Options Portfolio Management: How to Build and Balance Positions

Published on January 12, 2026 | 11 min readTable of Contents

- Key Takeaways

- Understanding the Basics of Options Portfolio Management

- Core Elements of an Options Portfolio

- Options Portfolio Management Principles

- Option Management in Practice

- Building an Options Portfolio Step by Step

- Example of a Balanced Options Portfolio

- Monitoring and Adjusting an Options Portfolio

- Common Mistakes in Options Portfolio Management

Reviewed by Leav Graves

Table of Contents

- Key Takeaways

- Understanding the Basics of Options Portfolio Management

- Core Elements of an Options Portfolio

- Options Portfolio Management Principles

- Option Management in Practice

- Building an Options Portfolio Step by Step

- Example of a Balanced Options Portfolio

- Monitoring and Adjusting an Options Portfolio

- Common Mistakes in Options Portfolio Management

Options portfolio management helps traders keep risk under control while looking for returns. But how do you build an options portfolio that stays balanced over time? What role does option management play in daily decisions, and how can options risk management with Greeks guide smarter position sizing and adjustments?

KEY TAKEAWAYS

- Options portfolio management is the practice of building, balancing, and adjusting option positions to control risk and improve returns

- A well-structured options portfolio should balance strategies, sectors, and expirations to avoid concentration and keep risk exposure within limits

- Options portfolio management relies on monitoring Greeks, position sizing, and timely adjustments, ensuring consistency between trading activity and financial objectives.

Understanding the Basics of Options Portfolio Management

Options portfolio management means building, balancing, and adjusting option positions in a way that keeps risk under control while leaving room for returns. Instead of treating each trade as a stand-alone bet, the focus is on how all positions work together inside one options portfolio.

This is different from stock-only investing because options carry unique features: limited lifespan, time decay, and sensitivity to volatility. A stock portfolio can be left alone for years, while an options portfolio requires active option management to avoid unexpected losses and to take advantage of short-term opportunities.

The value of options portfolio management comes from matching strategies with personal financial goals. A trader looking for steady income may use covered calls or credit spreads. Someone focused on downside protection may prefer protective puts. The important point is that every trade should serve the bigger picture, not just look good in isolation.

When thinking about alignment, ask simple questions:

- Does this position fit my income or protection goals?

- How does it affect my overall exposure to market moves?

- What will happen if volatility rises or falls?

Effective options portfolio management starts here. Monitoring Greeks such as Delta, Theta, and Vega helps measure whether the portfolio is tilted too far in one direction or exposed to rapid changes. Over time, these checks allow traders to adjust sizing, expiration dates, and strike selection so that the portfolio stays balanced.

In short, options portfolio management is not about one winning trade, but about creating a mix of trades that work together to support long-term objectives.

