No Loss Option Strategies - How True Zero Risk Trades Really Work

Published on December 22, 2025(Last updated on March 17, 2026)

Table of Contents

- Key Takeaways

- Options Trading without loss

- Why many traders say a no loss option trading strategy does not exist

- The role of put-call parity in building a no loss option strategy

- How to create a no loss option strategy

- An Example of Mispricing on Standard vs Synthetic Strategies (The Origin of No Loss Option Strategies)

- No Loss Option Strategy Example #1 - Zero risk collar

- No Loss Option Strategy Example #2 - Box spread

- No Loss Option Strategy Example #3 - Zero risk butterfly

- Read More

Reviewed by Leav Graves

Table of Contents

- Key Takeaways

- Options Trading without loss

- Why many traders say a no loss option trading strategy does not exist

- The role of put-call parity in building a no loss option strategy

- How to create a no loss option strategy

- An Example of Mispricing on Standard vs Synthetic Strategies (The Origin of No Loss Option Strategies)

- No Loss Option Strategy Example #1 - Zero risk collar

- No Loss Option Strategy Example #2 - Box spread

- No Loss Option Strategy Example #3 - Zero risk butterfly

- Read More

A no loss option strategy sounds impossible, but it isn’t. Traders hear mixed messages about risk-free options trading and what a real no loss option trading strategy should look like. This article explains when a zero risk option strategy is actually possible and why pricing gaps create these rare opportunities.

KEY TAKEAWAYS

- A no loss option strategy is a trading setup where the combined options position has zero net downside because the legs offset perfectly through put call parity or price misalignment.

- Traders often confuse risk-free options trading with fake definitions where one trade covers another, which is not a true no loss option strategy.

- A zero risk option strategy only exists when the price of a position differs from the price of its synthetic equivalent, allowing a long-short combination with no negative outcomes.

Options Trading without loss

A no loss option strategy works only when the position’s legs offset each other perfectly, usually because put call parity or a short lived pricing gap forces the payoff to sit at zero downside. Some of these setups are extremely short term, while others stay available for much longer depending on how they form.

In practice, there are three types of opportunities traders might run into:

- Pure price mismatches between a strategy and its synthetic version

These exist, but they are very hard to capture. They tend to appear for seconds or minutes and disappear as soon as market makers correct the prices. For most retail traders, they are simply too fast to act on. - Deep ITM put or call combinations that behave like a box spread

These can be easier to find and may stay open longer, but they often come with a high assignment risk. The payoff can still form a no loss option trading strategy, but the operational reality can get messy. - Put call parity setups with a stable no loss payoff

These are the most practical for retail traders. They remain available longer, and they are easy to execute, but they require a large amount of capital. The return usually mirrors the risk free rate, so small accounts won’t feel the benefit.

This is why some no loss option strategy setups feel impossible to catch, while others behave more like stable, slow moving forms of risk free options trading.

Why many traders say a no loss option trading strategy does not exist

Many traders argue that a no loss option trading strategy cannot exist because they think of it in the same way they think of a directional trade. They look for a setup where a small amount of capital magically avoids losses. By that standard, it really does look impossible. But the argument is only half right. If short-term bonds pay a risk free rate, then certain option structures can reflect the same idea. The return is small, but still above zero, so the logic that “no loss option strategies are impossible” doesn’t hold.

A second misconception comes from a YouTube-friendly trick you may have seen: the claim that you can create a no loss option strategy by doing two consecutive trades. The logic goes like this: “Trade A earns $100, and Trade B risks less than $100, so Trade B is risk free.” It sounds nice, but it falls apart immediately. Trade A was not risk free in the first place, so its profit cannot be used as a safety cushion. If Trade A fails, the entire construction fails. In other words, using the gains from one risky trade to justify another does not create a no loss option strategy. It simply hides the risk behind the timing of the trades.

A true zero risk option strategy needs one simple condition: the position must have no downside in any scenario, without relying on past gains. In practice, this only happens when pricing forces a risk free options trading window through the put-call parity, and the following section will clarify this concept.

