Reviewed by Leav Graves

Delta is one of the first things you run into when you start trading options, and that’s not surprising. Delta in options tells you how much a contract price should move when the underlying stock moves. But the delta options greek goes beyond simple price changes. How does delta work differently for calls and puts? Can it help you estimate the probability of a trade working out? What happens to delta in options when you're selling instead of buying? And how does it interact with the other greeks? This article covers all of it.

KEY TAKEAWAYS

- The delta in options tells you how much its price is expected to change for every $1 move in the underlying stock.

- Delta ranges from 0 to 1.00 when you buy calls and 0 to -1.00 when you buy puts. The closer delta is to 1 or -1, the more the option moves like the stock itself.

- Beyond price sensitivity, the delta options greek can also be used to estimate the probability of an option expiring in the money.

Delta Options - What Is It?

So what is delta in options, really? At its core, delta measures how much an option's price is expected to move for every $1 change in the underlying stock. If a call option has a delta of 0.60, you can expect its price to rise by about $0.60 when the stock goes up $1. It's the most direct link between the option and the stock it's based on.

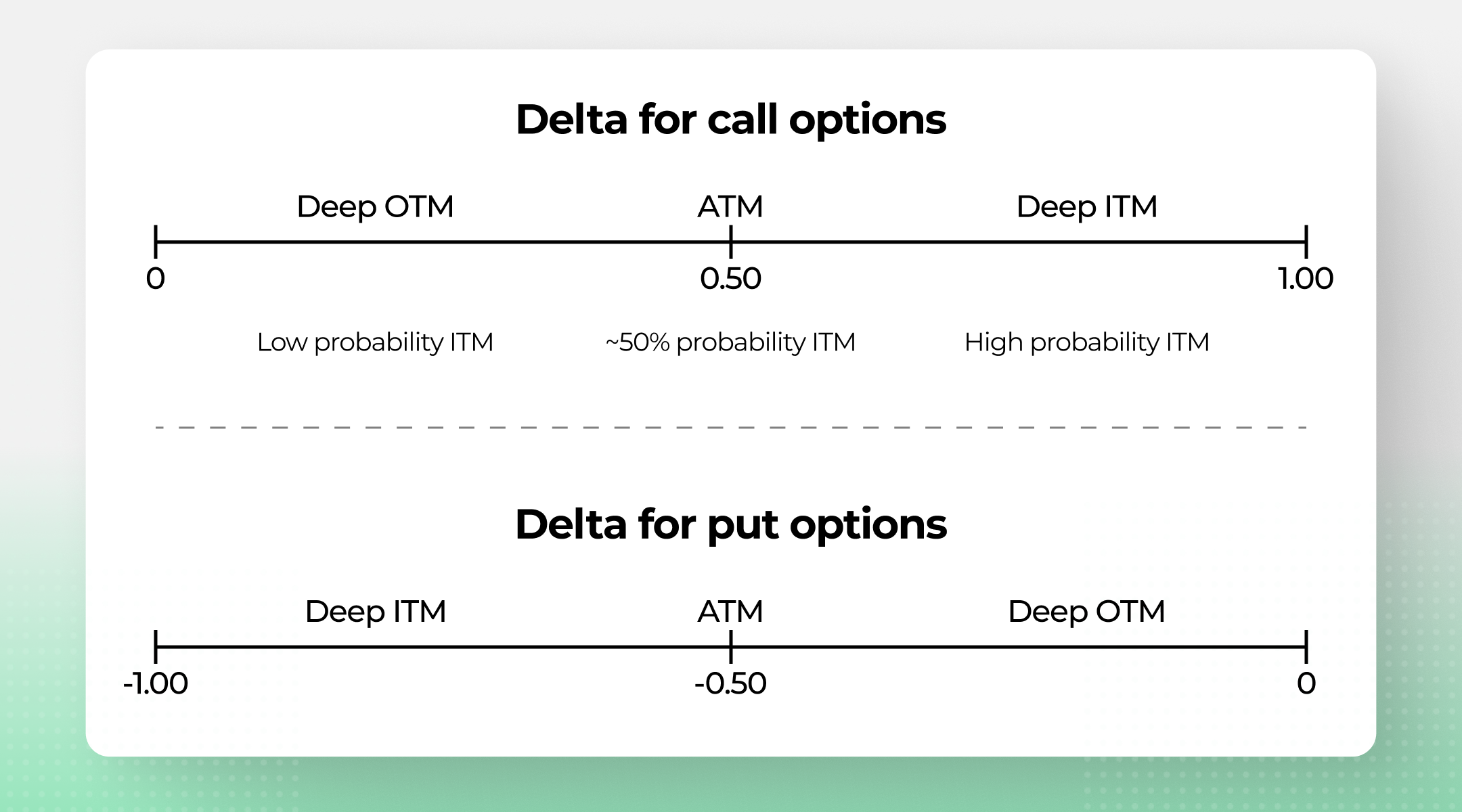

Call options always carry a positive delta, ranging from 0 to 1.00. Put options carry a negative delta, ranging from 0 to -1.00. An at-the-money (ATM) option typically sits near 0.50 for calls or -0.50 for puts. Deep in-the-money options push closer to 1.00 or -1.00, while far out-of-the-money options hover near zero.

The diagram below shows how the delta options greek range maps to moneyness and probability for both calls and puts:

But there's more to delta options than price sensitivity alone. Delta also works as a share equivalency measure. A call with a delta of 0.50 behaves roughly like owning 50 shares of the underlying stock. This makes it useful as a hedge ratio - if you own 100 shares and want to hedge with puts, delta tells you how many contracts you need.

The delta options greek also reflects directional bias. A positive delta position is bullish (you profit when the stock rises), while a negative delta position is bearish (you profit when the stock drops). This is why delta options values are often the first number traders check when evaluating a trade.

