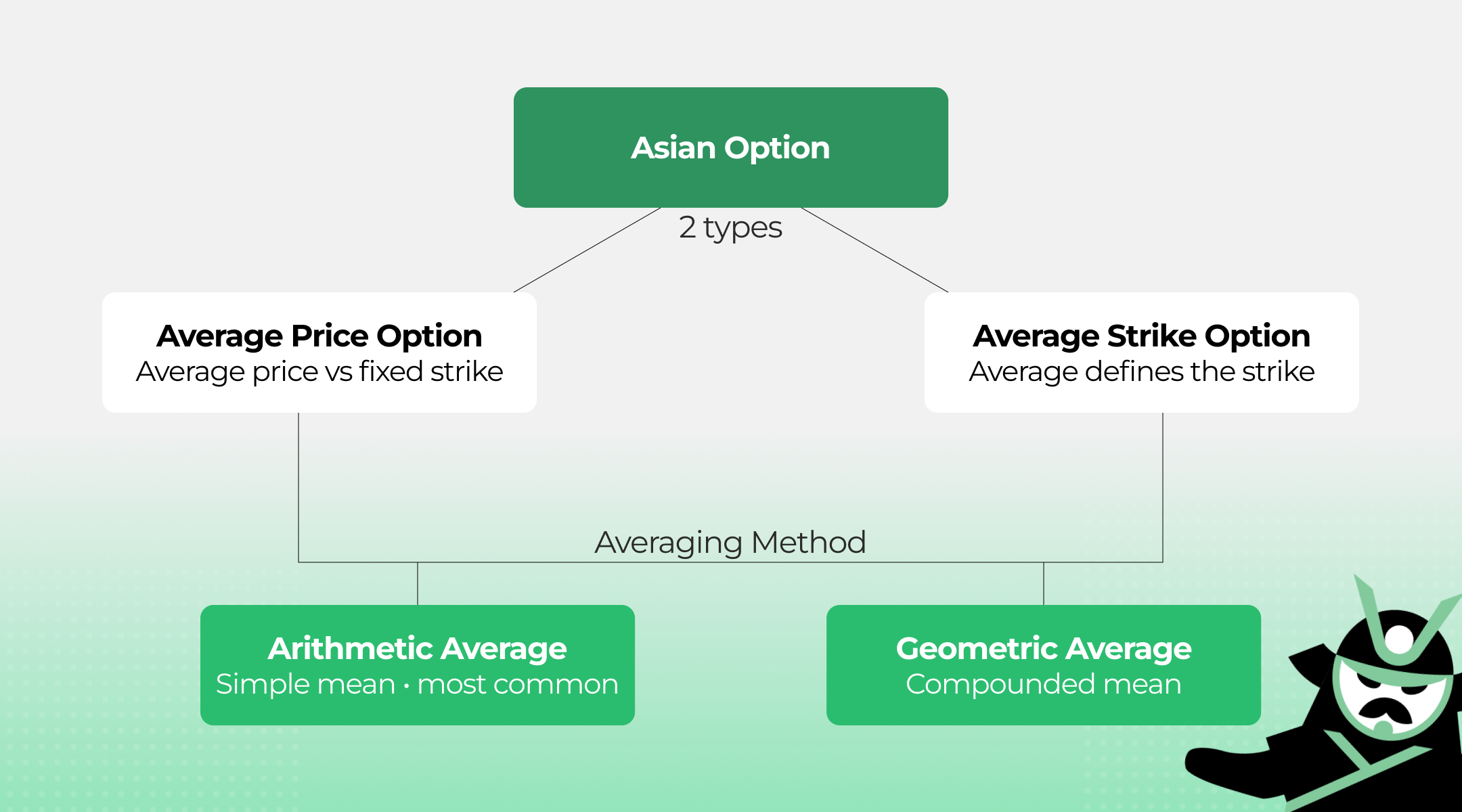

Here is a simple infographic that explains how an Asian option works:

This type of exotic option exists in 2 versions:

Average price options: compare the average price to a fixed strike price

Average strike options: use the average itself as the strike price

The average can be calculated in two ways, arithmetic (a simple mean) or geometric (a multiplied and rooted mean), with arithmetic being more common in practice. The type of average used must be defined in the contract up front.

How Asian Options Work From Observation to Payoff

When you buy an Asian option, the contract sets observation dates in advance, for example, every 30 days over a 90-day period. On each date, the price of the underlying asset is recorded. At expiration, those recorded prices are averaged, and that average determines the payoff.

If the average beats the strike price, the option pays out. If it doesn't, the loss is limited to the premium paid, just like one of the standard options you’d be able to find on our advanced options screener.

Asian Options vs. Standard Options in Risk and Pricing

The core difference is simple: a standard option's payoff depends on where the price lands on one specific day. An Asian option spreads that across many observations, so a single spike or crash doesn't decide everything.

That averaging effect reduces volatility exposure, which makes Asian options generally cheaper than standard options. The tradeoff is upside, if the price shoots up right at expiration, a standard option like the one shown in a put option payoff diagram captures that fully, while an Asian option only reflects the average.

Asian Option Example Using a Simple Price Average

Say you buy an Asian call option on oil with a $50 strike price. Prices are recorded monthly over three months: $48, $52, and $55. The average is ($48 + $52 + $55) / 3 = $51.67. The payoff is $51.67 - $50 = $1.67.

Observation

Price

Month 1

$48

Month 2

$52

Month 3

$55

Average

$51.67

Payoff (vs. $50 strike)

$1.67

With a standard option, the payoff would be based on that final $55 alone, giving $5. The Asian option pays less, but also cost less upfront. That tradeoff is exactly why Asian options are popular in commodities and FX markets, where businesses hedge against average price exposure over time, not just a single day's rate.

Gianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

Leav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders Education Leav GravesCEO

Leav GravesCEO