The role of put-call parity in building a no loss option strategy

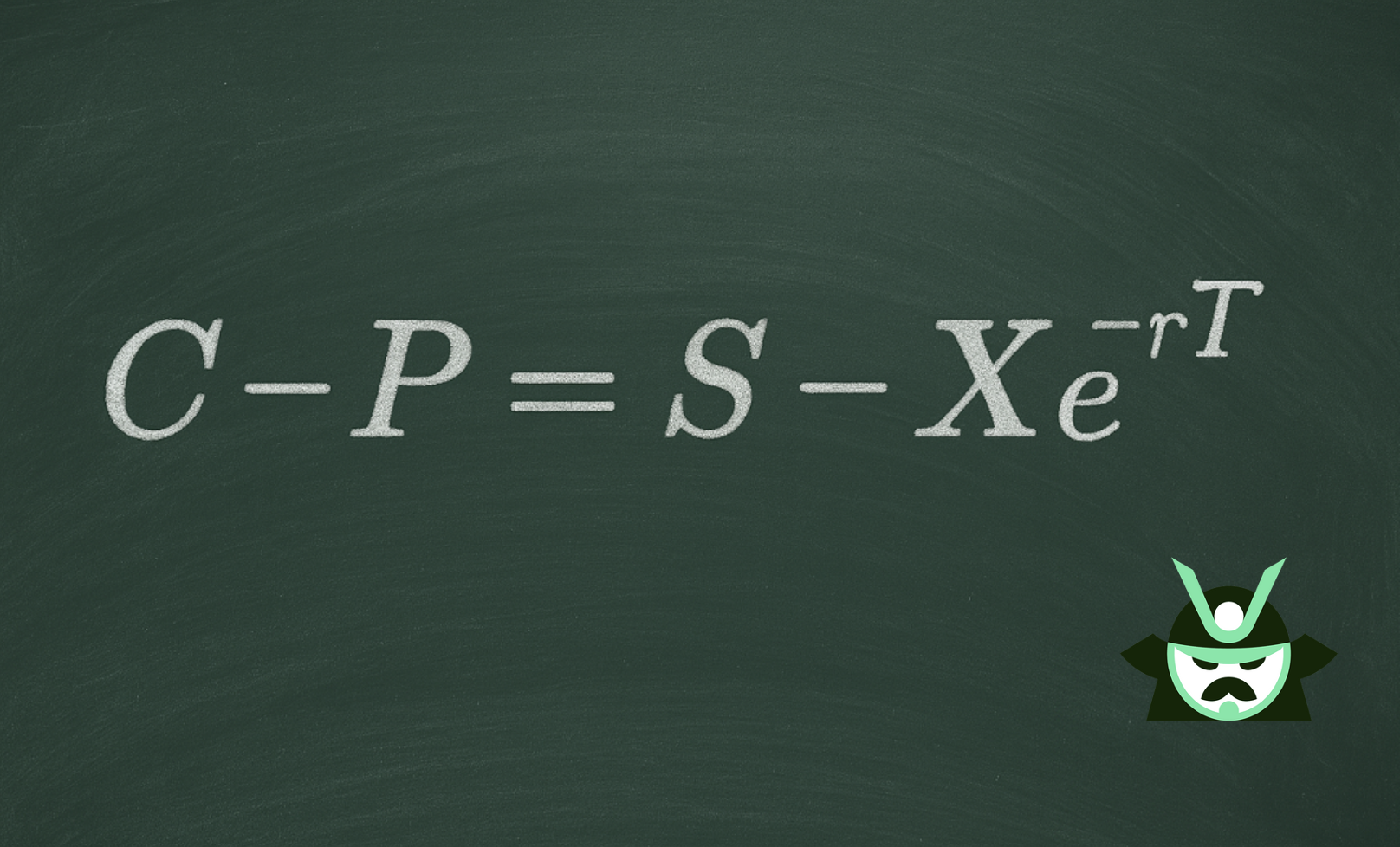

Put call parity is the backbone of any no loss option strategy because it tells you what a call, a put, and the underlying stock must cost when they share the same strike and expiration.

The basic formula shown above is simple: call price (“C”) minus put price (“P”) equals the stock price (“S”) minus the discounted strike (which is the strike price “X” multiplied by the exponential function of the product between the risk-free rate “r” and the time to expiration “T”, changed in sign). When this relationship holds, everything is in balance. When it doesn’t, a no loss option trading strategy becomes possible.

The key idea is that put call parity already embeds the risk free rate. Even when prices line up perfectly, the relationship between the call, put, and forward value of the stock creates a built in risk free return. That alone can form a no loss option strategy. A price mismatch simply boosts the profit. If the direct strategy is priced exactly in line with its synthetic version, you can still lock in the risk free rate by holding one and offsetting the other. If a mismatch appears, you long the cheaper side and short the richer side, which adds extra yield but doesn’t change the core concept. In both cases, you are not predicting direction. You are using parity to extract a payoff that cannot go negative.

