Condor Spreads - Using Calls or Puts to Define Risk and Target Volatility

Published on June 22, 2025 | 8 min readReviewed by Leav Graves

Condor spreads are a way to trade options while keeping both your risk and reward limited. Built with four legs using either all calls or all puts, each condor spread follows a simple structure. But why do traders choose a long condor or short one? And when is a call condor better than a put?

KEY TAKEAWAYS

- The condor spread is built with four legs using either all calls or all puts, with the same expiration and different strike prices (usually spaced at regular intervals)

- It shares the same payoff profile as the popular Iron Condor, but uses only calls or only puts - making it structurally simpler and often easier to place far out-of-the-money

- There are two main styles: long condor (profits from low volatility) and short condor (profits from large moves), each with a call or put variant

- Traders choose between call or put condors based on market liquidity and personal preferences - call condors are often easier to place far from the current price due to tighter spreads

What Is a Condor Spread?

The condor spread uses four option contracts, either all calls or all puts, with the same expiration date and evenly spaced strike prices. The structure - buy one option, sell two closer to the money, then buy another farther out - is nearly identical to the Iron Condor. The only difference is that a condor spread uses just calls or just puts, rather than mixing both. This setup defines your maximum risk and reward from the start, and is often easier to place far out-of-the-money.

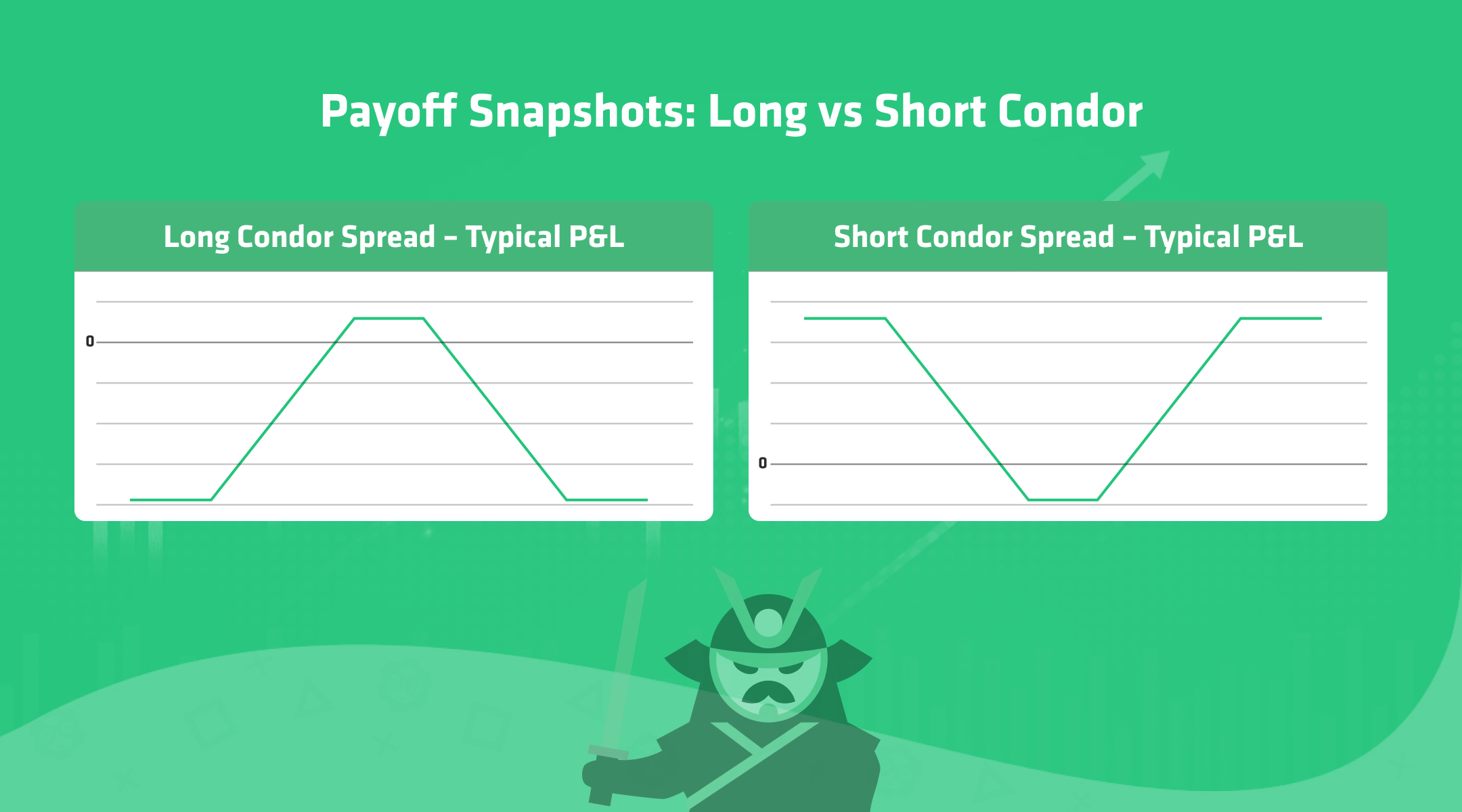

There are two types of condor option strategy setups: the long condor and the short condor. A long condor (built with either calls or puts) profits when the underlying stays within a narrow price range. A short condor profits when the underlying makes a big move outside the range.

Here’s how each version is structured:

