Reviewed by Leav Graves

If delta tells you how much an option’s price moves when the stock moves, what tells you how fast delta itself changes? That’s where gamma options come in. This article covers what gamma means in options, how it behaves at different strikes and expirations, and why it matters when you trade gamma options.

KEY TAKEAWAYS

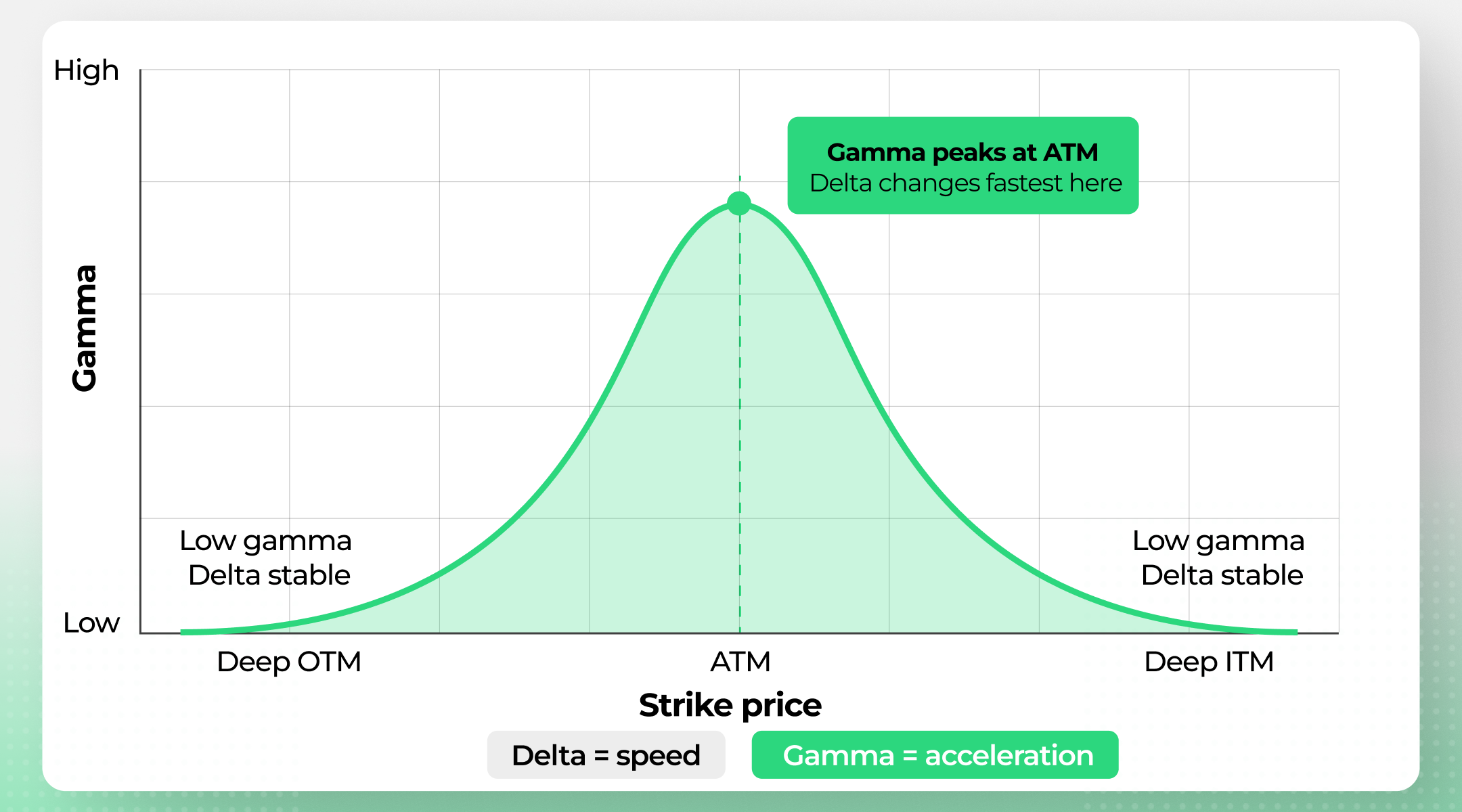

- The gamma in options tells you how fast its delta changes when the underlying stock moves by $1. It ranges between 0 and 1.

- At-the-money options have the highest gamma because their delta is the most sensitive to stock price changes. Deep ITM and deep OTM options have low gamma.

- Gamma increases as expiration approaches for near-the-money options, which means delta can swing sharply in the final days before expiry.

Gamma Options - What Is It?

So what is gamma in options, exactly? Gamma measures the rate of change of delta for every $1 move in the underlying stock. If delta tells you how much an option’s price will change when the stock moves, gamma tells you how much delta itself will shift after that move.