This is why a zero risk option strategy is possible, contrarily to what one may believe. You are simply taking advantage of parity forcing two different paths to the same payoff. When their prices drift apart, you have a zero-risk profit, and the structure becomes a no loss option strategy by definition.

How to create a no loss option strategy

The simplest way to build a no loss option strategy is to compare a standard strategy with its synthetic version and see which one is mispriced. A common example is the long call versus its synthetic twin, which is long 100 shares and long one put at the same strike and expiration. Both should produce the same payoff. If they don’t, you have a window to build a no loss option trading strategy.

Say the call is more expensive than the synthetic. In that case, you short the overpriced call and buy the cheaper synthetic version. You lock in the price gap at entry. The position is still bullish because both structures benefit if the stock goes up. The key is that the synthetic is cheaper, so the combined payoff cannot go negative. Even if the stock drops, the pricing difference cushions the move and turns the structure into a zero risk option strategy.

An Example of Mispricing on Standard vs Synthetic Strategies (The Origin of No Loss Option Strategies)

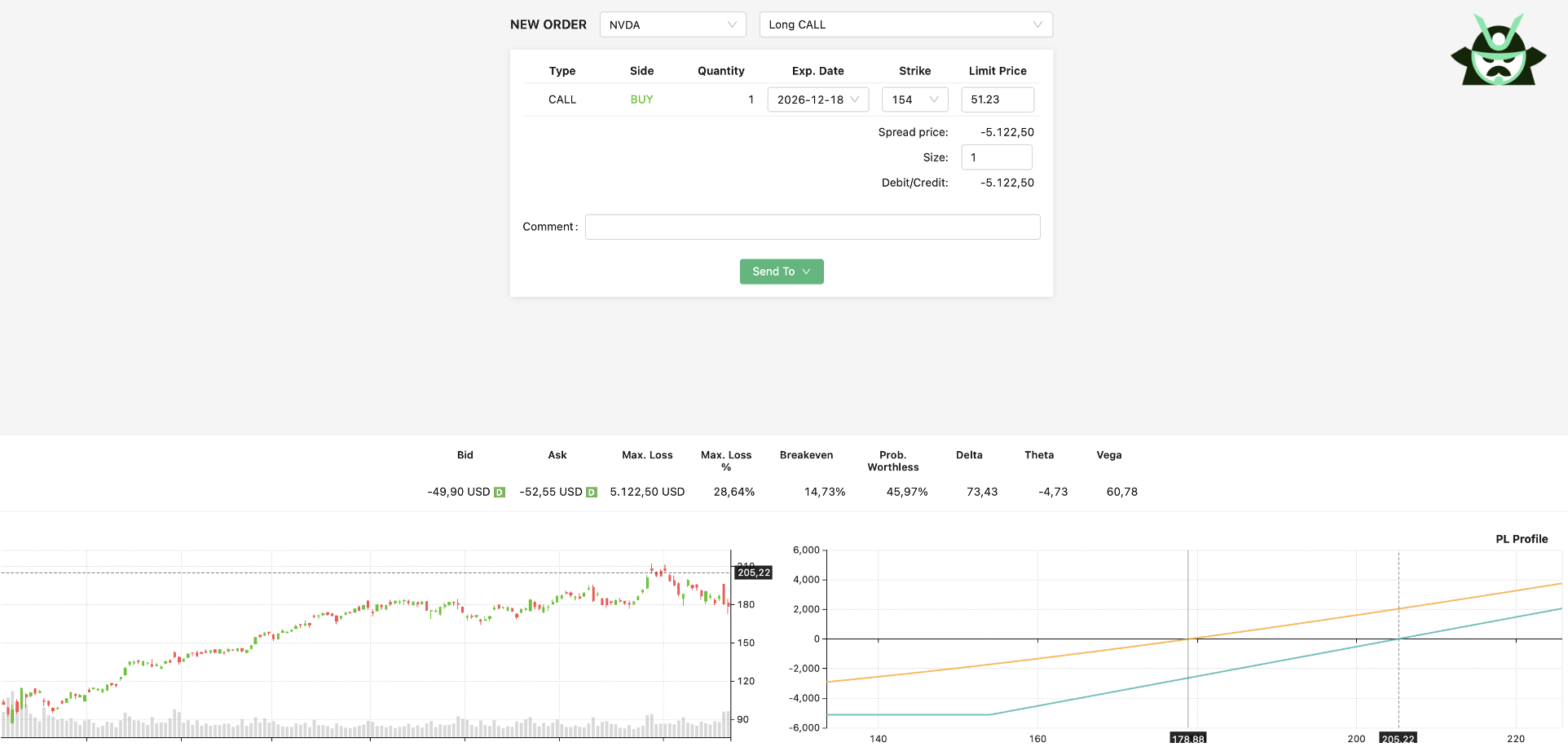

Let’s look at a practical example on NVDA with the help of our options strategy screener. This will allow us to show how a no loss option strategy can appear when the standard call and its synthetic version drift apart. Take options expiring one year from now. With NVDA trading at 178.88, look at the $154 strike.

