Intrinsic vs Extrinsic Value in Options - Understanding Value Beyond the Strike Price

Published on March 30, 2026 | 7 min readTable of Contents

Reviewed by Leav Graves

Table of Contents

When you buy an option, do you know what you are paying for? This article looks at intrinsic and extrinsic value in options, including intrinsic vs extrinsic value in options, the extrinsic value definition, and the intrinsic value of options. You will see how extrinsic vs intrinsic value affects price, risk, and timing.

KEY TAKEAWAYS

- The intrinsic and extrinsic values in options are the two components that make up an option’s premium, intrinsic reflects real exercise value, extrinsic reflects future potential

- Intrinsic value of options depends only on the relationship between strike price and underlying price, not time or volatility

- Extrinsic value changes constantly due to time decay, volatility, interest rates, and dividends, and usually disappears at expiration

Extrinsic vs Intrinsic Values Explained in Simple Terms

Intrinsic and extrinsic value in options answer a simple question, what part of the option price is real right now, and what part is based on what might happen next.

The intrinsic value of options is the “tangible part” you see in the premium. Why tangible? Because it comes from the relationship between the strike price and the current price of the underlying. In other words: if exercising the option right now would give you a profit, that amount is the intrinsic value. It is immediate, concrete, and does not depend on time or expectations.

Extrinsic value is different. The definition of extrinsic value is everything in the option price that is not intrinsic. This part exists because the future is uncertain. When there’s time left to the expiration, prices can move, and outcomes are not locked in yet. intrinsic vs extrinsic value in options is really a comparison between what is already there and what could still happen.