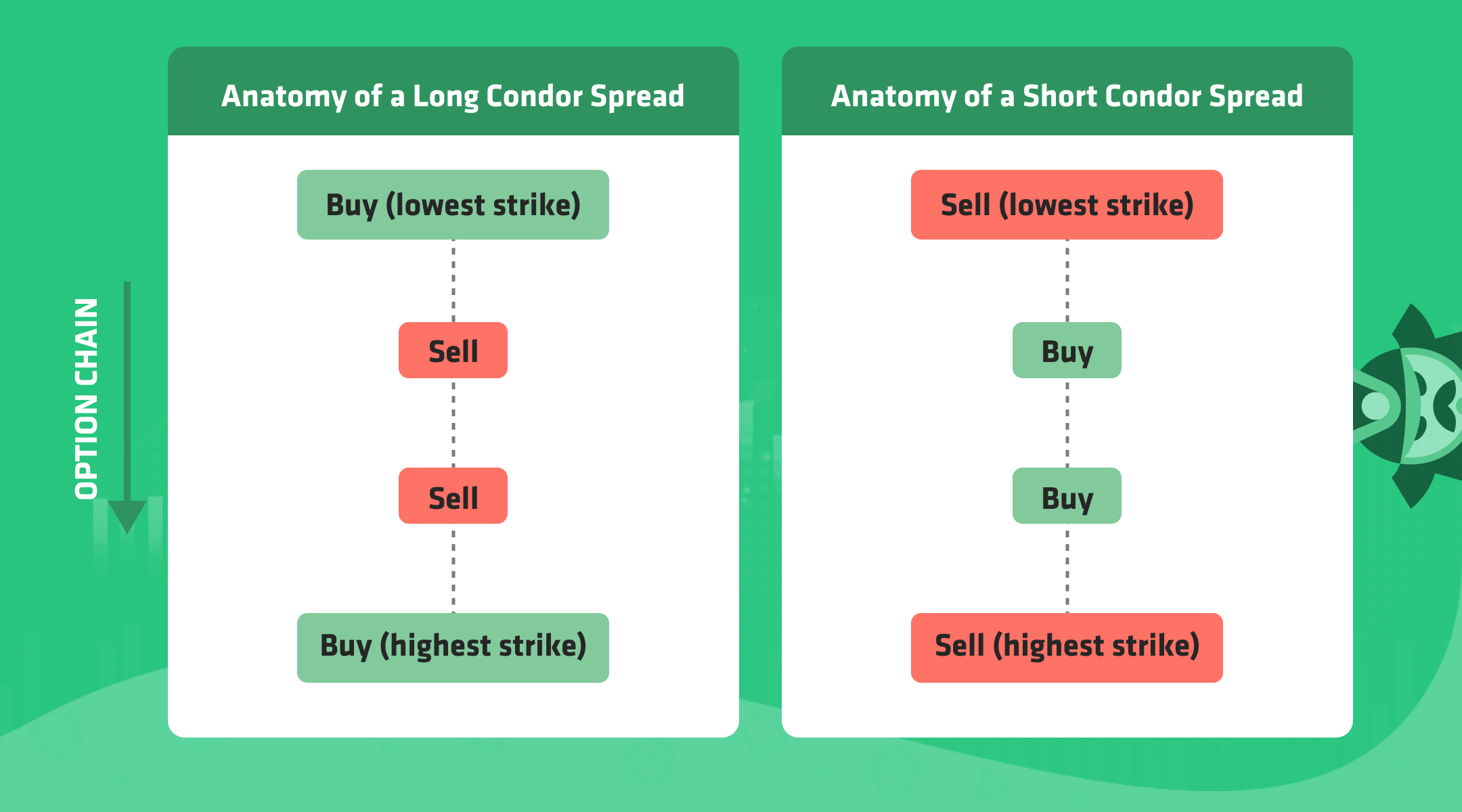

- Long condor with calls or puts: Buy the lowest strike, sell the next two strikes, buy the highest. Results in a net debit.

- Short condor with calls or puts: Sell the lowest and highest strikes, buy the two middle ones. Results in a net credit.

The call condor and put condor versions have identical risk/reward profiles. In fact, the only difference that it makes sense understanding is the one between a long condor spread and a short condor spread, as you can see below:

So, why would it make sense to choose between the call and the put variant, considering that the only difference really stands in the long/short nature of the trade? Well, most traders choose based on which side of the options chain has better pricing.

In any case, the iron condor, a mix of calls and puts, is the most popular variation of this type of strategy, and it shares the same profit/loss profile as the classic condor spread. The reverse iron condor, instead, shares the same P&L profile as the short condor spread. To see another breakout-oriented setup built for fast moves, you can review the reverse iron butterfly, which uses a tighter center and different wing structure to shape its risk profile.

Back to condor spreads: ideally, the two macro groups of condor strategies work as follows:

Here is a table summarizing the way the condor spreads strategy family works:

Condor Options Features | Long Call Condor Option Strategy | Short Call Condor Option Strategy | Long Put Condor Option Strategy | Short Put Condor Option Strategy |

1st Leg (lowest strike) | Buy Call | Sell Call | Buy Put | Sell Put |

2nd Leg | Sell Call | Buy Call | Sell Put | Buy Put |

3rd Leg | Sell Call | Buy Call | Sell Put | Buy Put |

4th Leg (highest strike) | Buy Call | Sell Call | Buy Put | Sell Put |

Net Premium | Net Debit (you pay to enter) | Net Credit (you receive upfront) | Net Debit (you pay to enter) | Net Credit (you receive upfront) |

Target Outcome | Price stays between short strikes | Price moves outside the strike range | Price stays between short strikes | Price moves outside the strike range |

