Trade Idea - Long Call ZEBRA on KMI

Published on August 5, 2025(Last updated on September 5, 2025)

Disclaimer: The trades discussed in this blog reflect the author's personal strategies and decisions. These are not financial advice and should not be considered recommendations to buy, sell, or hold any financial instruments. The author is not a licensed financial advisor. Options trading carries significant risk, and readers should perform their own research or consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Today, I opened a bullish position on Kinder Morgan (KMI) using a long call ZEBRA strategy that allows for synthetic long exposure with limited risk and reduced capital requirements. This structure is especially compelling when a stock appears poised to break higher but I want to avoid tying up large amounts of capital or facing undefined risk.

With KMI trading around $27.10, I’m constructing this position to participate in upside movement as the stock trends toward its average analyst price target of $31.76. The recent earnings report and favorable industry tailwinds both support a bullish bias.

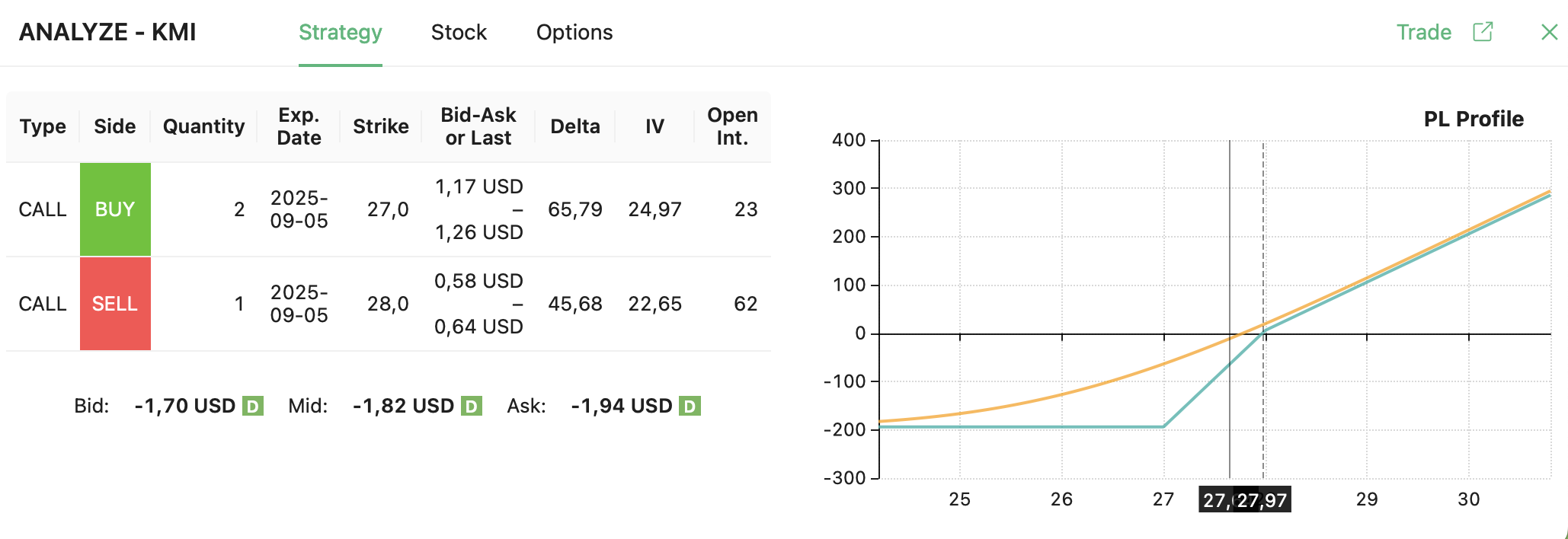

The Trade

All options are in the September 2025 expiration:

- Buy 2× 27.0 Calls

- Sell 1× 28.0 Call

The P&L looks like this:

This setup results in a net debit of approximately $1.82 per share, or $182 total per spread. It provides nearly 1:1 upside participation beyond the long strike, with risk tightly defined to the initial outlay.

Also, I'm posting the price chart at the moment I opened the trade:

Why KMI?

