Reviewed by Leav Graves

Theta in options measures how much value your contracts lose each day from time alone. But does time decay always work against you? How does it speed up near expiration, and can you use it to gauge portfolio risk? Below, you'll find options theta explained in simple, practical terms.

KEY TAKEAWAYS

- Theta in options tells you how much extrinsic value it loses each day as time passes. This is known as time decay.

- Theta works against option buyers (negative theta) and in favor of option sellers (positive theta), making it a core factor when choosing between long and short strategies.

- Time decay accelerates as expiration approaches, especially for at-the-money options, meaning options lose value faster in their final days.

Theta Options - What Is It?

Theta is the one-day rate of decline of an option's extrinsic (or time) value. Every option has a shelf life, and theta tells you how fast that shelf life is ticking away.

Options are decaying assets. Their extrinsic value erodes a little each day and drops to $0 if they expire out of the money. This is why understanding what theta is in options matters for every strategy you run.

For option buyers, theta is a headwind. The underlying stock needs to move far enough in your favor to overcome the daily time decay. That doesn't mean long positions can't be profitable - it just means time isn't on your side, and faster moves help.

For option sellers, it's the opposite. Theta in options works in your favor because the contract you sold is losing value every day. You can buy it back later at a lower price and pocket the difference. But as any guide with options theta explained will tell you, it isn't free money - if the stock moves against you, losses from price movement can easily outweigh the time decay you collected.

Here's a quick summary of how theta in options affects each side:

- Long options (buyers): Negative theta. Time decay works against you.

- Short options (sellers): Positive theta. Time decay works in your favor.

Options Theta Explained with a Real-World Analogy

Think of theta in options like an extended warranty. Say you buy a one-year warranty for $365. That's roughly $1 per day of coverage. After 100 days, you wouldn't expect to pay the full $365 for what's now only 265 days of remaining protection. Options work the same way - the closer you get to expiration, the less time value remains.

One common misconception: if you buy an OTM put for $3.00 with a theta of -0.10, you won't see a $0.10 debit hit your brokerage account each morning. Theta is a theoretical measure. It assumes everything else stays frozen and only time changes.

A Mistake Samurai Often Sees

We often see traders treat theta like a daily paycheck, expecting the exact decay number to show up in their P&L every morning. Then the stock moves, IV shifts, and the position behaves nothing like the theta number suggested. Theta is one input into the price, not a line item that gets deducted on its own. The sooner that clicks, the sooner the rest of the greeks start making sense together.

In practice, an option's price reflects all the options greeks at once. A call could be gaining value from the stock moving up (delta) while losing a bit from theta at the same time. The greeks can offset or amplify each other depending on what the market is doing.

Theta Options - A Practical Example

Say you buy an out-of-the-money put for $3.00 with a theta of -0.10. All else being equal (which is a purely theoretical case), after 10 days that option would lose roughly $1.00 in value, bringing it down to around $2.00.

From the seller's side, the math is the same but the direction flips. The seller collected $3.00 in premium, and after 10 days, the option is now worth about $2.00. They could buy it back for a $1.00 profit - without the stock doing anything dramatic.

The table below sums up the 2 cases we have just mentioned:

Scenario | Day 0 | Day 10 (all else equal, considering theta in options) |

Buyer paid | $3.00 | Option worth ~$2.00 |

Seller collected | $3.00 | Can buy back at ~$2.00 |

Theta effect | - | -$1.00 for buyer, +$1.00 for seller |

This is what theta in options looks like in practice - time passes, value shifts from buyer to seller.

What Does Theta Mean in Options and Extrinsic Value?

Theta only erodes an option's extrinsic value. It doesn't touch intrinsic value. This distinction matters because it changes how theta behaves depending on where the option sits relative to the stock price.

Quick refresher: intrinsic value is the amount an option is worth if you exercised it right now - for a call, that's the stock price minus the strike. Extrinsic value is everything else on top of that, driven mainly by time remaining and implied volatility. Theta only chips away at the extrinsic portion, as we explain below:

- Deep ITM options carry very little extrinsic value regardless of how much time is left. Their price is mostly intrinsic, so theta is minimal. For sellers, this is also a signal - deep ITM short options have a higher chance of early assignment since there's little time value left for the holder to preserve.

- OTM options are 100% extrinsic value. Theta directly tells you how fast that premium is melting away. If you're holding a long OTM option, theta is eating into your entire position.