Example: Long Condor Spread with Calls and Puts

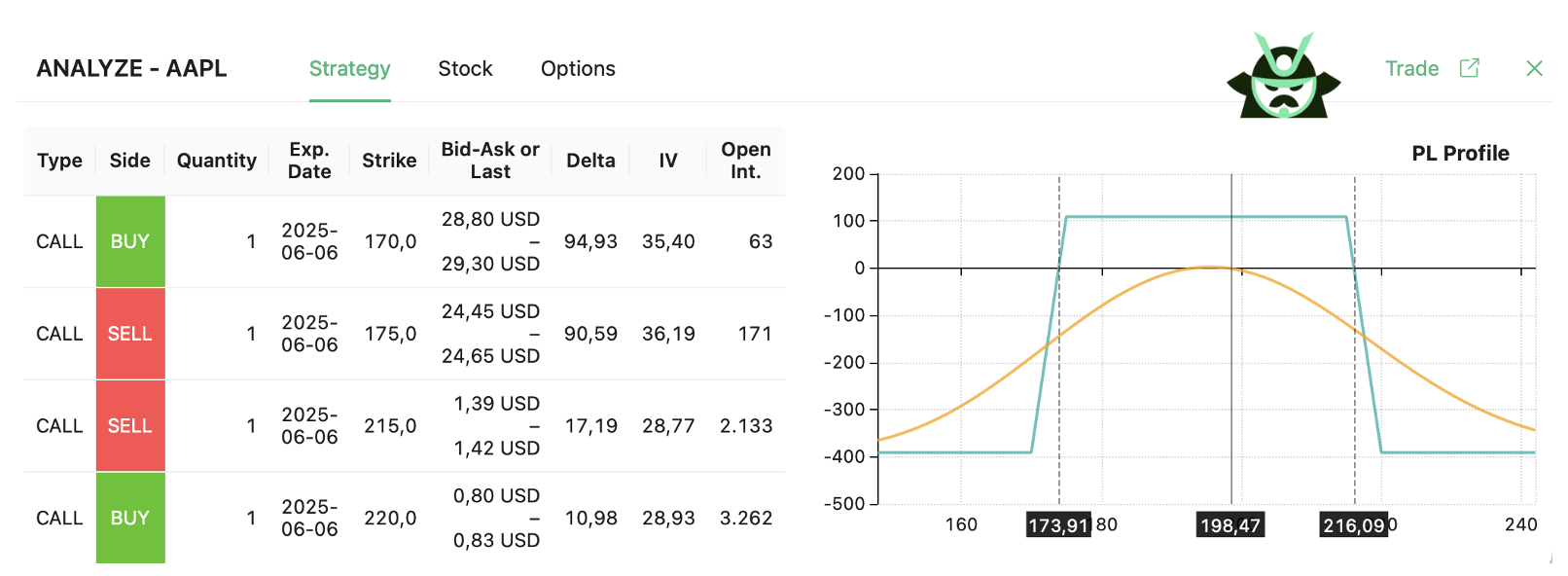

Let’s say Apple (AAPL) is trading around $198.50, and you expect it to stay relatively stable over the next month. This is a situation where a long condor spread might make sense. In this example, we’ll walk through how to build it using call options.

Here’s one way to set it up using the condor option strategy:

- Buy 1 AAPL $170 call

- Sell 1 AAPL $175 call

- Sell 1 AAPL $215 call

- Buy 1 AAPL $220 call

All four options have the same expiration date (one month from now). This setup is called a call condor, and it results in a net debit. You're paying to open the trade. The two middle strikes (175 and 215) define the range where the strategy makes money. Outside of that, you lose a fixed amount.

P&L Breakdown

Thanks to our new “Custom Scan” feature, you could build this condor option strategy and scan the market in the way you want. Your long condor spread with calls would have the following P&L profile:

Specifically, we would have:

- Max profit: Happens if AAPL expires between the two short strikes ($175 and $215). In that case, one of the short options and one of the long options expire in the money, while the other two expire worthless. The spread between the strikes locks in a fixed value, and subtracting the initial debit gives you the maximum profit.

- Max loss: Occurs if AAPL ends below $170 or above $220. You lose the net debit, which in this case is close to $400.

- Breakeven points: Around $173.91 and $219.09, based on the net premium paid.

This condor spread has a limited risk and a limited reward. In this example, you risk around $400 to make less than $100. That may sound unbalanced, but this is typical for long condor setups. You’re aiming for high probability, not high return. Most of the time, if the price stays inside the range, you’ll make something. But the payoff is small.

This is why many traders use condor options when they expect the stock to do very little over the life of the trade. You give up potential upside in exchange for defined risk and better odds.