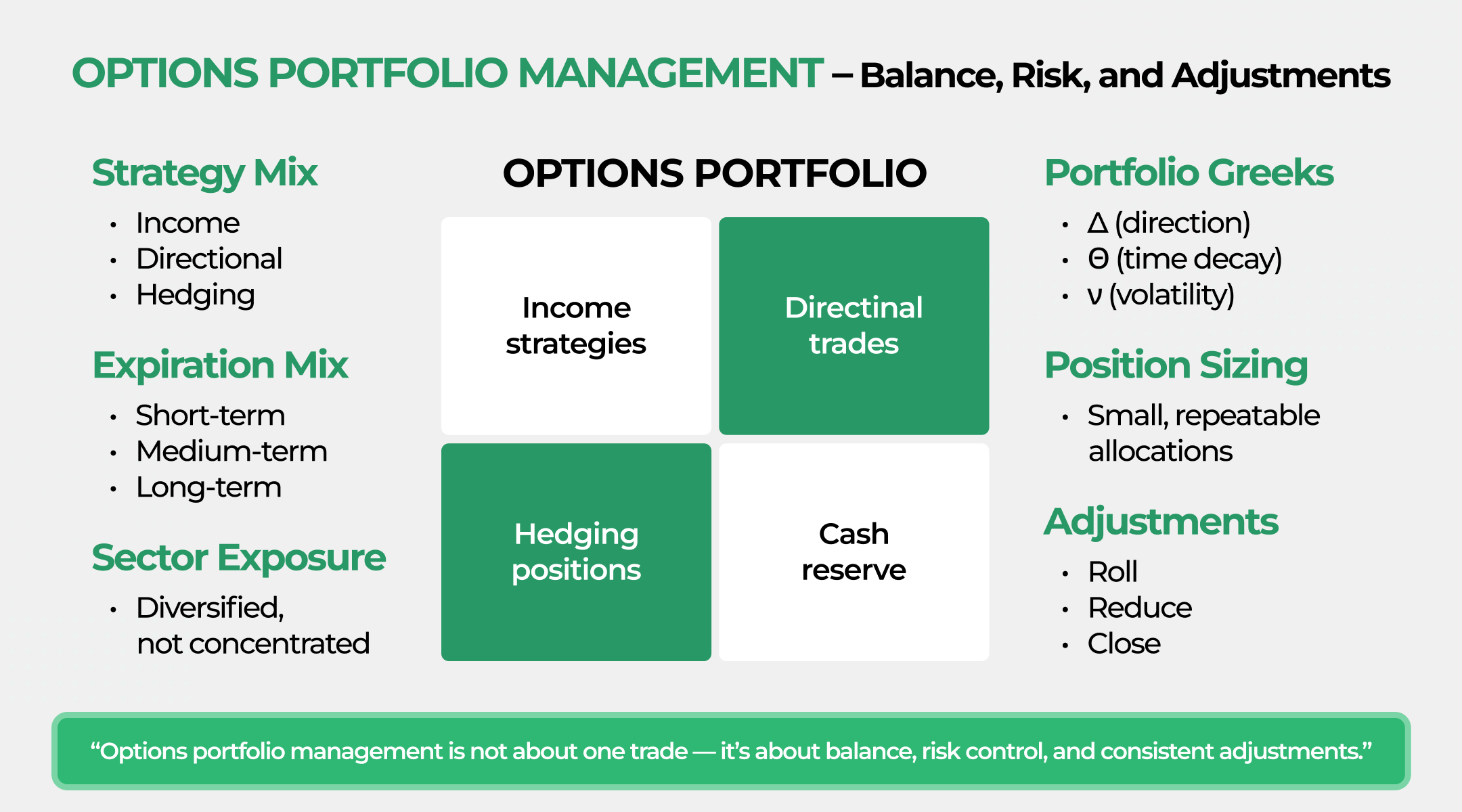

Core Elements of an Options Portfolio

Strong options portfolio management starts with structure. A trader cannot rely on one strategy or one market view. The goal is to spread exposure so no single trade or sector can ruin the account.

Diversification is the first step. An options portfolio should include different strategies, like covered calls for income, protective puts for insurance, and spreads for controlled risk. Expiration dates matter too. Mixing short-term and longer-term contracts avoids putting all exposure on one date. Strike selection is another lever, since choosing both near-the-money and out-of-the-money strikes helps balance potential returns with cost. Finally, sector diversification prevents heavy concentration in a single industry.

Allocation is just as important. For instance, you may choose to limit a single position to 5-10% of total portfolio value. While this is just an example, a similar action may ensure no one trade grows too large. Within that framework, riskier strategies get smaller allocations, while defined-risk strategies may allow for larger size.

For practical option management, balance is key. Calls, puts, and spreads should work together to create defined outcomes. If one side of the market moves against you, another position should help offset the loss. This does not eliminate risk, but it helps keep the portfolio steady.

Options risk management begins with these elements. Without them, even the best strategy will not hold up in real trading conditions.

Options Portfolio Management Principles

Options risk management is what separates a consistent trader from one who relies on luck. In options portfolio management, every trade adds exposure to the whole account. Without risk controls, even a small position can snowball into big losses.

The Greeks are the most practical way to measure and control exposure. Delta shows how sensitive your options portfolio is to price changes in the underlying. Gamma tracks how quickly Delta will change, which matters as expiration gets closer. Theta measures time decay, an important factor if you sell options for income. Vega shows how much volatility impacts your portfolio value. Together, these metrics make risk visible instead of guessing.

One of the most practical applications of these metrics is the concept of portfolio delta, an idea popularized by Tom Sosnoff. It treats your entire options book as one combined position and compares its expected movement to the S&P 500. This makes it easy to see whether your portfolio as a whole leans bullish, bearish, or neutral, not just on individual trades, but relative to the broader market.