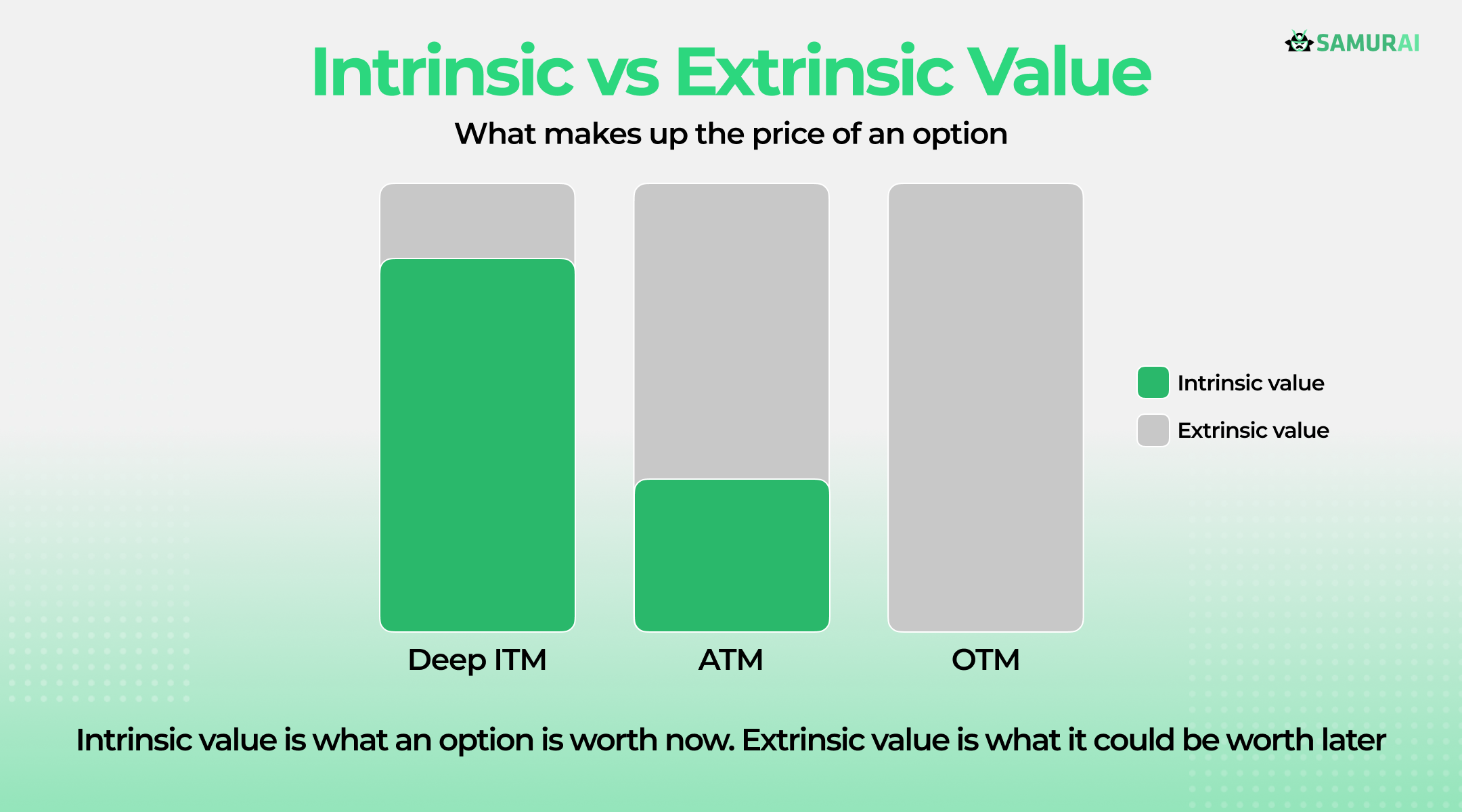

This is a simple infographic you can keep in mind when you think about this topic:

In simple terms:

- The intrinsic value reflects real exercise value today

- The extrinsic value reflects probability, time, and uncertainty

- Both combine to form the full option premium

The idea is that intrinsic and extrinsic value in options exist at the same time. An in-the-money option has intrinsic value, but it also carries extrinsic value as long as expiration has not arrived. As time passes, that extra portion fades, leaving only intrinsic value, or nothing at all. Understanding extrinsic vs intrinsic value helps you see what you are paying for and what you are risking.

Intrinsic Value of Options and How It Is Calculated

Intrinsic value of options is the part of the option price that comes from real, immediate value. It answers one question, if you exercised the option right now, would it be worth something? If the answer is yes, that amount is intrinsic value. If not, intrinsic value is zero. This is the most concrete part of intrinsic and extrinsic value in options.

Options fall into three simple categories based on intrinsic value:

- In-the-money, exercising the option creates value

- At-the-money, the strike and price are about the same

- Out-of-the-money, exercising the option makes no sense

This is how intrinsic value works in options:

Option type | Market price vs strike | Intrinsic value |

Call | Price above strike | Price minus strike |

Call | Price at or below strike | 0 |

Put | Price below strike | Strike minus price |

Put | Price at or above strike | 0 |

For call options, intrinsic value comes from buying below the market price. If the stock trades above the strike, the call has intrinsic value equal to that difference. If the stock is at or below the strike, intrinsic value is zero. You can see this clearly in a call option payoff diagram.

For put options, intrinsic value works in reverse. If the stock trades below the strike, the put has intrinsic value equal to that gap. If the stock is at or above the strike, intrinsic value is zero.

This is where intrinsic vs extrinsic value in options becomes useful. The intrinsic value of options depends only on price and strike. Time, volatility, and expectations do not matter here. That is why intrinsic value never goes below zero, you can always choose not to exercise.

Everything else in the option price falls under the extrinsic value definition. Intrinsic vs extrinsic value in options is the split between real exercise value and future possibility. Understanding intrinsic and extrinsic value in options helps you see whether you are paying for value that already exists or for potential that may never show up.

And for the record, intrinsic and extrinsic values are two available columns in our screener for the options market. This means you can play around with them as you please to evaluate every single strategy.

Definition of Extrinsic Value and What It Represents

Extrinsic value is the part of an option’s price that comes from possibility, not from real exercise value. The definition of extrinsic value, in practical trading terms, is simple. It is the amount you pay for time, uncertainty, and the chance that price moves in your favor before expiration. This is the second half of intrinsic and extrinsic value in options.

This explains why out-of-the-money options can still be expensive. Even with zero intrinsic value of options today, there is still time left. Price can move, volatility can expand, and probabilities are not settled yet. That future potential is what traders are paying for.