Gamma ranges between 0 and 1. Where it falls depends mostly on how close the option’s strike price is to the current stock price:

- At-the-money (ATM) options have the highest gamma. A small price move can push them in or out of the money, so delta reacts strongly.

- Deep in-the-money (ITM) options already have delta close to 1 (calls) or -1 (puts). There isn’t much room left for delta to change, so gamma is low.

- Deep out-of-the-money (OTM) options have delta near 0. The stock would need a big move to make delta budge, so gamma stays low here too.

One more thing worth noting: gamma is positive for long positions and negative for short positions, regardless of whether you’re trading calls or puts. This is a key property of gamma options that becomes important when we look at how your P&L behaves depending on which side of the trade you’re on.

Options Gamma Explained: The Stability of Delta

Here’s another way to think about gamma options: they tell you how stable or unstable your delta is.

- High gamma = delta is unstable. It can shift fast with a small stock move.

- Low gamma = delta is steady. It won’t change much unless the stock makes a big move.

This options greeks analysis matters when you use delta as a rough estimate of the probability that an option expires in the money. If gamma is high, that probability estimate can flip quickly, which means your position’s risk profile is changing fast.

The biggest gamma spikes happen near expiration for at-the-money options. As expiration gets closer, extrinsic value drains out, and the option starts pricing almost entirely on intrinsic value. This makes delta behave in a more binary way - it’s heading toward either 0 or 1 (or -1 for puts). That transition can happen fast, and gamma is what captures that speed.

So when you see options gamma explained in terms of “risk near expiration,” this is what it means. An ATM option a few days from expiry can see its delta swing from 0.50 to 0.90 with a small stock move. That’s gamma options in action.

Gamma Options - A Practical Example

Let’s walk through what gamma means in options with a worked example. Say you buy a call option with these starting values:

• Option price: $1.00

• Delta: 0.40

• Gamma: 0.10

Stock Rises $1

Delta is 0.40, so the option gains $0.40. New option price: $1.40. Gamma adds 0.10 to the delta greek, which will now be equal to 0.50.

Stock Rises Another $1

Delta is now 0.50, so the option gains $0.50. New option price: $1.90. Gamma adds another 0.10, making the new delta equal to 0.60.

Notice how the gains accelerate. The first dollar move earned you $0.40, the second earned $0.50. Each dollar move in the stock adds more to your option’s value because gamma keeps pushing delta higher.

Now flip it - what if the stock drops $1 instead? Delta is 0.40, so you lose $0.40. New price: $0.60. Gamma subtracts 0.10 from delta, making new delta 0.30. If the stock drops another $1, you only lose $0.30. The losses decelerate, which is one benefit of holding positive gamma options positions.

Keep in mind that gamma itself changes as the stock moves, so these numbers are approximations. But they show how gamma options work in practice.

What Does Gamma Mean in Options for Long Positions?

For long options - whether calls or puts - gamma is your friend when the stock moves in your favor. Higher gamma means delta increases faster as the stock moves your way, so your profits pick up speed.

But it cuts both ways. If the stock moves against you, delta also shifts faster in the wrong direction, amplifying losses in the early part of the move.

Think of it this way: a long call with delta 0.40 and gamma 0.10 will see its delta rise to 0.50 after a $1 stock increase. The next $1 move has even more impact. This acceleration is what makes gamma options attractive for directional traders expecting a big move, but you need it to happen before time decay chips away at your position.

What Does Gamma Mean in Options for Short Positions?

If you sell options, gamma works against you. Short positions carry negative gamma, which means that when the stock moves against your position, delta accelerates in the wrong direction and your losses grow faster with each dollar.

This is especially dangerous for uncovered (naked) short options. A short call on a stock that starts rallying will see delta climb quickly, and each additional dollar of stock movement creates a bigger loss than the one before.

The risk is highest near expiration, when gamma peaks for at-the-money options. This is why experienced sellers pay close attention to gamma in options as expiry approaches. Managing or closing short gamma options positions before the final days can help prevent drastic P&L swings.

Option Samurai's screener lets you sort and filter by gamma alongside delta, theta, and vega - so you can spot high-gamma setups or avoid them, depending on your strategy.

Other Factors to Consider with Gamma

At expiration, gamma drops to zero. By that point, delta has settled at either 0 (the option expires worthless) or 1/-1 (the option is in the money and gets exercised). There’s no more uncertainty for gamma to measure.

There’s also a direct relationship between gamma and theta. As gamma increases near expiration, theta - the rate of time decay - also increases. High gamma options are expensive to hold because time decay accelerates alongside delta sensitivity. You get more explosive delta moves, but you pay for it through faster erosion of time value. Having options gamma explained in this way shows why many traders weigh gamma against theta before entering a position.

If you want to screen for gamma options or other greeks, Option Samurai lets you filter by gamma, delta, theta, and more to find positions that match your risk preference and trading style.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.