Kinder Morgan looks well-positioned for multi-year growth, supported by three key themes:

- Rising Global Demand for Natural Gas

As the world leans more on natural gas, especially LNG, KMI plays a central role - moving roughly 40% of the gas feeding U.S. LNG export terminals. The company expects global demand for natural gas to increase by 25% by 2050, and it has the infrastructure to capitalize. - Massive, Contract-Backed Project Pipeline

In Q2 2025, KMI added $1.3 billion in new projects, bringing its total backlog to $9.3 billion. Roughly half of this is aimed at growing power needs, while the other half secures long-term recurring income. The predictability of cash flows enhances the attractiveness of a long-term bullish strategy. - Favorable Regulatory and Tax Outlook

Permitting timelines are shrinking and new tax policies allow KMI to write off more capital expenditures. Management expects to pay minimal federal income tax through at least 2028, giving the company more flexibility to invest or return capital to shareholders.

Recent Earnings Paint a Supportive Picture

Kinder Morgan’s Q2 2025 earnings matched expectations with EPS of $0.28, while revenue grew 13% YoY to $4.04 billion, beating estimates by over 4%. Strength came primarily from the Natural Gas Pipelines and Terminals segments, offsetting some weakness in Product Pipelines.

The company's reaffirmed 2025 outlook includes:

- $2.8 billion in net income (+8% YoY)

- $1.27 adjusted EPS (+10%)

- $1.17 dividend per share

- $8.3 billion adjusted EBITDA

These metrics indicate steady performance and shareholder-friendly capital allocation.

Trade Breakdown

- Max Risk: below $200 (initial debit)

- Breakeven: $27.97 at expiration

- Upside Potential: Substantial if KMI breaks above $28, with increasing gains toward and beyond the $31.76 target

- Downside Risk: Capped at the initial debit

- Return if Target is Reached: If KMI rises to just under $32 by expiration, the trade could return well over 100% on risk. The price is quite far and I don't think this is likely to happen. But it's good to know.

With the energy sector seeing renewed capital inflows and KMI showing strong fundamentals, this ZEBRA setup gives me a capital-efficient way to get long without taking on the risks of owning shares outright.

This trade is part of my public trade log and will be tracked accordingly. As always, I may adjust or exit the position depending on how price and volatility evolve over the coming weeks.

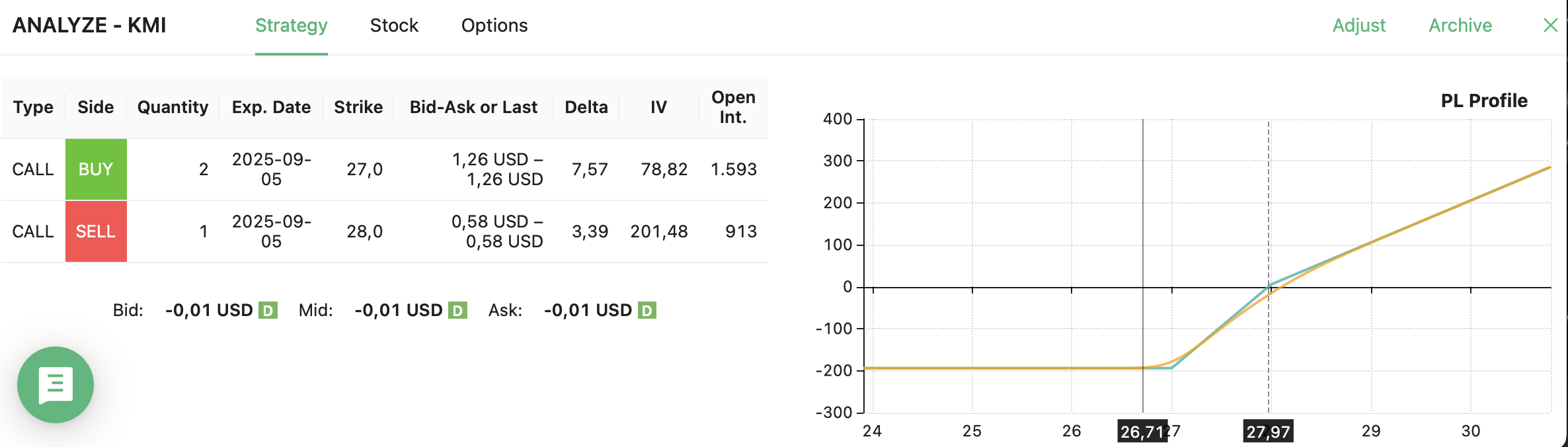

Update: Trade Closed

The trade did not play out as expected. KMI had a strong decline a few days after I opened the position on rather low volume and no apparent news, since then it sort of got stuck and never recovered:

That's ok, I'm glad I used a trade with a built-in stop loss like KMI, the loss is more than bearable.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.