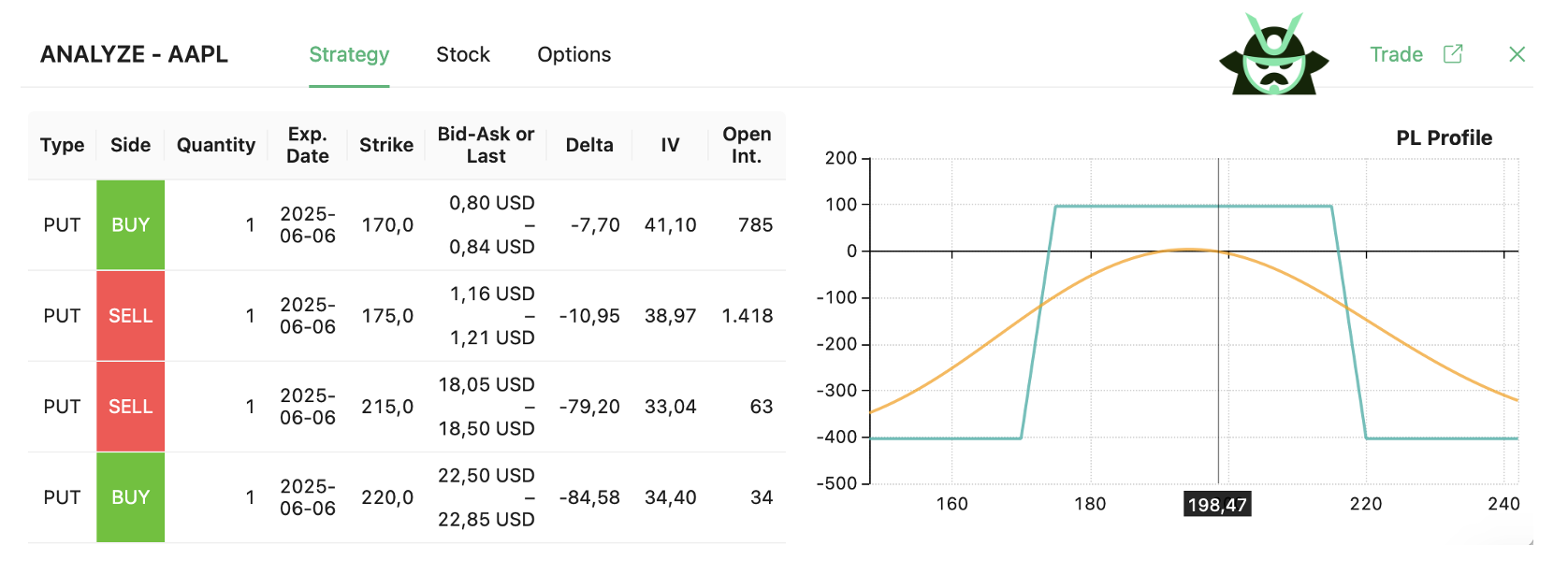

You could build the exact same condor trading setup using puts, and this is the P&L profile you would have built:

The long condor with puts gives you (pretty much) the same risk-reward profile. You just use a different set of instruments. Often, the choice between calls or puts comes down to liquidity or pricing at the time of entry. Usually if you are trying to position the strategy OTM, it will be easier to pick calls or puts (as OTM options have better bid-ask spreads).