Here is a simple reference table. Keep in mind that these numbers are not rules. They are only examples showing how two traders with different styles might shape their risk exposure. Each target involves a trade-off, more stability vs. more opportunity, more income vs. more volatility, and so on:

Risk Metric | Trader 1 (Lower Risk Preference) | Trader 2 (Higher Risk Preference) | Explanation & Trade-Off |

Portfolio Delta | -0.2 to +0.2 | -0.4 to +0.4 | A tighter delta range keeps directional exposure small, reducing drawdowns but limiting upside. A wider range allows stronger market views but increases volatility of returns. |

Total Theta (per day) | +$50 to +$100 | +$200 to +$400 | Lower theta means fewer short-premium positions and less vulnerability to volatility spikes. Higher theta increases income potential but adds risk during fast market moves. |

Max Position Size | 5% of portfolio | 10% of portfolio | Smaller sizing protects the portfolio from single-trade failures but slows growth. Larger sizing magnifies gains and losses, which suits traders comfortable with higher variance. |

Sector Exposure | 20% max | 35% max | Keeping exposure low avoids concentration risk but can dilute returns when a sector is trending. Allowing higher exposure creates more focused bets but increases correlation during downturns. |

Practical option management also means knowing when to exit. Clear stop-loss rules prevent emotional decisions. This will largely depend on your risk tolerance and market view, but for instance you could choose to cut losses at two times the credit received for a short option.

Profit-taking is equally important. Another example? A trader may choose to close at 50-75% of max profit to reduce risk. Exit triggers can also include time. For instance, some traders prefer rolling around the 21-day mark, but the right timing varies widely depending on the strategy

In the trade log you can find on our options screener, we track portfolio Greeks and even the total time value across all open trades. This gives a complete view of exposure that platforms like ThinkOrSwim, Robinhood, or TastyTrade do not provide. It helps traders adjust before problems build up.

Effective options portfolio management is not a one-time step. It is a daily habit that keeps an options portfolio safe and balanced.

Option Management in Practice

Option management is the daily work of monitoring and adjusting positions so the overall options portfolio stays aligned with goals. Trades are not static. Market conditions change, and without adjustments, even a solid setup can turn into a problem.

The main tools in options portfolio management are:

- Rolling: moving a position forward in time or to a new strike to keep exposure in line.

- Adjusting strikes: shifting risk levels up or down as the underlying price moves.

- Closing early: taking profit or cutting losses before expiration when risk-reward no longer makes sense.

These adjustments are not random. They are triggered by specific signals, such as profit targets, stop-loss levels, or time left until expiration. Clear rules help avoid emotional decisions.

Here is a table that attempts to give you a better idea of the matter. These triggers are examples, not universal rules. Different traders prioritize different things: speed of adjustment, risk tolerance, and how actively they want to manage positions. The table shows how two traders might handle the same situation with different thresholds.

Trigger Point | Trader 1 Action (More Cautious) | Trader 2 Action(More Flexible) | Explanation & Trade-Off |

50–75% of max profit reached | Close position and lock gains | Hold longer or close selectively | Taking profits early reduces exposure to late-stage volatility but limits total profit. Holding longer seeks full value but increases gamma and gap risk. |

Loss reaches ~2× credit received | Exit immediately | Evaluate conditions; may adjust before closing | Hard stop-loss avoids large drawdowns but may cut trades too early. A flexible trader may adjust or hedge, accepting higher risk for potential recovery. |

≈21 days to expiration | Roll forward to reduce gamma risk | Hold longer and roll later if needed | Rolling early controls gamma and avoids fast P/L swings. Waiting gives more time for theta decay but increases exposure to large directional moves. |

Underlying moves ~10% | Adjust strikes or reduce size | Monitor trend; adjust only if thesis changes | Quick adjustments maintain tight risk control but increase trading frequency. Waiting reduces activity and fees but carries more directional risk. |

In options portfolio management, these small actions prevent one trade from putting the entire portfolio at risk. Combining adjustments with broader options risk management ensures that positions keep working together rather than pulling the account in opposite directions.

Done consistently, option management makes the portfolio more stable and helps avoid surprises that come from leaving trades unchecked.

Building an Options Portfolio Step by Step

The first step in options portfolio management is deciding what you want the portfolio to achieve. Goals shape every choice.

A trader focused on income may use covered calls or credit spreads. Someone focused on protection may rely more on puts. For growth, directional trades like long calls and vertical spreads can be added. Without a clear objective, the portfolio can easily drift into random trades.

Position sizing is the next layer. No single trade should dominate the account. For instance,a trader may choose to keep individual positions at 1-5% of total capital, depending on risk. This is especially important when working with low cost options trading strategies, where smaller premiums can encourage overtrading and accidental concentration if sizing rules are ignored.