Extrinsic vs intrinsic value becomes clear when you think in terms of odds. Intrinsic value reflects what you would gain right now. Extrinsic value reflects the probability of finishing in-the-money later. The higher that probability, the more extrinsic value an option carries. When the probability drops, extrinsic value shrinks.

Extrinsic value is often called time value because time is the main driver. More time means more chances for price to move. Less time means fewer chances.

In simple terms:

- Extrinsic value exists because the future is uncertain

- Out-of-the-money options are priced on probability, not payoff

- Time passing reduces extrinsic value, even if price does not move

As expiration approaches, uncertainty fades. That is why intrinsic and extrinsic value in options shift over time. By the final day, extrinsic vs intrinsic value resolves into one outcome, either intrinsic value remains, or the option expires worthless.

Extrinsic Value Definition in Practice (Time Decay and Volatility)

Extrinsic value changes mainly because of time and volatility. The extrinsic value definition in practice comes down to this, the more time and uncertainty an option has, the more it is worth beyond intrinsic value of options. This is a key part of intrinsic and extrinsic value in options that traders feel every day.

Time remaining until expiration matters because it represents opportunity. With months left, price has many chances to move. With days left, those chances shrink fast. This is why time decay speeds up as expiration gets closer. Early on, extrinsic value melts slowly. Near expiration, it drops faster because uncertainty resolves quickly.

At-the-money options usually carry the most extrinsic value. They sit right where price could move either way, so the probability of finishing in-the-money is highest. Deep in-the-money options are mostly intrinsic. Far out-of-the-money options have low odds, so extrinsic value is limited.

Implied volatility plays a similar role. When volatility rises, expected price movement increases, so extrinsic value expands. When volatility falls, that future potential is priced lower. This is where intrinsic vs extrinsic value in options becomes visible even if price does not move.

To clarify how extrinsic value works, we’ve listed a few common cases in the table below:

Factor | Effect on extrinsic value |

More time to expiration | Higher extrinsic value |

Less time to expiration | Faster time decay |

At-the-money strike | Highest extrinsic value |

Higher implied volatility | Expands extrinsic value |

Lower implied volatility | Shrinks extrinsic value |

Intrinsic and Extrinsic Values in options Using Real Examples

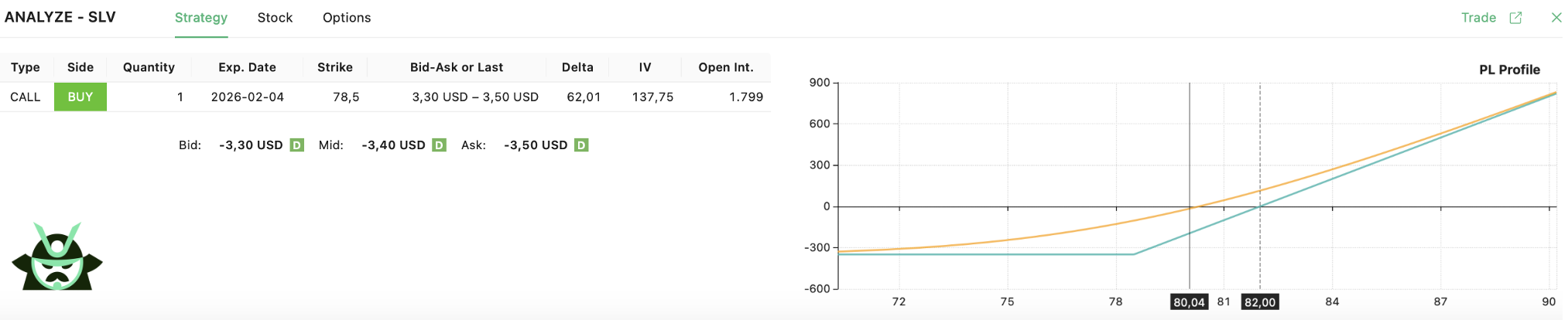

The examples below use SLV options captured a few seconds apart, with the price sitting around 80. The timing is not identical, but close enough to show how intrinsic and extrinsic value behave in real trades.

In the first image, the call option is in-the-money:

The strike ($78.5) sits below the current price ($80.04), so exercising the option would create immediate value. That payoff comes entirely from the intrinsic value of options ($80.04 - $78.5 = $1.54, while the rest of the option premium corresponds to the extrinsic value).