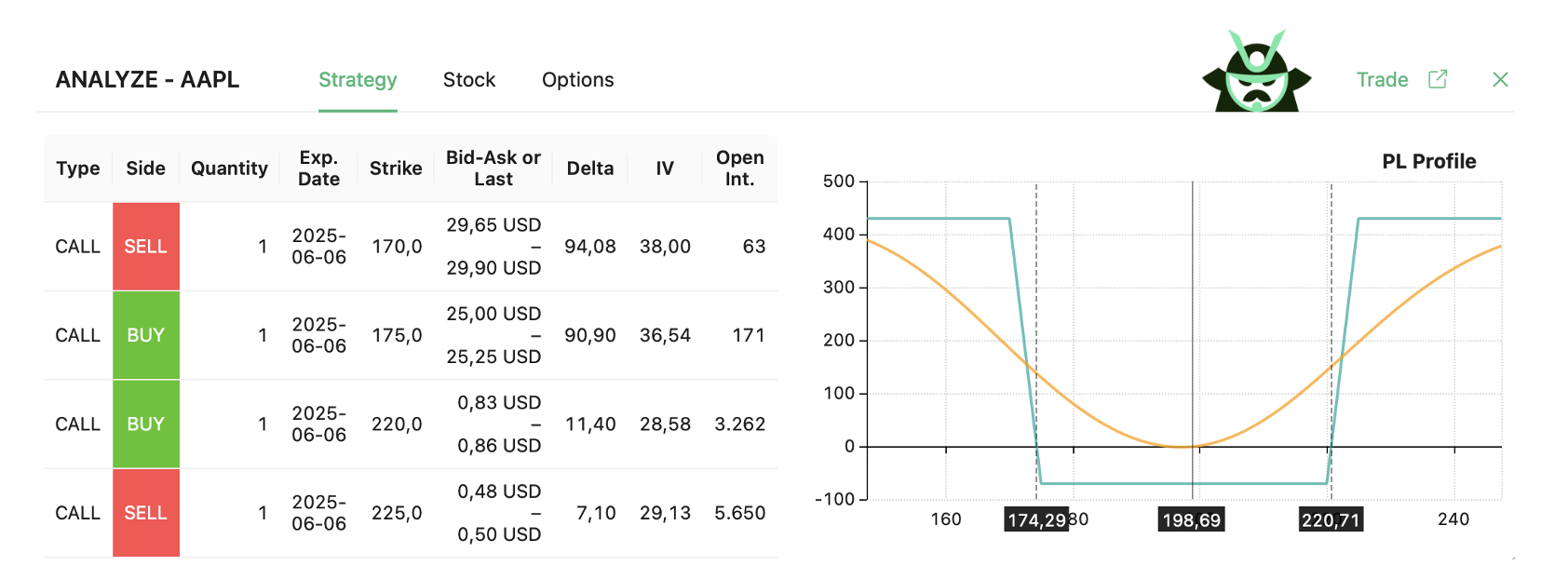

Example: Short Condor Spread with Calls and Puts

Let’s say AAPL is trading around $198.50 and you expect a big move over the next month, but you’re not sure in which direction. This is where the short condor spread comes in handy. You can use it to bet on volatility with defined risk.

Here’s how you’d set up a call condor:

- Sell 1 AAPL $170 call

- Buy 1 AAPL $175 call

- Buy 1 AAPL $220 call

- Sell 1 AAPL $225 call

All contracts expire on the same day. This structure results in a net credit, meaning you receive money when opening the trade. It’s the opposite of the long condor, and the profit/loss chart looks like a reversed iron condor.

You’ll profit if AAPL moves outside the range between the two short calls, and lose if it stays inside.

P&L Breakdown

Again, by relying on our Custom Scan feature on our options screener, you would be able to scan the market for the short condor spread strategy. Here is what your P&L for this specific short condor spread with calls would look like:

This is what you should take away from the chart above:

- Max profit: Over $400, reached if AAPL finishes below $170 or above $225

- Max loss: Close to $70, happens if AAPL stays between roughly $174.29 and $220.71

- Breakeven points: Around $174.29 and $220.71, based on the credit received

This version of the condor option strategy has a favorable reward-to-risk ratio. You’re risking $70 to potentially make over $400. But you’ll only win big if the price makes a large move outside the range. That means this is a lower-probability trade. It won’t win often, but when it does, the payoff is significant.

That’s the trade-off with this type of condor trading. You give up probability to gain a better return. These setups are often used ahead of earnings, major economic events, or any time you expect sharp movement but don’t want to guess the direction.