As shown in the chart above, the long $154 call has a maximum loss of $5,122.50.

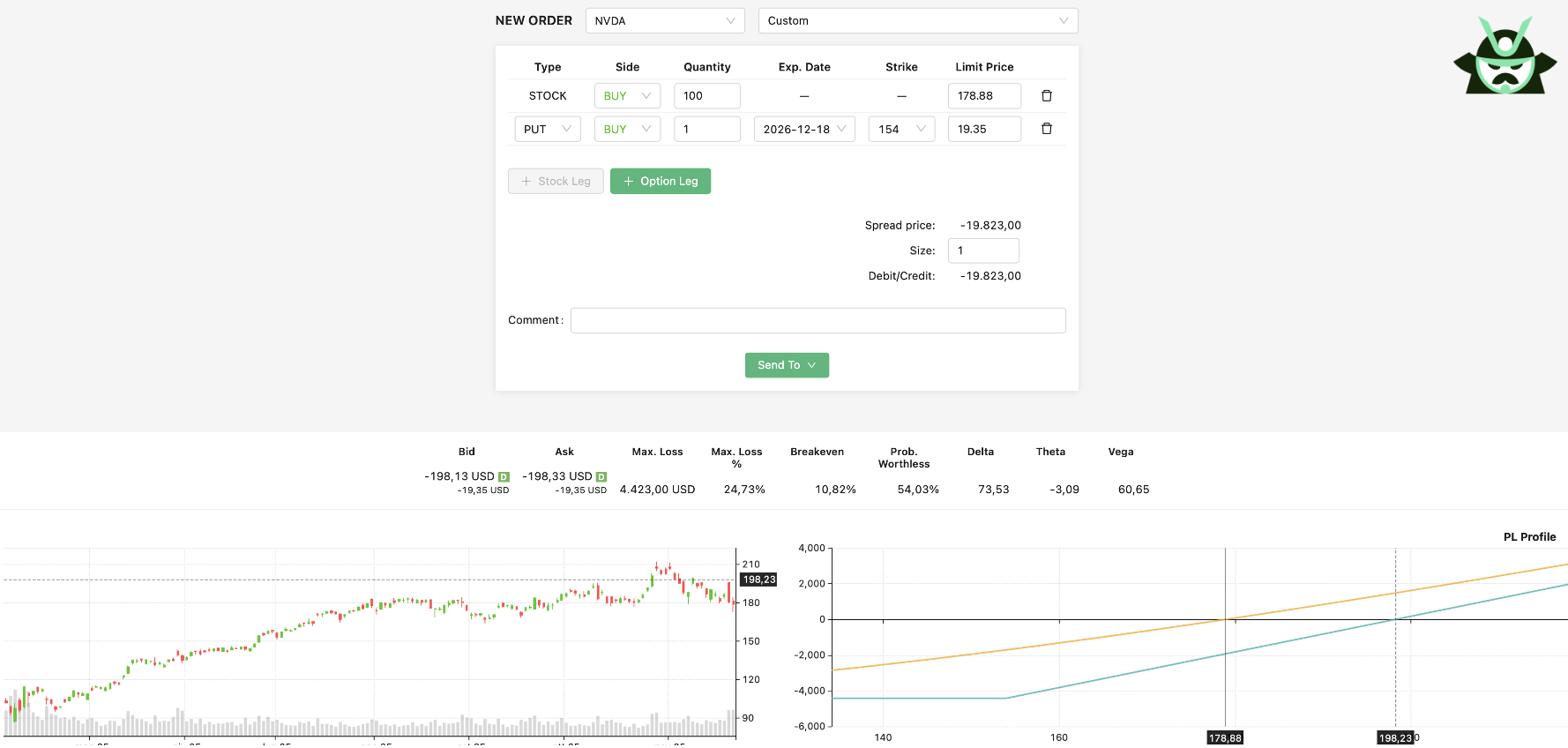

You would expect the synthetic call, built by buying 100 shares and going long on the $154 put, to show the same downside:

And yet, as you can see above, it doesn’t. The synthetic version has a maximum loss of $4,423.