As a side note, consider that, in our screener for the options market, we are showing delta in 100s to make it easier to read (so a delta of 0.50 will actually be 50, and so on).

Where Delta Fits Among the Options Greeks

Delta is one of five options greeks that traders use to measure risk. Here's a quick overview of what each one tracks:

Greek | What It Measures |

Delta | Price change per $1 move in the stock |

Gamma | Rate of change of the delta options greek |

Theta | Daily time decay - how much value the option loses each day |

Vega | Sensitivity to changes in implied volatility |

Rho | Sensitivity to changes in interest rates |

Of all the greeks, delta is typically the first one traders look at because it directly links the option's price to the stock's price. If you only learn one greek, start with delta options. Understanding how delta works gives you the foundation to make sense of gamma, theta, vega, and rho.

Delta Options - A Practical Example

Numbers make this easier. Here are two quick examples that answer the “what does delta mean in options?” question when real money is on the line.

Call Example

You buy a call option priced at $3.00 with a delta of 0.50. The stock moves from $50 to $51. Your option should increase by about $0.50 (delta x $1 stock move), all other things being equal. This will bring the new price to roughly $3.50.

Put Example

You hold a put option priced at $5.00 with a delta of -0.30. The stock rises $1, so your put drops to about $4.70 (again, all other things being equal). If the stock falls $1 instead, the put rises to about $5.30.

Keep in mind that delta is a theoretical estimate. In practice, your actual P&L will also be shaped by gamma (delta is always shifting), theta (time decay chips away at value), and vega (volatility changes affect pricing). Delta options pricing gives you a starting point, not a guarantee.

Use Option Samurai's screener to filter options by delta range, moneyness, and expiration - so you find setups that match your directional view without digging through chains manually.

Options Delta Explained for Calls and Puts

With options delta explained in simple terms, here's how this greek behaves depending on whether the option is in or out of the money.