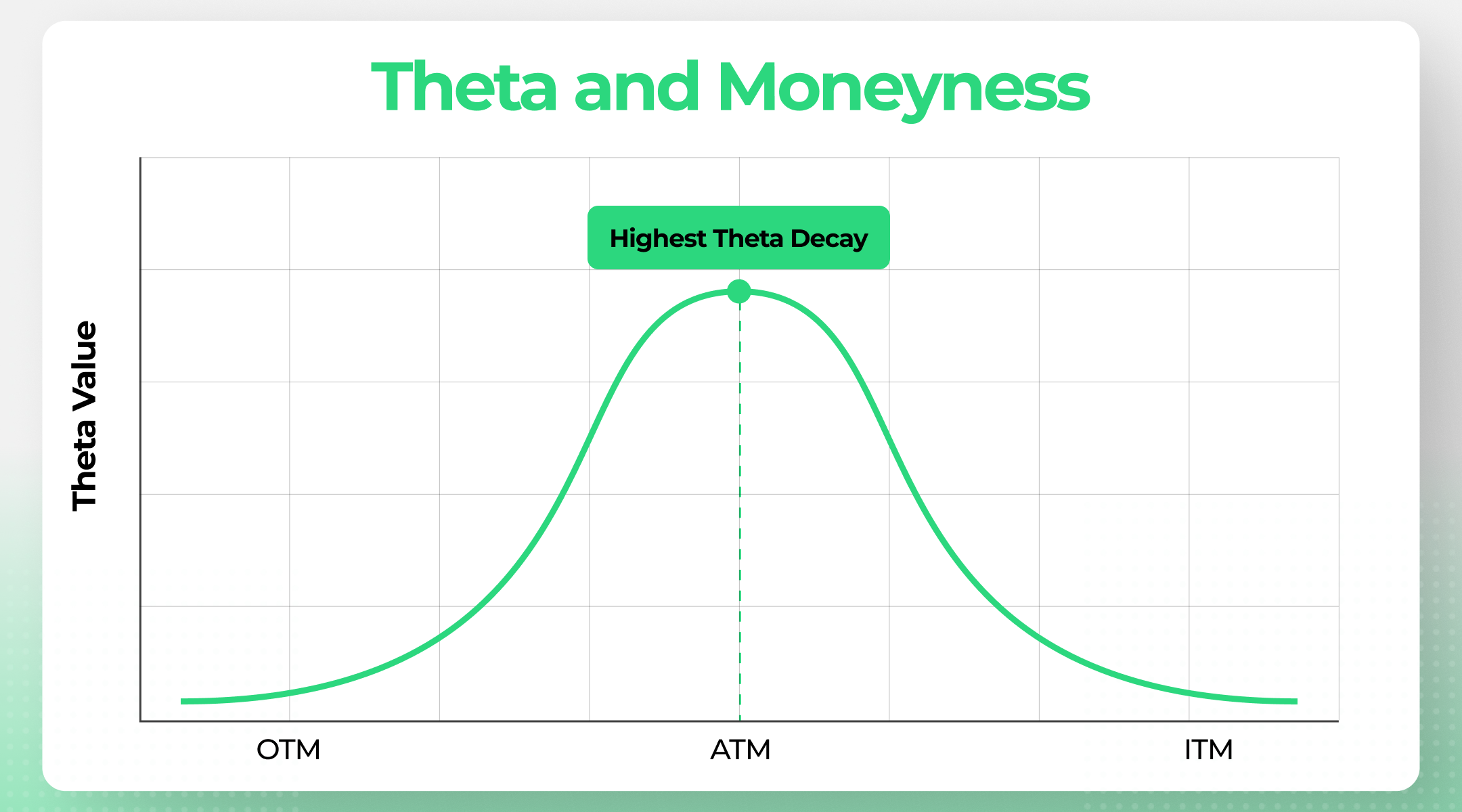

- ATM options near expiration see the sharpest theta acceleration. This is where time decay hits hardest, because ATM options carry the most extrinsic value and it drains rapidly in the final days.