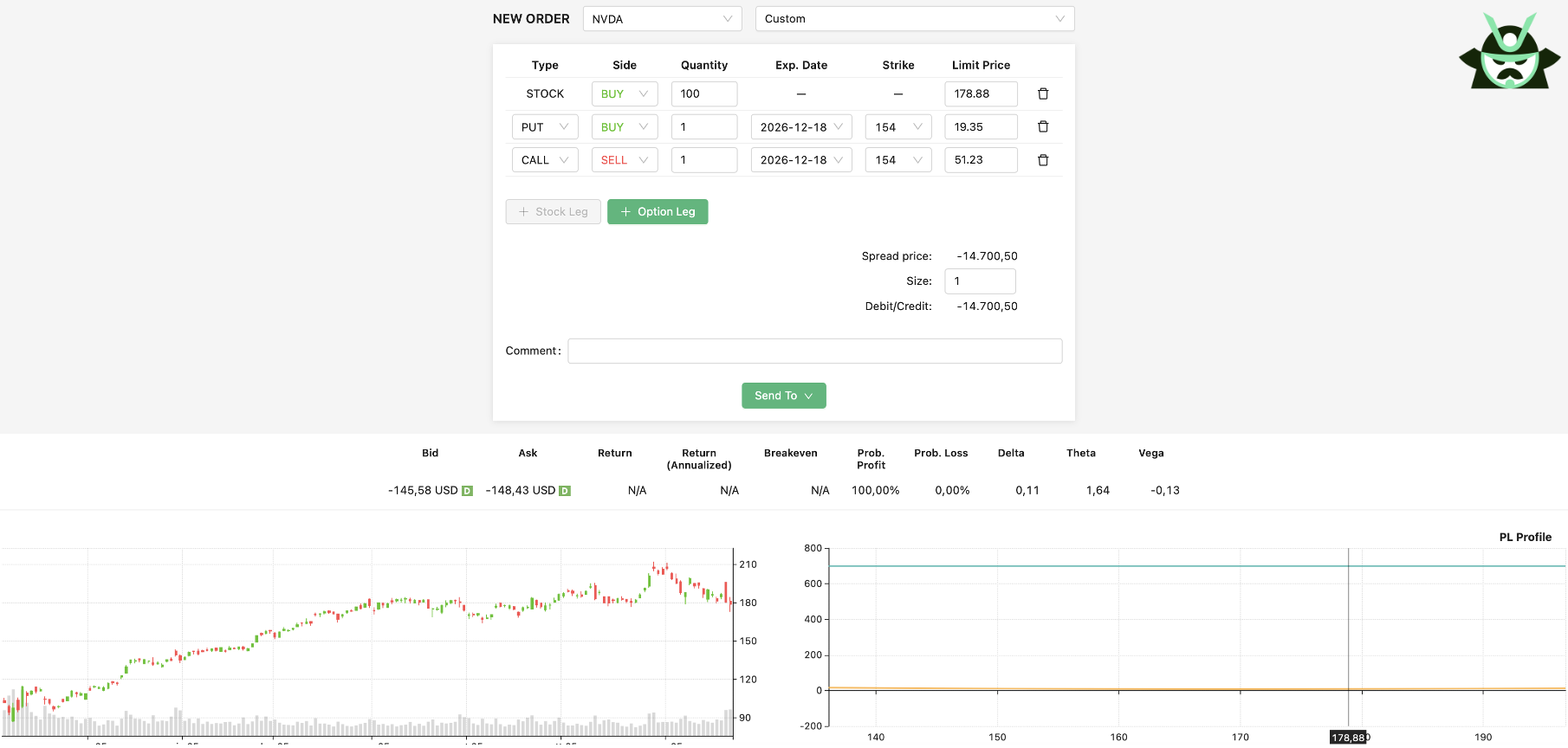

That gap means the call is overpriced relative to its synthetic version. To build a no loss option trading strategy from this, you short the expensive call and go long the cheaper synthetic structure:

Look at the chart above: no matter where NVDA finishes, the difference between the two payoffs guarantees a gain of $699.50 over the year.

A quick breakdown helps:

- You buy 100 NVDA shares at 178.88

- You buy the $154 put for $2.68 (times the 100 multiplier)

- You sell the $154 call for $27.90 (times the 100 multiplier)

The net cost is $15,366, which is above 4% return for a zero risk option strategy. Feel free to check: that sits close to the yield on short term US bonds, which explains why risk free options trading often mirrors the risk free rate.