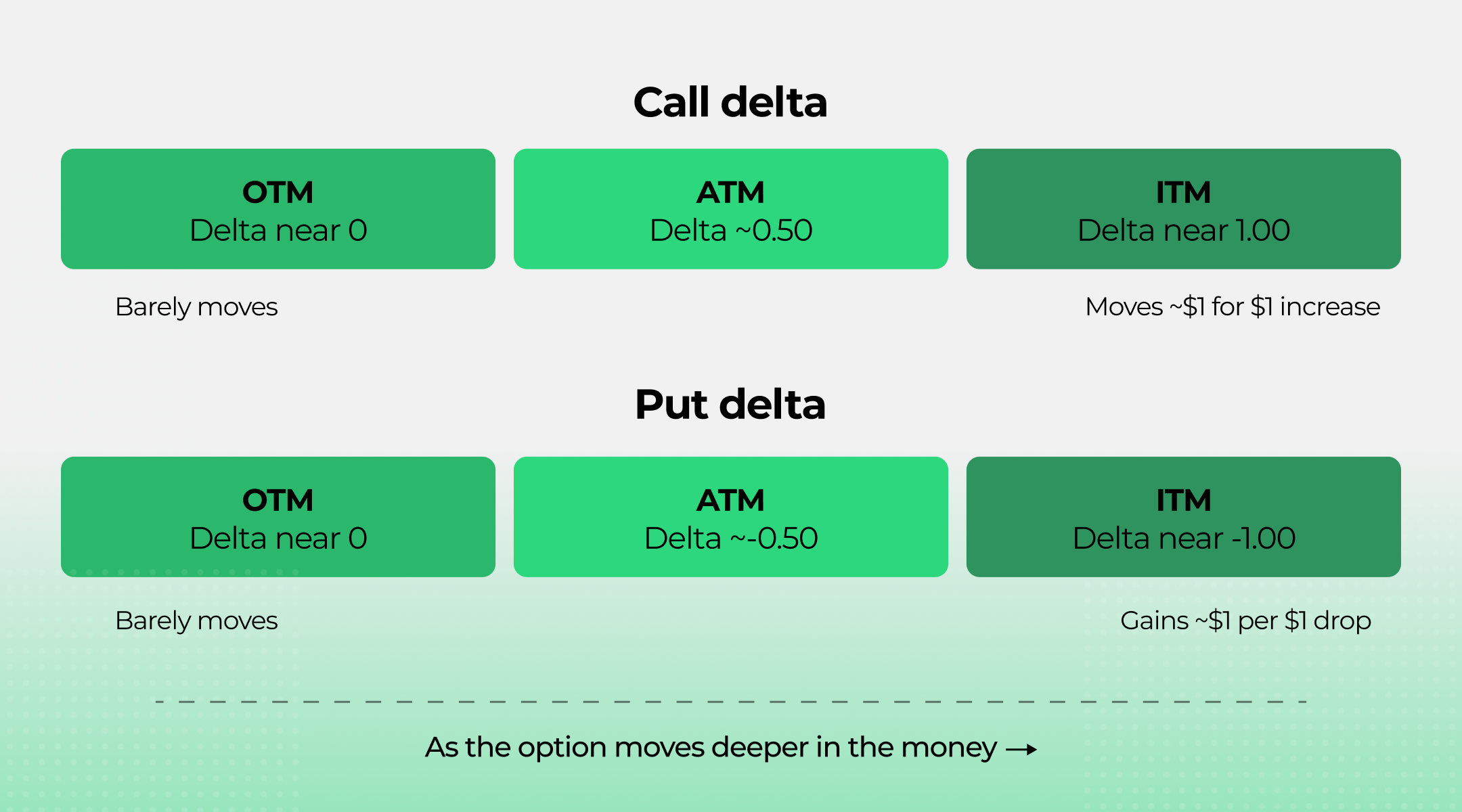

Let’s start from this simple infographic:

Call Delta

As a call option moves deeper in the money (ITM), its delta increases toward 1.00. A deep ITM call with a delta near 1.00 moves almost dollar-for-dollar with the stock. As the call moves further out of the money (OTM), delta drops toward 0 - meaning the option barely reacts to small stock moves.

Put Delta

Put delta works in the opposite direction. A deep ITM put has a delta approaching -1.00, so it gains close to $1 for every $1 the stock drops. An OTM put has a delta near 0, and it barely moves when the stock changes price.