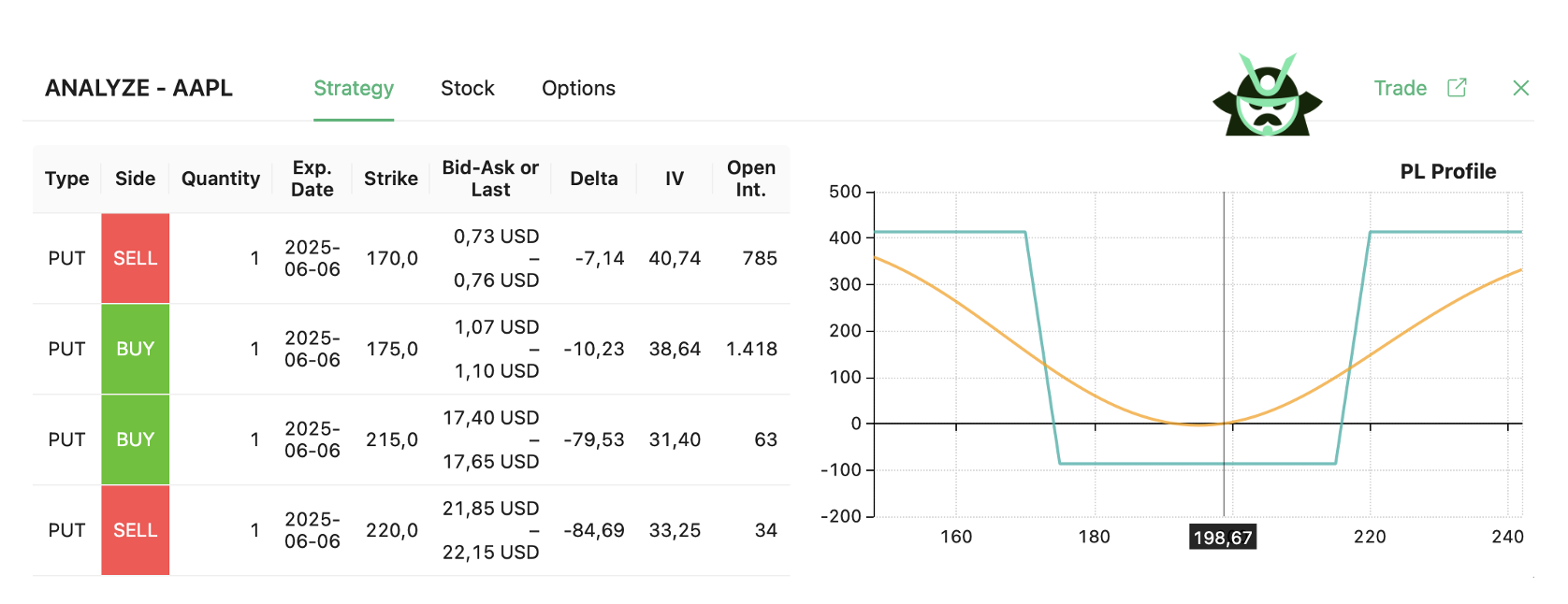

You could build the same condor spread using puts, and you would get a P&L that would look like this:

This is the short condor with puts. The risk and reward are identical to the call version. In fact, the payoff chart is the same. The difference is execution. Some traders prefer puts for margin reasons, or because the put options chain is more liquid at certain strikes.

Both call and put versions are valid. The decision comes down to pricing, spreads, and personal preference.