Can you earn more than the risk free rate? Yes, but only if you accept the chance of earning less. Once you open that door, more interesting combinations become possible, as the next section shows. In practice, this is where more directional structures come into play: for example, combining synthetic positions with asymmetric exposure, like those used in risk reversal options, allows traders to tilt the payoff while still anchoring the logic to parity-based pricing. But let's not make things unnecessarily complicated and let's just look at our top 3 no loss option strategies below.

No Loss Option Strategy Example #1 - Zero risk collar

A collar uses the same pricing logic as the earlier example, just applied to different strikes. A normal collar is simple: you own 100 shares, buy a protective put, and sell a covered call to offset part of the cost. Most collars require a debit because the put usually costs more than the call brings in. But when mispricing appears on the strikes you choose, a collar can turn into a no loss option strategy.

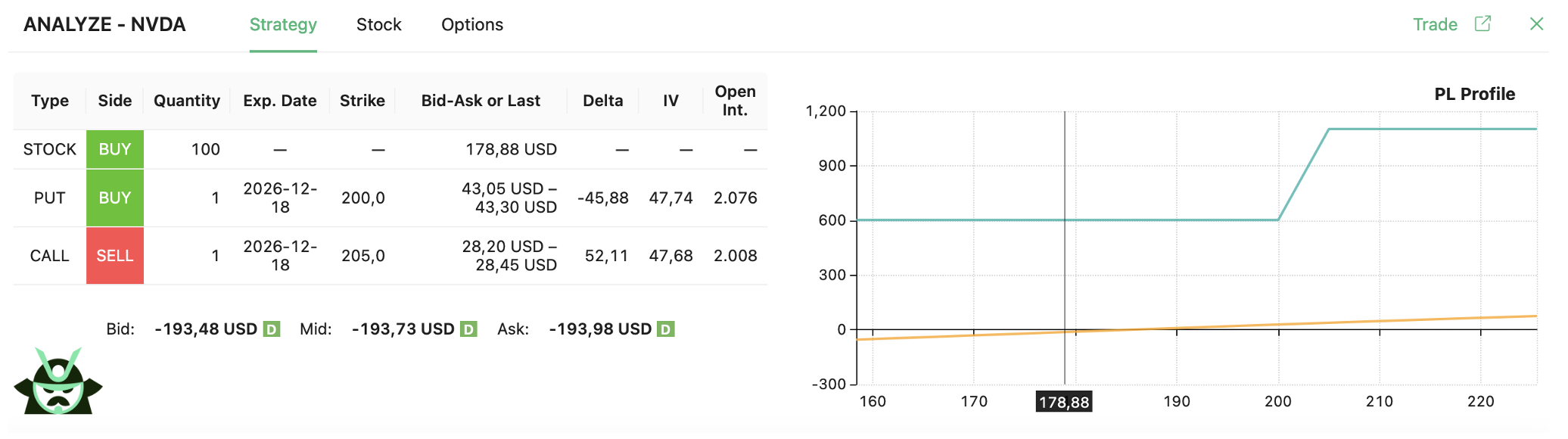

Take, again, NVDA options expiring a year from now. Start with a bullish case: long 100 shares, long the $200 put, and short the $205 call.

In this setup, you either earn $602 if NVDA stays below $200 or $1,102 if NVDA finishes above $205. The $500 jump between these outcomes comes from the 5 point strike difference multiplied by 100 shares. This is exactly how a no loss option trading strategy behaves when the collar is priced in your favor. Notice that your profit will either be equal to 3.11% (less than the risk free rate) or 5.69% (more than the risk free rate).