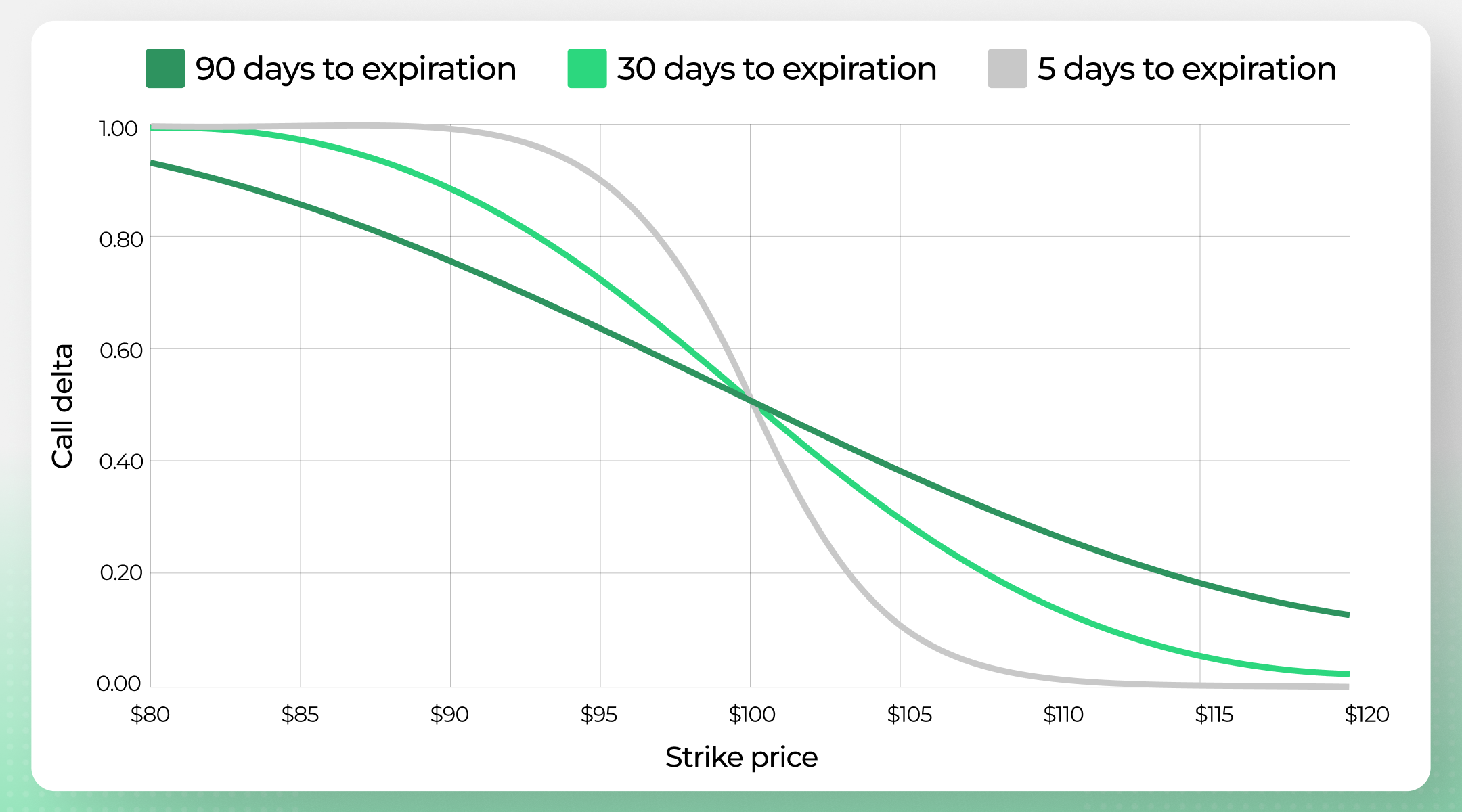

Delta Near Expiration

As expiration approaches, the delta options greek becomes more extreme, and this is very easy to see when you think of a call option on a stock trading at $100:

ITM options see their deltas sharpen toward 1.00 or -1.00, while OTM deltas collapse toward 0. This is sometimes called the "delta cliff" because the shift can happen fast in the final days before expiration.

One important thing to remember: delta doesn't stay fixed. Gamma is the rate at which delta itself changes. High gamma means delta can shift quickly, especially for ATM options close to expiration. This is why a delta options position can feel stable one week and volatile the next.

What Does Delta Mean in Options for Long vs Short Positions?

The delta options greek works the same way mechanically whether you're buying or selling contracts. The difference is how it hits your P&L. Here's how delta in options plays out for each position type:

- Long call: The stock rises $1, your call gains the delta amount in value. If delta is 0.60, you make about $0.60 per share. Good for the buyer.

- Short call: Same move, same delta, but now you're on the other side. The option gains value, which means the seller loses that amount.

- Long put: You profit when the stock drops. Delta tells you how much the put gains per $1 decline. A delta of -0.40 means the put rises about $0.40 when the stock falls $1.

- Short put: The seller loses as the put gains value on a stock decline. The same -0.40 delta that helps the buyer hurts the seller by the same amount.

The key point is straightforward: delta tells you the size of the move, but your position (long or short) determines whether that move helps or hurts you. Two traders can hold the exact same delta options contract and have opposite outcomes depending on which side of the trade they're on. With options delta explained this way, you can see why knowing your position's net delta matters before you enter any trade.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.