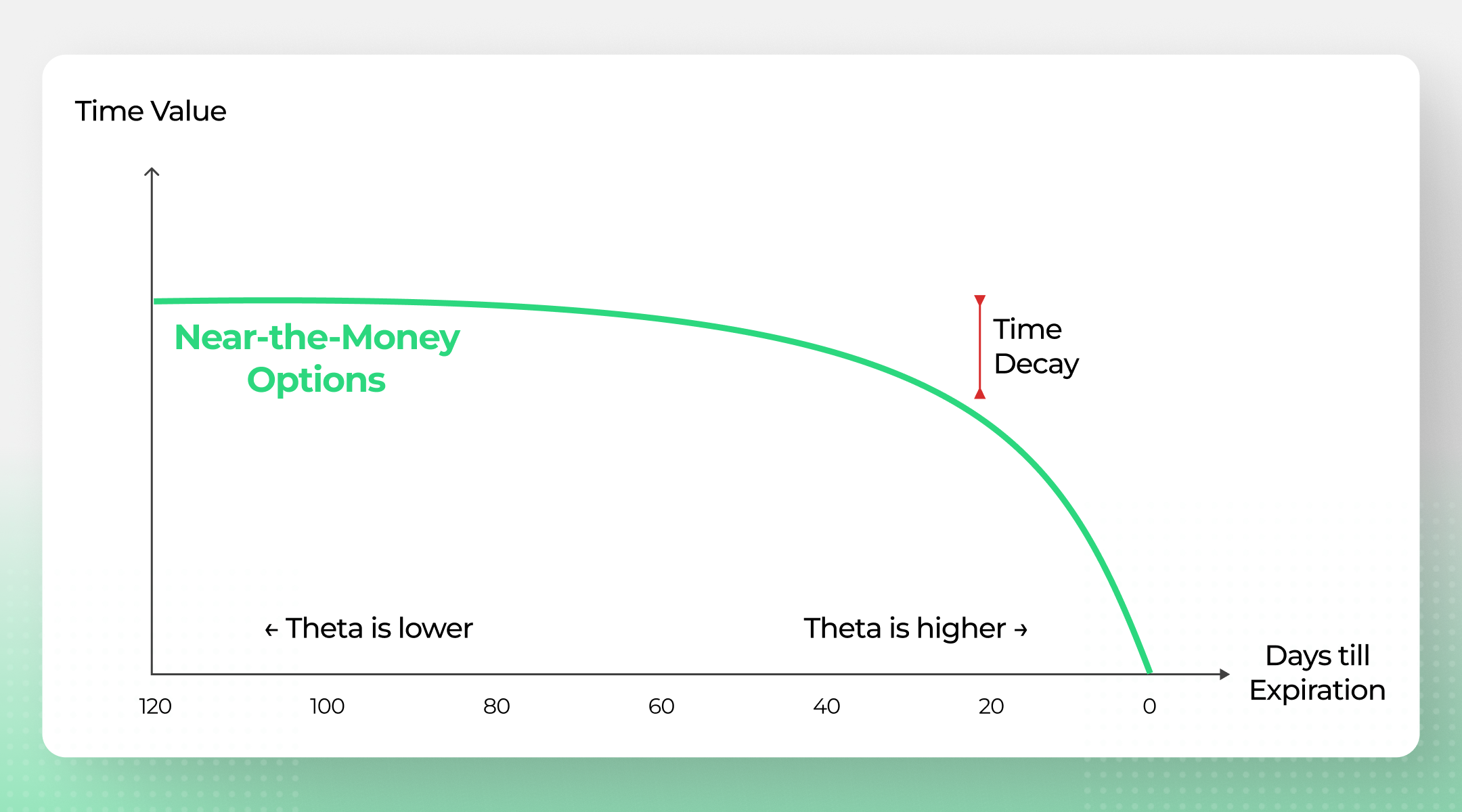

The relationship between theta and moneyness isn't linear: it peaks sharply at the money and tapers off in both directions. ATM options carry the most extrinsic value, so they have the most to lose each day. As you move further OTM or deeper ITM, extrinsic value shrinks and theta shrinks with it. The chart below shows this characteristic bell shape:

This is why ATM options are the favorite playground for premium sellers: they offer the richest daily decay. It's also why deep ITM long calls or puts behave almost like stock — there's barely any time value left to erode.

The theta decay of ATM options has a very characteristic shape. The chart below shows how this plays out. Theta doesn't decay in a straight line - it accelerates as expiration gets closer:

So, what is theta in options when it comes to extrinsic value? It depends entirely on moneyness and time to expiration. Understanding what theta means in options comes down to this: it's a measure of how much embedded time value a contract has left and how quickly that value is disappearing. Traders use it to evaluate whether the remaining premium justifies holding or entering a position.

Theta in Options as a Risk Indicator

Once you understand what theta means in options from a pricing standpoint, the next step is using it as a risk indicator..

Say you sell 1 XYZ 100-strike put and the theta is $10 per day. That $10/day in time decay sounds nice, but you're taking on $10,000 in notional stock risk (100 shares × $100 strike). If XYZ expires above $100, you keep the full premium. If it drops to $0, you're on the hook for $10,000.

Now scale that up. Sell 10 of the same put and your daily theta jumps to $100, but your notional exposure is $100,000.

- 1 short put: $10/day theta, $10,000 notional risk

- 10 short puts: $100/day theta, $100,000 notional risk

The more theta you collect, the more risk you carry - they go hand in hand.

This is why monitoring your total portfolio theta matters, and why having options theta explained from a risk angle is just as important as understanding time decay. It gives you a quick read on your overall exposure. If your daily theta in options looks unusually high, that's a sign you may be taking on more risk than intended. Theta in options is as much a risk gauge as it is a profitability measure, and keeping an eye on it helps you stay sized correctly.

AUTHOR

Gianluca LonginottiFinance Writer - Traders Education

Gianluca LonginottiFinance Writer - Traders EducationGianluca Longinotti is an experienced trader, advisor, and financial analyst with over a decade of professional experience in the banking sector, trading, and investment services.

REVIEWER

Leav GravesCEO

Leav GravesCEOLeav Graves is the founder and CEO of Option Samurai and a licensed investment professional with over 19 years of trading experience, including working professionally through the 2008 financial crisis.