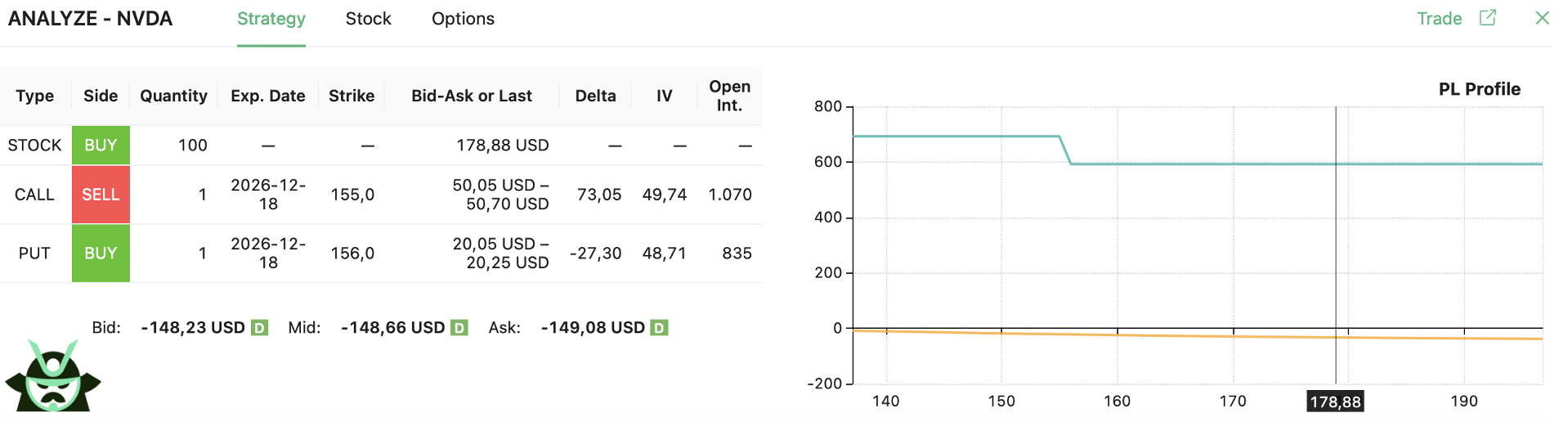

Now flip to a bearish case using the same idea. Go long 100 shares, short the 155 call, and long the 156 put:

Here you earn $592 if NVDA closes above $156, or $692 if it drops below $155. Again, the profit gap is exactly $100 dollars, which matches the 1 point difference between the strikes. Your profit will therefore move between 3.49% and 4.16%.

This structure works because the put and call legs create a fixed payoff range, turning the position into a reliable form of risk free options trading when parity aligns in your favor. And if you want to play around with this strategy, you can refer to the link at the bottom of this article, where we provide you with a pre-built Excel template to calculate collars based on this principle.

No Loss Option Strategy Example #2 - Box spread

We do not mean to mislead anyone: you don’t need to own shares to have a no loss option strategy. A box spread is one of the clearest ways to see how a no loss option strategy works without owning any underlying stocks. It creates a fixed payoff by combining four option legs built on the same two strike prices. The structure is simple:

- Buy an in the money call

- Sell an out of the money call

- Buy an in the money put

- Sell an out of the money put

These four legs create a payoff that is locked to the strike difference. If the box is priced below that fixed payout, you are looking at a no loss option trading strategy.

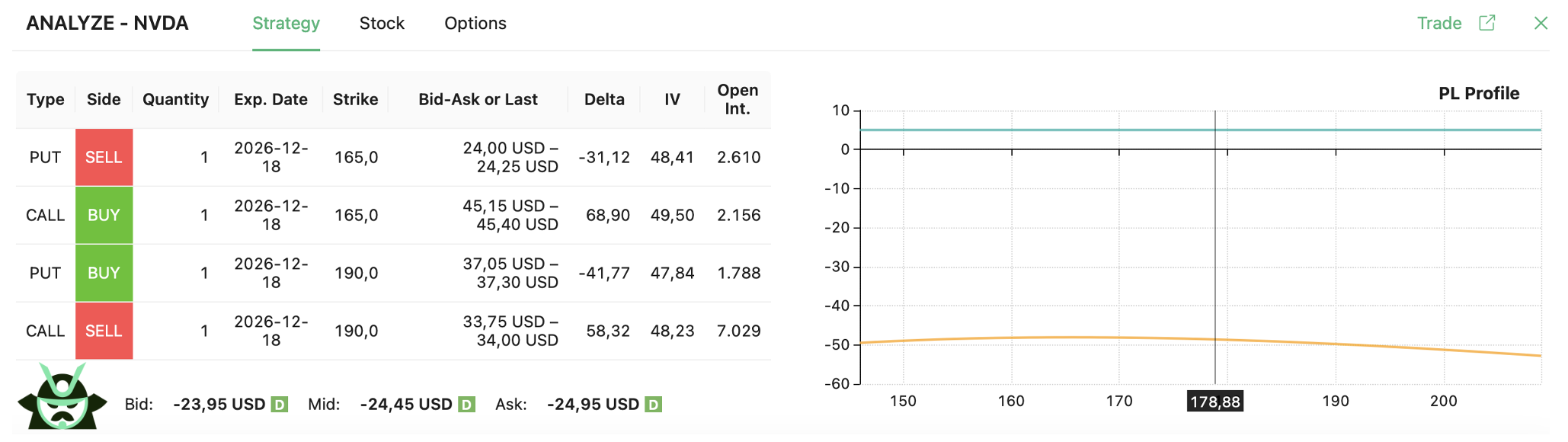

Take NVDA as an example. Using one year options:

- Sell the 165 put

- Buy the 165 call

- Buy the 190 put

- Sell the 190 call

If this box costs $2,495 and pays $2,500, the profit is $5. That’s not exciting, but it is guaranteed, which is the textbook definition of a zero-risk option strategy. The catch is the return. Five dollars on 2,495 is about 0.2%. It works, but it’s small.

