Double Diagonal Spread - An Advanced Time Decay Strategy Explained

Published on August 20, 2025(Last updated on October 23, 2025)

Table of Contents

- Key Takeaways

- What Is a Double Diagonal Spread?

- How the Double Diagonal Option Strategy Works

- Profit, Risk, and Breakeven Points

- Real Trade Example of a Double Diagonal Calendar Spread

- Greeks and Sensitivity to Volatility

- Managing a Double Diagonal Spread

- When to Use a Double Diagonal Spread

- Risks and Early Assignment Considerations

Reviewed by Leav Graves

Table of Contents

- Key Takeaways

- What Is a Double Diagonal Spread?

- How the Double Diagonal Option Strategy Works

- Profit, Risk, and Breakeven Points

- Real Trade Example of a Double Diagonal Calendar Spread

- Greeks and Sensitivity to Volatility

- Managing a Double Diagonal Spread

- When to Use a Double Diagonal Spread

- Risks and Early Assignment Considerations

The double diagonal spread is a lesser-known options strategy that combines time decay and defined risk. Why do some traders prefer it over a standard iron condor? What makes the double diagonal option strategy so flexible - and when does a double diagonal calendar spread actually make sense? Let’s break it down.

KEY TAKEAWAYS

- A double diagonal spread is a neutral strategy built by combining two diagonal spreads - one with calls, one with puts - with different expiration dates.

- It profits from time decay and limited price movement, with defined risk and potential for rolling into an iron condor.

- Works best when the underlying stays within the short strike range until expiration.

What Is a Double Diagonal Spread?

A double diagonal spread is a neutral options strategy made by combining two separate diagonal spreads - one on the call side, one on the put side. Both sides use different expiration dates and different strike prices, but the goal is the same: profit from time decay while keeping risk limited.