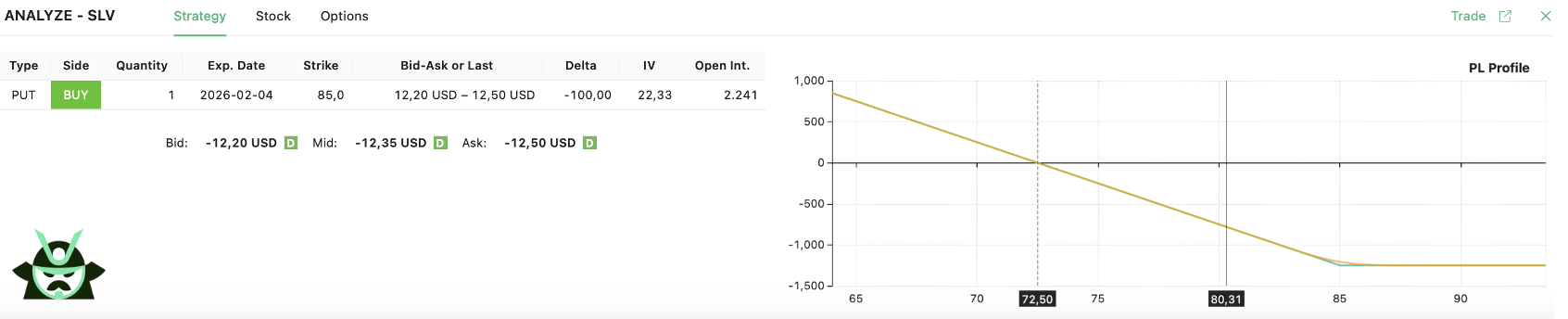

The second image shows a long put that is also in-the-money:

Here, the strike ($85) is above the current price ($80.31). The value comes from the right to sell higher than the market. A part of the option price is intrinsic value ($85 - $80.31 = 4.69), with intrinsic vs extrinsic value in options clearly tilted toward extrinsic (notice the price of the option is above $12, which means that we have over $7 in extrinsic value).

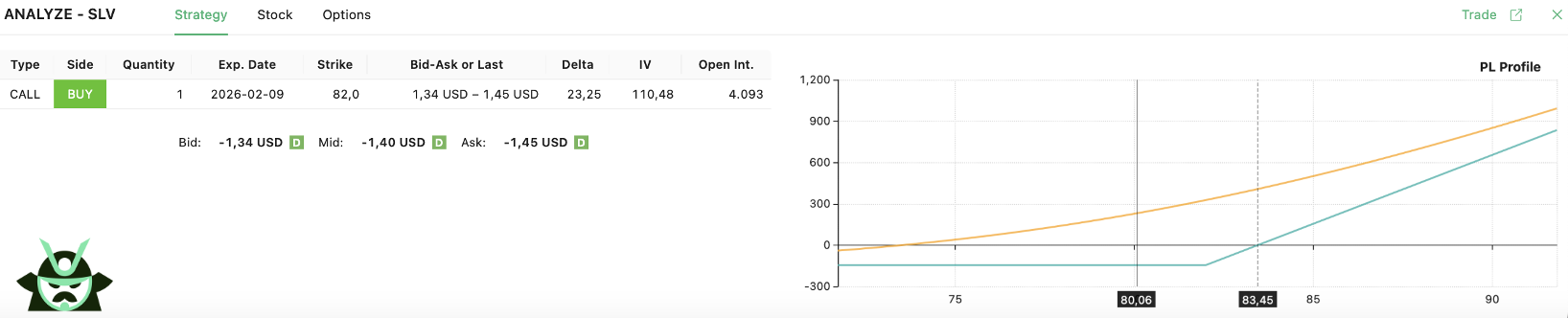

The third image shows a call option that is out-of-the-money:

There is no intrinsic value of options at this price level (you would not exercise a call at $82 when you can simply purchase SLV on the market at $80.06). Still, the option is not worthless. The extrinsic value definition explains why, time remains, and price could move above the strike before expiration. So, 100% of the option price corresponds to the extrinsic value of the contract.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.