Directional trades, which carry more uncertainty, should stay on the smaller side. Defined-risk strategies such as spreads may allow for slightly larger allocations. Hedging positions, while not always profitable on their own, should still get room in the options portfolio because they protect other trades.

A simple allocation table can help. These allocations are examples only. Different traders prioritize income, growth, or protection depending on their goals and risk tolerance. The table shows how two traders might structure the same portfolio in different ways.

Strategy Type | Trader 1 Allocation(More Stable) | Trader 2 Allocation (More Growth-Oriented) | Explanation & Trade-Off |

Income strategies | 50% | 35% | A higher income allocation provides steady premium flow and smoother returns, but limits upside. Reducing income positions frees capital for directional trades but increases P/L volatility. |

Directional trades | 20% | 40% | Smaller directional exposure lowers drawdown risk but captures fewer big moves. Larger directional exposure can accelerate gains in trending markets but increases variance and uncertainty. |

Hedging positions | 20% | 15% | More hedging keeps downside controlled but reduces net returns. Less hedging boosts performance during calm markets but leaves the portfolio vulnerable during sharp declines. |

Cash reserve | 10% | 10% | Maintaining a fixed cash buffer adds flexibility and reduces forced decisions. Keeping it flat across styles balances optionality with capital efficiency. |

Blending strategies into one portfolio makes risk more manageable. For example, selling a covered call can bring steady income, while a protective put ensures large losses are capped. Adding a small position in a call spread may capture upside without exposing too much capital.

So, to recap this part:

- Define goals before placing trades

- Size positions based on risk, not just conviction

- Balance income, protection, and growth to keep the options portfolio stable

When done consistently, this step-by-step approach turns option management into a structured process instead of guesswork.

Example of a Balanced Options Portfolio

In options portfolio management, a conservative trader can split a $50,000 account across income, directional, hedging, and cash in line with the earlier allocation targets.

- Income strategies (50%): $25,000 placed in covered calls and credit spreads. The goal is to generate steady premium income while keeping risk defined. Expected returns are modest but consistent.

- Directional trades (20%): $10,000 in call or put spreads. These trades allow participation in market moves without risking too much capital. Maximum loss is limited to the debit paid.

- Hedging positions (20%): $10,000 in protective puts under selected holdings. These act as insurance, capping downside if markets pull back.

- Cash reserve (10%): $5,000 left unallocated. This gives flexibility to add trades or adjust existing ones without overexposing the portfolio.

This setup shows how diversification and clear limits work together. Income strategies take the largest share because they are more predictable. Directional trades and hedging are balanced equally, giving both upside potential and downside protection. The cash reserve provides breathing room.

Through consistent option management, the portfolio remains stable while still allowing for growth. Options risk management ensures each part supports the bigger picture rather than working against it.

Monitoring and Adjusting an Options Portfolio

Another important thing to know about options portfolio management is that monitoring is a routine, not a one-time task. Daily checks should focus on portfolio delta to keep directional risk balanced. This becomes even more critical with short term options trading, where fast theta decay and rising gamma can shift portfolio exposure much faster than in longer-dated positions. Weekly reviews can track theta exposure, making sure time decay is working in your favor, and check sector concentration to avoid overloading one industry.

Practical tools make this easier. Many traders use spreadsheets to log trades, journals to record reasoning, and analysis software to track Greeks in real time. A good system shows not just individual positions, but the combined effect on the options portfolio.

By combining option management with consistent tracking, traders avoid blind spots. Options risk management works best when it is applied every day, not just when a problem appears.

Common Mistakes in Options Portfolio Management

Even with good planning, traders often fall into predictable traps. The biggest risk in options portfolio management is overconcentration. Putting too much capital into one sector or one strategy exposes the account to unnecessary swings. Diversification keeps losses contained.

Another common mistake is ignoring Greeks. Without tracking Delta, Gamma, Theta, and Vega, a trader may unknowingly load the portfolio with too much directional risk or excessive time decay. Regular checks are part of effective options risk management.

Holding trades too close to expiration without adjustments is also risky. Gamma increases sharply in the final days, making small price moves dangerous. Rolling or closing positions early keeps risk controlled.

Quick mistakes and fixes:

- Overconcentration: many traders reduce this risk by spreading exposure across sectors and strategies

- Ignoring Greeks: regular monitoring helps avoid hidden risks

- Holding to expiration: some traders reduce gamma exposure by managing trades before the final weeks

- No exit plan: defining profit and loss guidelines ahead of time helps maintain discipline

Smart option management avoids these pitfalls and keeps the options portfolio steady.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.