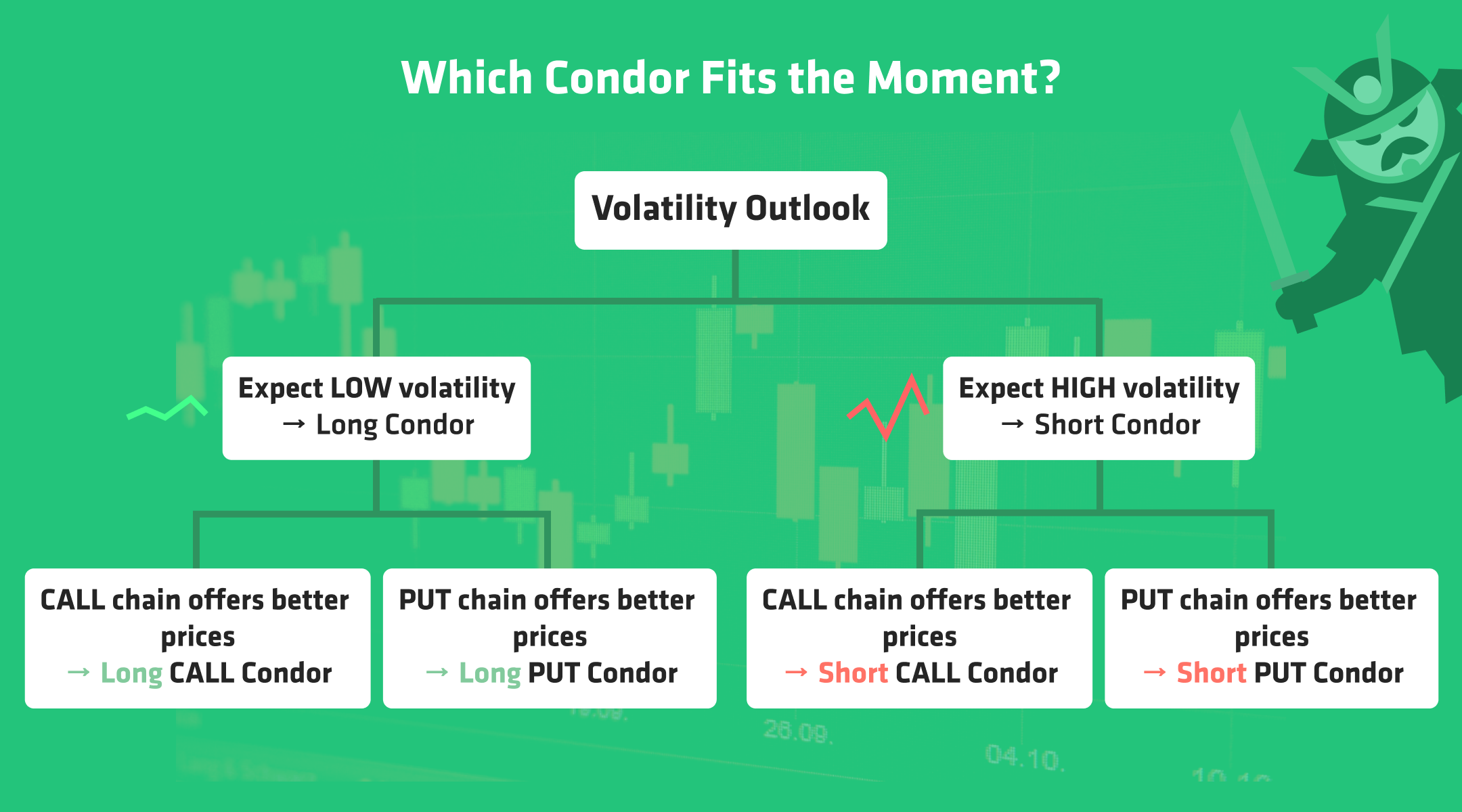

Additional Aspects to Consider about the Condor Spreads

Before leaving you, we want to address a few additional points that it is worth considering before trading a condor spread (either long or short). First of all, check out our infographic about choosing the right condor strategy for the right moment:

Also, consider the following points:

- The condor strategy is usually easier to build far out-of-the-money than an iron condor. This is because OTM calls or puts tend to have tighter bid-ask spreads than deep ITM puts.

- All condor options setups (calls, puts, or iron) have the same risk-reward profile. The difference is in how you get there.

- Choose the structure that offers better liquidity and fills. Sometimes the condor option strategy is just more practical.

- A secondary use: if you already have a call spread open, you can later add a second, reversed one to turn it into a call condor, useful if the stock keeps drifting.

In short, it’s less about theory and more about what works best in your current condor trading setup.

Read More

Read about the custom option strategy screener feature, which lets you scan the market for custom strategies such as condor spreads and many more

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.