This is why traders use box spreads mainly when they want risk-free options trading on a large size or when funding costs make the box attractive. The no-loss option strategy is real here, but the reward tends to mirror the market’s own risk-free rate.

Notice that this is the debit version of the box spread (or long box spread). There’s a riskier credit version (the short box spread) with an assignment risk you cannot ignore. The whole no loss logic is, however, valid for both versions of this strategy.

No Loss Option Strategy Example #3 - Zero risk butterfly

Another cool no-loss option strategy we want to mention is the butterfly. First things first: a regular butterfly is a simple structure built with three strikes, and it behaves like this:

- You buy a lower call

- You sell two calls at the middle strike

- You buy a higher call

A normal butterfly needs the stock to finish near the center strike to reach max profit. What changes in a no-loss option strategy is how you combine the butterfly idea with shares and a protective put to eliminate downside.

Take NVDA with one year to expiration. You can build this version by:

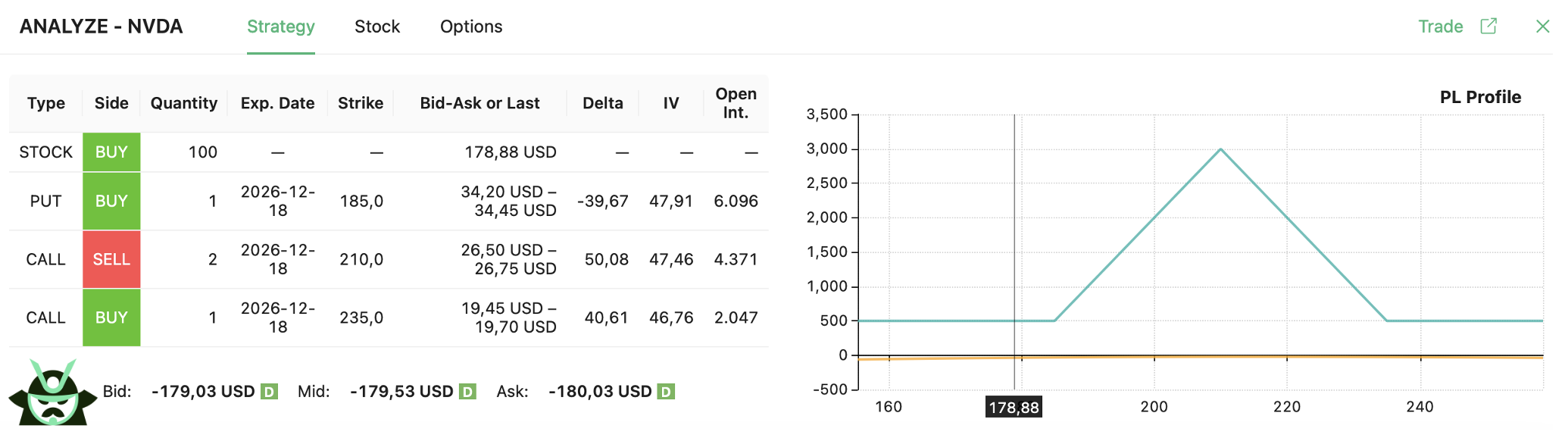

- Buying 100 shares at 178.88

- Buying the 185 put

- Selling two 210 calls

- Buying the 235 call

And here is your P&L chart:

If NVDA ends below 185, you earn 497. If it ends above 235, you also earn 497. These two outer regions create the “zero risk option strategy” floor. They give you guaranteed gains regardless of the stock direction, which is what makes this behave like a no-loss option trading strategy when the pricing lines up.

The middle area between 185 and 235 is where things can get interesting. The payoff rises and peaks at 210 with a max profit of 2,997. Is hitting that exact number realistic? Probably not. But trading does not need perfection. As time passes, the orange curve in your chart will usually lift. If at any point you see an open gain above the 500 level, you can simply close the trade and call it a day.

This mix of safety and optional upside is what makes the butterfly a fun addition to the no loss option strategy toolbox.

If you want to learn more about trading options, you can download our free options cheat sheet

Read More

Collar Calculator (Blog post with free included Excel template)

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.