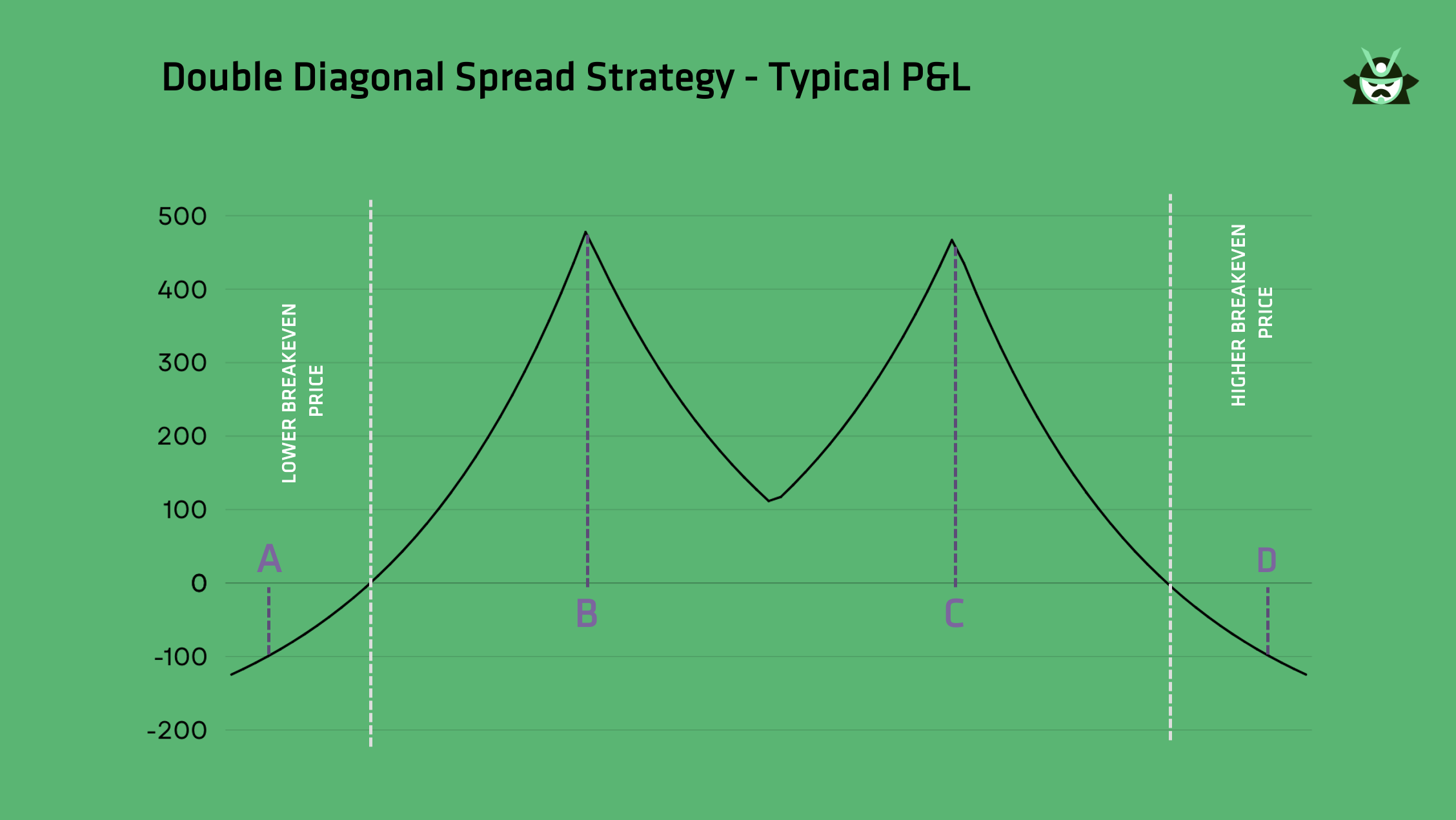

Here’s the typical P&L chart of a double diagonal spread (it’s quite similar to the one of a regular diagonal spread, as you may find on our screener for the options market):

You can read the chart as follows:

- Buy an out-of-the-money put, strike price A (with a later expiration)

- Sell a closer out-of-the-money put, strike price B (with an earlier expiration)

- Sell an out-of-the-money call, strike price C (with an earlier expiration)

- Buy a further out-of-the-money call, strike price D (with a later expiration)

The idea is that you will normally have the current stock price between II and III.

This creates a structure where you’re long both a call and a put, and short both a call and a put, with all the options having different strike prices. The trade is usually opened for a net debit, and the max risk is the amount you pay upfront. To be clear: you should aim to open the double diagonal spread for a net credit. However, that might not be possible since the front-month options you're selling often have less time value than the back-month options you're buying. Therefore, this article will focus on the common net debit case.

Think of it like two diagonals glued together:

- The call side is a diagonal call spread

- The put side is a diagonal put spread

The strategy does best when the stock stays between the short strike prices - usually the range of the short strangle - until expiration.

This setup is also called a double diagonal calendar spread, and it’s popular with traders looking to squeeze value out of time decay while keeping a tight grip on risk.

How the Double Diagonal Option Strategy Works

This double diagonal spread is built using four options: two longer-term and two shorter-term, all placed at different strikes. You’re combining a diagonal call spread and a diagonal put spread in a single position.

This structure works best when the underlying price stays between the short strikes until the near-term expiration. If that happens, both short options expire worthless, and you keep the premium. Meanwhile, the long options still hold value because they expire later.

Because the short options lose time value faster, the double diagonal option strategy benefits from time decay. That’s where most of the edge comes from.

- It’s usually opened for a net debit

- The stock should start somewhere between the short strikes

- The position can have a slight bullish or bearish tilt depending on where you place the shorts

Some traders roll the short legs forward after expiration and sell them again. When all the options end up with the same expiration, the double diagonal calendar spread can turn into a hybrid version of the iron condor strategy, with extra time decay already captured.

Profit, Risk, and Breakeven Points

The double diagonal spread offers defined max risk and limited max reward, making it a favorite for traders who want tight control over outcomes.

Your max profit happens when the stock lands exactly at the strike of one of the short options - either the short call or short put - on the front-month expiration. In this case, both short legs expire worthless, and the longer-dated options still retain time value. That time value becomes your max reward.

In general, we’d say you should not expect a home run. The double diagonal option strategy is built to win small and win often. It’s usually a net debit trade, which means you pay to enter it. That entry cost is your max loss. If the stock makes a big move and volatility drops, your long options lose value fast - and you can end up with nothing.

Real Trade Example of a Double Diagonal Calendar Spread

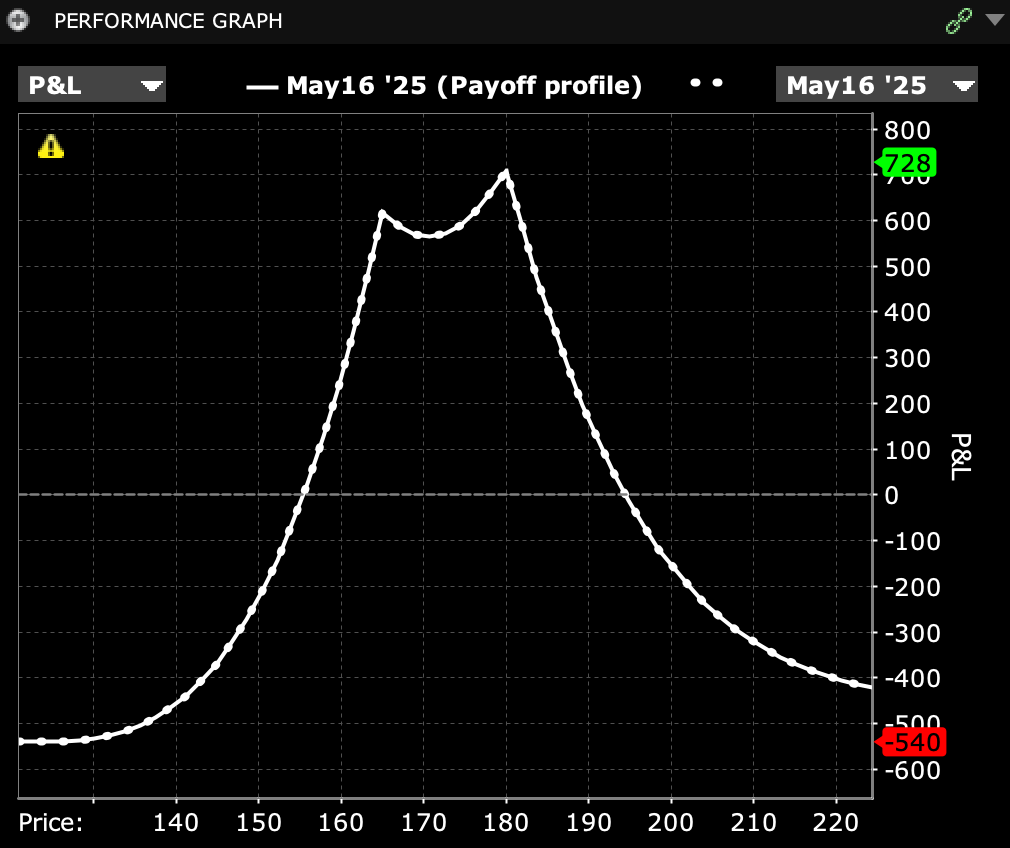

AMZN is trading at $172.61. Here’s how a trader might build a double diagonal spread around that price:

- Buy 1 June 20, 2025 $140 Put

- Sell 1 May 16, 2025 $165 Put

- Sell 1 May 16, 2025 $180 Call

- Buy 1 June 20, 2025 $210 Call

This creates a double diagonal calendar spread with the short legs closer to expiration (May) and the long legs one month further out (June). The short options are placed on either side of the current price to form a neutral zone.

Your double diagonal spread P&L chart would look like this:

Based on this setup:

- You risk $540 on the left-hand side

- You risk $459 on the right-hand side

These represent the max loss on each half of the position if AMZN moves far past the short strikes.

When the May options expire, you can clearly see the risk/reward profile: two peaks centered around $165 and $180. Those are your max profit zones. If AMZN ends up near either strike on expiration day, the short options lose most of their value, while the long ones still hold premium.

The estimated max reward at peak is close to $700, depending on volatility and pricing of the remaining long legs.

Greeks and Sensitivity to Volatility

The double diagonal spread starts off with a delta close to zero. That’s because the position is neutral - long and short legs cancel each other out. But as time passes or price moves, delta shifts. If AMZN drifts near one of the short strikes, the position picks up direction.

Since we are buying and selling options, we also need to take into account the net effect of implied volatility on the trade. The double diagonal option strategy is long vega. That means it benefits when implied volatility rises (vegas tend to decrease as we approach expiration). A volatility spike boosts the value of the longer-dated options, giving the trade more breathing room. If volatility drops, the position can lose value - even if price stays in range.

Time decay works in your favor here. The double diagonal calendar spread is positive theta as long as the stock stays between the short strikes.

Quick recap:

- Delta: starts neutral, becomes directional over time

- Vega: positive - rising volatility helps

- Theta: positive in range - profits from time decay

Once price breaks out, both vega and theta advantages drop off fast.

Managing a Double Diagonal Spread

Managing a double diagonal spread means staying ahead of the short legs. As expiration nears, the risk of one side moving in-the-money increases. This is where gamma risk kicks in - price changes accelerate and can eat into your gains fast.

To reduce this risk, many traders roll the short options 5 days before expiration. This lets you extend the trade without riding into the weekend with unwanted exposure.

You can roll by:

- Closing the short put and call

- Opening new ones with the same strikes, but later expiration

This turns your double diagonal calendar spread into a new one with more time to work.

A few tips:

- Always use limit orders to avoid slippage

- Monitor short strikes daily in the final week

- Don’t wait until the last minute to manage in-the-money legs

A little attention goes a long way with this double diagonal option strategy.

When to Use a Double Diagonal Spread

The double diagonal spread works best in low-volatility or sideways markets where price stalls between the short strikes. It also fits well before earnings or macro events - when implied volatility is expected to rise. Just be careful: once the event hits, IV crush can hurt your long legs.

This double diagonal calendar spread is a solid choice when:

- The underlying is range-bound

- You expect implied volatility to rise

- You're trading indexes or ETFs (which move slower and spike less)

To better understand how each half of this setup works, you can explore our complete guide on the diagonal spread, where we explain the single-leg mechanics that form the base of the double diagonal strategy. And if you want to compare this neutral approach with a directional, volatility-sensitive structure, you can also review the reverse iron butterfly to see how it behaves in fast-moving markets.

Risks and Early Assignment Considerations

Short options in a double diagonal spread carry early assignment risk, especially around ex-dividend dates. If a short call or put moves in-the-money, you could end up with unwanted stock - long or short. That means margin impact, slippage, and extra trades to unwind.

The best move? Monitor short legs closely and close them before expiration if needed.

- Assignment = short stock (from short call) or long stock (from short put)

- Intraday swings can hurt, even with defined max risk

- Best to exit early if the stock is near your short strikes

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.